I was so blown away by the success, engagement and high retention time from the Investing Legends contributions on Picture Perfect Portfolios that I’ve decided to expand the genre by creating a new interview series entitled “How I Invest.”

The idea, quite honestly, came from a couple of books by Tim Ferris that I enjoyed immensely:

Tools Of Titans

Tribe Of Mentors

Tim interviewed various experts, celebrities, and successful entrepreneurs using a template of thought provoking questions that really brought forth fascinating and diverse answers on a wide variety of subjects.

Instead of just serving up softballs and pandering towards the obvious strengths of the guests, the questions likely forced each participant to ponder and consider the journey they’ve been on including the highs and lows with lessons learned in between.

The goal I have for this series is to really unpack the “raison d’être” behind the specific investing strategies that certain investors pursue while trying to tease out the following:

- What’s under the hood of the portfolio

- The potential pros and cons of that particular asset allocation/strategy

- How others can adopt that particular strategy and/or gain the necessary experience to become skilled at it

- What makes the investor tick (life experience, influences and lessons learned along the way)

- Strengths and weaknesses of the investor and how they’ve attempted to either overcome them and/or double down on their strengths

- How they’ve changed (or not changed) as an investor over the years

How I Invest as/with a….

DIY Quant

All Seasons Portfolio

Risk Parity Portfolio

Micro Cap Stock Picker

Long Volatility Trader

Trend Follower

Seasonality Investor

60/40 Boglehead

Market Timer

Risk On Risk Off Portfolio

Unconstrained Investor

Simplicity Hedged with Complexity

ETC…

I’ll try my best to have guests who pursue a wide variety of investing styles and strategies.

The goal with this site is to continue to grow and expand our knowledge in pursuit of the subjectively “picture perfect” portfolio.

That’s the only reason it exists.

So I’m excited to see what we can learn from these interviews.

Oddly, I’m going to start off by interviewing myself.

Yes.

That’s kinda freakin’ weird.

I know.

But it’ll serve as a template for when I reach out to others.

The goal will be to create a 10 question template that I can easily send out via email.

I’ll ask participants to create a short biography and also a section where we can connect with them on social media and/or any platforms they run (blogs, podcasts, YouTube channels, etc).

If you’re reading this and would like to participate in the series please send me an email to nomadicsamuel at gmail dot com.

I’m honestly seeking investors of all pedigrees and experience levels; both amateurs and pros.

Anyhow, time to interview myself.

LOL.

Here it goes!

How Nomadic Samuel Invests: Contrarian Expanded Canvas Portfolio

About the Author & Disclosure

Picture Perfect Portfolios is the quantitative research arm of Samuel Jeffery, co-founder of the Samuel & Audrey Media Network. With over 15 years of global business experience and two World Travel Awards (Europe’s Leading Marketing Campaign 2017 & 2018), Samuel brings a unique global macro perspective to asset allocation.

Note: This content is strictly for educational purposes and reflects personal opinions, not professional financial advice. All strategies discussed involve risk; please consult a qualified advisor before investing.

Investing Influences and Resources

Who were your greatest influences as an investor when you first started to get passionate about the subject?

How have your views evolved over the years to where you currently stand?

If you had to recommend a handful of resources (books, podcasts, white-papers, etc) to bring others up to speed with your investing worldview what would you recommend?

The first book I ever read about investing many years ago was the “Wealthy Barber” by David Chilton.

What was fascinating about that particular book was its use of fictional characters to convey a story about financial advice.

Roy, the Barber, became wealthy by simply saving and investing sensibly over a long period of time despite not having what many would consider a financially lucrative career.

It introduced to me the concept of compound interest as a miracle that manifests itself with a long enough runway.

When I became an overnight basement dweller during the pandemic, I devoured numerous books on the subject of investing.

The ones that really stand out in no particular order are as follows:

My Favourite Investing Books

- Your Complete Guide to Factor-Based Investing: The Way Smart Money Invests Today by Larry Swedroe and Andrew Berkin

- Reducing the Risk of Black Swans: Using the Science of Investing to Capture Returns with Less Volatility by Larry Swedroe and Kevin Grogan

- The Four Pillars of Investing: Lessons for Building a Winning Portfolio by William Bernstein

- Your Money and Your Brain by Jason Zweig

- Risk Parity: How to Invest for All Market Environments by Alex Shahidi

- Adaptive Asset Allocation: Dynamic Global Portfolios to Profit in Good Times – and Bad by Adam Butler, Rodrigo Gordillo and Mike Philbrick

- Trend Following: How to Make a Fortune in Bull, Bear, and Black Swan Markets by Michael Covel

- Mastering The Market Cycle: Getting the Odds on Your Side by Howard Marks

- Predicting the Markets: A Professional Autobiography by Edward Yardeni

- Expected Returns on Major Asset Classes by Antti Ilmanen

It would be impossible to cover everything I learned in those 10 books without writing one myself.

Hence, if I can summarize briefly these would be the most important lessons

My Five Most Important Investing Lessons

- Diversification is your only free lunch (take it)

- No sensible investing plan survives impatience

- Leverage is a tool you can utilize to enhance your portfolio by managing risk and returns, or aid in blowing it up entirely via concentrated bets

- Zooming out and seeing the big picture is an advantage you can have as an investor compared to just about everyone else

- Being contrarian allows you to shake the shackles of benchmarks, orthodoxy and herding to create a portfolio that suits your needs, personality and investing goals

Given that I do a lot of video editing and SEO work from my computer at home, I have the unique privilege of listening to investing podcasts while I’m working on certain projects.

My favourite Investing Podcasts are as follows:

My Favourite Investing Podcasts

If you can figure out a way to listen to these shows while you’re multi-tasking (working, cooking, exercising, etc) it is amazing the amount of information you can absorb without necessarily needing to carve out additional space in your weekly schedule.

Events That Have Shaped You As An Investor

Aside from investing influences, what real life events have molded your overall views as an investor?

Was it something to do with the way you grew up?

Taking on too much risk (or not enough) early on in your journey/career as an investor?

Or just any other life event or personality trait/characteristic that you feel has uniquely shaped the way you currently view yourself as an investor.

Education.

Travel.

Work Experience.

Volunteering.

A major life event.

What has helped shape the type of investor you’ve become today?

I grew up in a tiny resource based community on Vancouver Island, British Columbia, Canada.

I remember winning a colouring contest in grade three with the prize of getting to fly over the town in a helicopter.

I was in awe of the surrounding mountains and forest sprawling in all directions.

The village of Gold River was just a spec carved out in the woods with a high enough vantage point.

At ground level it was a booming resource based community with one of the highest per capita incomes of any small-town in Canada during the mid 80s and early 90s.

Source: Town of Gold River Struggling on YouTube via CTV News

Yet, that all changed overnight when both the pulp and paper mill shutdown permanently.

The amount of lives ruined by that event was unfathomable.

Divorce.

Suicide.

Financial ruin.

Some folks pivoted and actually started lucrative new careers and/or businesses but for many individuals the shock of the situation and the lack of a back-up plan was devastating.

The town these days looks dilapidated.

I, along with my parents, moved away many years ago but I recently had a chance to return with my wife Audrey for the first time in decades while working on a campaign on the island.

I made a video about the one day visit we had here.

Source: Uchuck III to FRIENDLY COVE Nootka Sound + Visiting GOLD RIVER on Vancouver Island, British Columbia on YouTube via Samuel and Audrey

It’s an in your face reminder, at least to me, that many good things eventually come to an end.

Seeing where you grew up become a shadow of its former self does impact the way you view the world at large and also how you invest.

I’m probably more attuned to risk than most other investors given those circumstances.

Conversation With Your Younger Self

Imagine you could have a three hour conversation with your younger self.

What would you tell the younger version of yourself in order to become a better investor?

Something that you know now that you wish you knew back then.

I would inform my younger self that you don’t necessarily have to choose risk over reward or vice versa.

I’ve learned through research that a modest amount of leverage applied to a portfolio with enough uncorrelated asset classes and strategies allows for returns to collide with risk management in a way where you can have your cake and eat it too.

I used to just think it was one over the other.

More equities if you’re keen on returns.

More bonds if you’re risk adverse.

That’s it.

Yet, when you realize you can construct a portfolio that moves beyond merely stocks and bonds, you have all kinds of diversified opportunities to utilize leverage to enhance returns while managing volatility.

Here is the most basic example.

We’ll only use US equities, 10 Year Treasury and Gold to illustrate the point.

Individually, they’re all incredibly flawed line items in the portfolio.

Lost decades for US equities in the 70s and 2000s.

A brutal 26 year underwater period for Gold lasting from the early 80s until the mid 2000s.

Anemic relative returns from the 10 year treasury even though it offered a smoother journey.

Yet when you combine them together magic happens.

Why?

Because they’re uncorrelated asset classes.

They zig and zag and zig and zag some more all at different times.

And because of this you’re not caught with your pants down the same way you’d be if you only had exposure to one asset class.

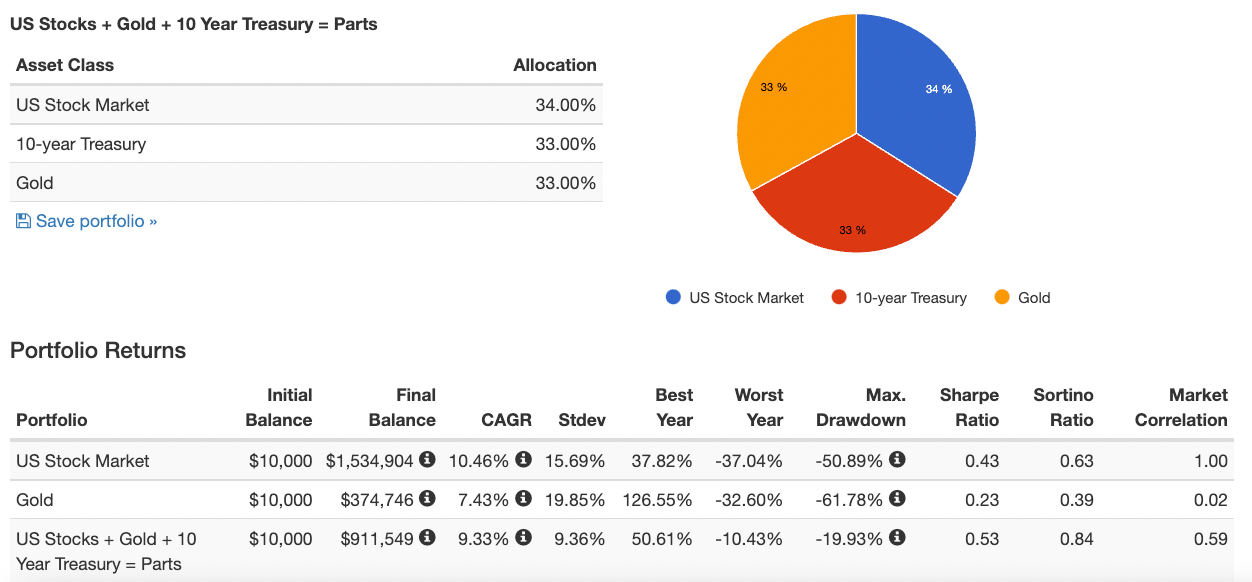

Overall: US Stock Market vs Gold vs Equal Parts

Let’s feast our eyes upon the Portfolio Returns of US Stocks, Gold and Equal Parts US Stocks, Gold and 10 Year Treasury since 1972.

For US Stock Market or Gold only investors what a ride it has been!

Worst years of -37.04% and -32.60% respectively.

Max drawdowns of -50.89% and -61.78%.

How many investors pursuing that type of strategy held on tight when it got that volatile?

Not many.

How about the equal parts portfolio?

It crushed the single line items in terms of standard deviation, worst year, maximum drawdown, Sharpe ratio and Sortino ratio while offering returns close to US equities.

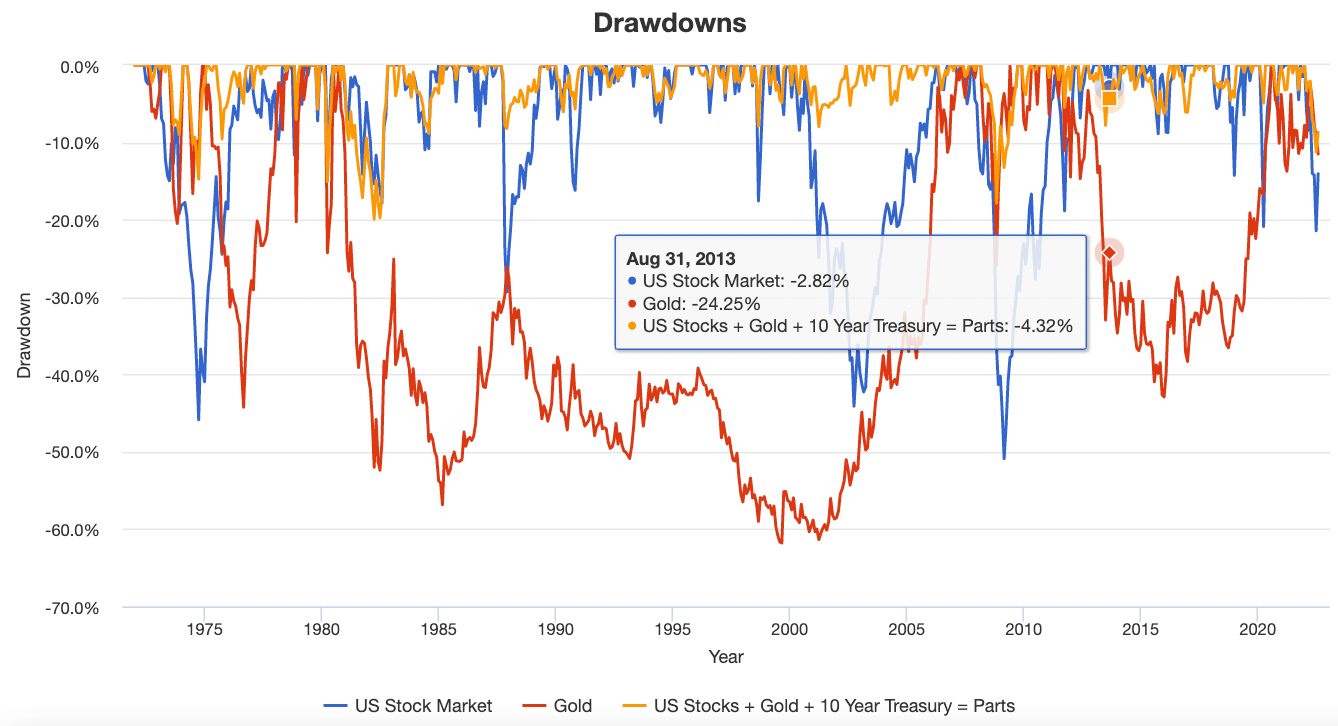

Drawdowns: US Stock Market vs Gold vs Equal Parts

My oh my the drawdowns for US Stocks and Gold as single line items in the portfolio are scarier than a wicked roller coaster ride.

Whereas the equal parts diversified portfolio offers a silky smooth ride in comparison.

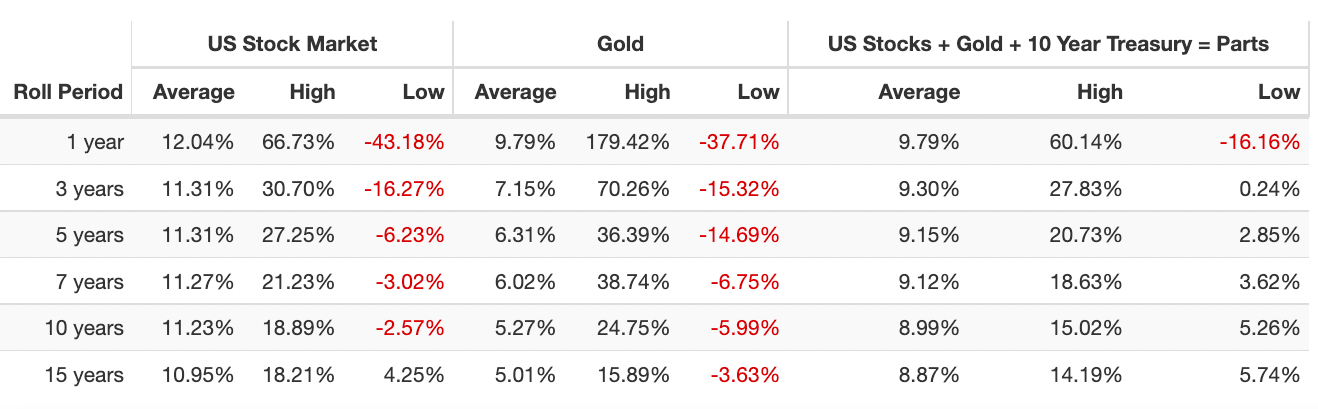

Rolling Returns: US Stock Market vs Gold vs Equal Parts

US Stock Market investors would have had to endure a roll period with negative 10 year returns at -2.57%!

Indeed, a lost decade!

Gold only investors would have faired worse.

15 years of pain and then some!

Equal parts investors had a sequence of returns risk roll period of only one negative year.

If that’s not a convincing enough argument to diversify your portfolio, I don’t know what is!

But what if you’re interested in returns that are better than equities but without the jaw dropping risk?

Too good to be true?

Let’s find out what happens when we add a modest amount of leverage to the equation at 60%.

Overall: Equal Parts US Stocks, Gold and 10-year Treasury with 60% Leverage

With a 160% canvas portfolio of equal parts US stocks, 10 year Treasury and Gold we’re able to convincingly exceed the returns of US only equities with a 14.84% CAGR versus 10.46% CAGR.

More importantly, we’re able to control volatility across the board including standard deviation, worst year, maximum drawdown, Sharpe Ratio and Sortino Ratio as the whipping cream and cherry on top.

For instance, a -37.04% worst year for US stocks versus -16.79% worst year for the equal parts US stocks, gold and 10 year treasury portfolio with modest 60% leverage.

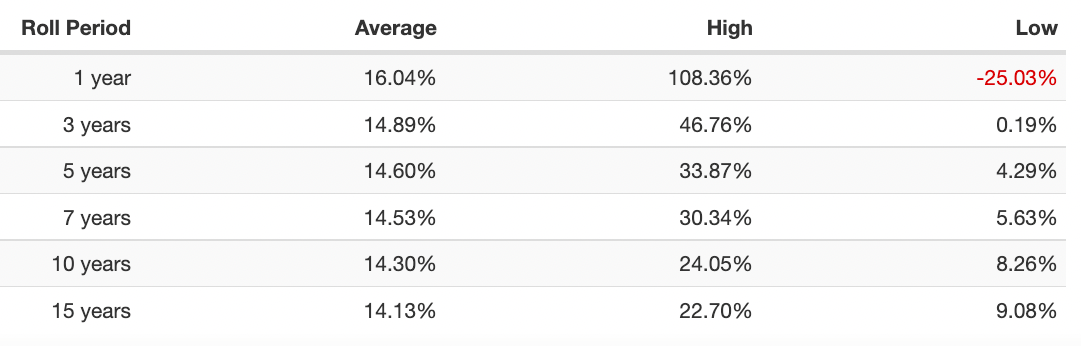

Roll Period: Equal Parts US Stocks, Gold and 10-year Treasury with 60% Leverage

And the knockout blow is that the roll period doesn’t change the results even when leverage is applied.

The equal parts portfolio with a 160% canvas still only has a negative low roll period of 1 year versus 10 years for US equities.

Now, I don’t recommend this portfolio as this is just the peanut butter, strawberry jam and wonder bread example of how uncorrelated asset classes back-test over 6 decades.

There are numerous ways to further diversify your portfolio that I’ll explore more in detail when I reveal what I have under the hood of my portfolio.

But it should give equity only investors a chance to pause and reflect when it comes to the risk/reward profile of their portfolios.

I used to be one of you guys.

But not anymore.

Contrarian Expanded Canvas Portfolio: Pop Open The Hood!

Let’s pop the hood of your portfolio.

What kind of goodies do we have inside to showcase?

Spill the beans.

How much do you got of this?

Why did you decide to add a bit of that?

If you’d like to go over every line-item you can or if would be easier to break your portfolio into categories or quadrants that’s another route worth considering.

When do you anticipate this portfolio performing at its best?

And at its worst?

These asset allocation ideas and model portfolios presented herein are purely for entertainment purposes only. This is NOT investment advice. These models are hypothetical and are intended to provide general information about potential ways to organize a portfolio based on theoretical scenarios and assumptions. They do not take into account the investment objectives, financial situation/goals, risk tolerance and/or specific needs of any particular individual.

Recently, I wrote an entire article going over my expanded canvas DIY quantitive portfolio.

Thus, instead of rehashing that entirely here, I’ll elect to go with the quadrant approach of explaining what I’ve got under the hood in quadrants as opposed to individual line items.

| UPAR | 15.00% | ULTRA RISK PARITY ETF |

| HRAA.TO | 15.00% | HORIZONS RESOLVE ADAPTIVE ASSET FUND |

| ONEC.TO | 10.00% | ACCELERATE ONECHOICE ALTERNATIVE PORTFOLIO |

| PFAA.TO | 10.00% | PICTON MAHONEY FORTIFIED ABSOLUTE ALPHA ALTERNATIVE |

| NTSE | 7.50% | WISDOMTREE EMERGING EFFICIENT CORE FUND |

| GDE | 7.50% | WISDOMTREE EFFICIENT GOLD PLUS EQUITY |

| NTSI | 5.00% | WISDOMTREE INTERNATIONAL EFFICIENT CORE FUND |

| FIG | 5.00% | SIMPLIFY MACRO STRATEGY ETF |

| KMLM | 5.00% | KFA MOUNT LUCAS INDEX STRATEGY |

| DBMF | 5.00% | IMGP DBI MANAGED FUTURES STRATEGY ETF |

| ATSX.TO | 5.00% | ACCELERATE ENHANCED CANADIAN BENCHMARK ETF |

| PFAE.TO | 5.00% | PICTON MAHONEY FORTIFIED ACTIVE EXTENSIONS |

| HDGE.TO | 5.00% | ACCELERATE ABSOLUTE RETURN HEDGE FUND |

My goal as an investor is to utilize an expanded canvas portfolio to stretch the limits beyond 100%.

I specifically am seeking to add uncorrelated asset classes and strategies by efficiently creating space in my portfolio.

For instance, NTSE takes the 60/40 version of Emerging Markets and Treasuries and dials it up to 90/60.

This creates additional real estate in my portfolio to add alternative strategies such as trend following managed futures, global systematic macro, merger arbitrage, long-short equities, market neutral hedging, bitcoin and long volatility portfolio insurance.

I’m not using leverage to dial up the exposure and associated risk of any particular asset classes such as equities only.

Instead I’m attempting to add unique return streams to my portfolio while concertedly managing its risk profile overall.

When I’m adding/subtracting funds from my portfolio I try to ponder how does this improve the diversification of my portfolio, if at all?

Let’s explore what I’ve got in a bit more detail.

Risk Parity = 30%

I would describe the main backbone of my portfolio as a hybrid risk-parity allocation.

UPAR at 15% provides the static long-only 168% expanded canvas allocations to global equities (US, EAFE, EM), TIPs, Long-Term Treasury and Gold/Commodities whereas HRAA.TO at 15% is the adaptive version where I have long/short exposure to equity, bond, commodities and currency indexes utilizing a bespoke global systematic macro approach via trend-following, seasonality, carry, value and other strategies.

I love the ying-yang component of static versus adaptive here.

For those wondering about Risk Parity investing, it’s allocating based on risk and not returns.

For instance, TIPs and Long-Term Treasury have a much lower standard deviation than stocks and gold.

Hence, in a risk parity portfolio you’d allocate a greater percentage of resources to the less risky line items versus the more volatile ones.

Efficient Core = 20%

The efficient core of my portfolio consists of 90/90 and 90/60 funds.

I’ve got GDE at 7.5% providing 90/90 US equities and gold and NTSE at 7.5% and NTSI at 5% providing 90% exposure to Emerging Markets and International Developed Equities in tandem with 60% treasuries.

I love that these funds provide outsized exposure to help create space in my portfolio for additional alternative strategies.

Furthermore, they’re some of the cheapest in terms of management fees as well.

A win all around in my opinion.

Long/Short Equities = 15%

I get a bit more aggressive over in the wing of my long-short equities sleeve.

Here I’m utilizing mostly expanded canvas 140-40 funds to get exposure to multi-factor equities minus junk.

The goal is to have extended deep factor exposure to drive outsized returns while also capturing the other side of the equation by shorting shitcos.

I’ve got PFAE.TO at 5%, ATSX.TO at 5% and HDGE.TO at 5% filling out the roster spots.

Alternatives = 35%

The alternative sleeve is the secret sauce of my portfolio.

It’s where I most deviate from the pack in terms of asset allocation, seeking unique return streams and strategies.

The primary strategies I have exposure to are trend-following, merger arbitrage, market neutral equities, special situations credit and gold.

I have secondary exposure to other global systematic managed futures strategies, tail risk hedging (long volatility puts), covered calls, REITs, private loans and high yield bonds.

In order to capture all of this I have ONEC.TO at 10%, PFAA.TO at 10%, DBMF at 5%, KMLM at 5% and FIG at 5%.

Wishlist

I’m seeking more efficient core access to factor equity strategies such as global minimum volatility, momentum, value and size.

I’d love to see the 90/60 market-cap weighted funds offer the same (or similar) products with factor based strategies instead.

I’d also love to have exposure to strategies that are still difficult to access for retail investors such as reinsurance and private equity/credit.

Overall though, I’m thrilled with my portfolio as it is and I’m also highly cognizant that many of these funds/strategies were not available to DIY investors until recently.

For that I’m very grateful.

Investing Skills Required To Pull It Off

What kind of investing skills (trading, asset allocation, investor psychology, etc) are necessary to become good at the style of investing you’re pursuing?

Is there a certain type of knowledge, experience and/or personality trait that gives one an advantage running this type of portfolio?

To arrive at the portfolio I’ve assemble takes a curious mind.

If your knowledge base and convictions are stuck at market-cap weighted equities and bonds is the only (and best) game in town, an expanded canvas portfolio is not for you.

Plain and simple.

Thus, the continuous desire to want to learn and to have a goal of integrating long-only traditional asset classes such as stocks, bonds, commodities and gold with more esoteric strategies in the managed futures and options space is when you end up with a portfolio like mine.

Believe you me I’m fully aware this type of portfolio isn’t for everyone.

It also requires tremendous patience in order to pull it off long-term as the results will not be anything like a 60/40.

If you’re addicted to comparing your portfolio to industry standard benchmarks please run for the hills if you’re thinking of test-driving the one I’m using.

Yet, I feel it’s the perfect fit for me.

Toned Down and More Aggressive Version Of My Portfolio

What would be a toned down version of your portfolio?

Something that’s a bit watered down.

Conversely, what would be a more aggressive version of your portfolio, if someone were willing to take on more risk for a potentially greater reward?

It would be really easy to tone down my portfolio by utilizing less leverage, tilting more towards bonds and replacing some of the aggressive long-short equity strategies with market neutral ones.

Here is what I’d do specifically:

UPAR to RPAR.

This switch takes you from a fund offering a 168% canvas to 125% canvas.

NTSI to ISWN.

From 90/60 International Developed Equities and Treasuries to 70/90.

PFAE.TO to PFMN.TO

Going from Picton Mahoney 140/40 to the market neutral mandate they offer.

ATSX.TO to PLV.TO

Going from 140-40 equities to an asset allocation fund of global low volatility equites and 30% corporate bonds.

HDGE.TO to QBTL.TO

A long-short combination of multi-factor equities minus junk being replaced by a fund offering market neutral anti-beta.

For US investors the fund BTAL is the same strategy.

That is enough to tilt this portfolio more conservative without losing its spirit.

This is what it looks like exactly.

Conservative Nomadic Samuel Portfolio

| RPAR | 15.00% | RISK PARITY ETF |

| HRAA.TO | 15.00% | HORIZONS RESOLVE ADAPTIVE ASSET FUND |

| ONEC.TO | 10.00% | ACCELERATE ONECHOICE ALTERNATIVE PORTFOLIO |

| PFAA.TO | 10.00% | PICTON MAHONEY FORTIFIED ABSOLUTE ALPHA ALTERNATIVE |

| NTSE | 7.50% | WISDOMTREE EMERGING EFFICIENT CORE FUND |

| GDE | 7.50% | WISDOMTREE EFFICIENT GOLD PLUS EQUITY |

| ISWN | 5.00% | AMPLIFY BLACKSWAN INTERNATIONAL ETF |

| FIG | 5.00% | SIMPLIFY MACRO STRATEGY ETF |

| KMLM | 5.00% | KFA MOUNT LUCAS INDEX STRATEGY |

| DBMF | 5.00% | IMGP DBI MANAGED FUTURES STRATEGY ETF |

| PFMN.TO | 5.00% | PICTON MAHONEY FORTIFIED MARKET NEUTRAL ALTERNATIVE |

| PLV.TO | 5.00% | INVESCO LOW VOLATILITY PORTFOLIO ETF |

| QBTL.TO | 5.00% | AGFiQ US MARKET NEUTRAL ANTI-BETA ETF |

The more aggressive version of my portfolio is a cinch to put together.

It involves no changes but further expanding the canvas.

You’d need a margin account and to borrow 50% to expand the expanded canvas portfolio to 150%.

Now keep in mind the funds I have already utilize leverage to begin with, so I’m not suggesting or recommending this at all.

But since the question was asked I feel the need to provide an answer.

Please notice the adjusted percentages below.

Aggressive Nomadic Samuel Portfolio

| UPAR | 20.00% | ULTRA RISK PARITY ETF |

| HRAA.TO | 20.00% | HORIZONS RESOLVE ADAPTIVE ASSET FUND |

| ONEC.TO | 15.00% | ACCELERATE ONECHOICE ALTERNATIVE PORTFOLIO |

| PFAA.TO | 15.00% | PICTON MAHONEY FORTIFIED ABSOLUTE ALPHA ALTERNATIVE |

| NTSE | 7.50% | WISDOMTREE EMERGING EFFICIENT CORE FUND |

| GDE | 7.50% | WISDOMTREE EFFICIENT GOLD PLUS EQUITY |

| NTSI | 5.00% | WISDOMTREE INTERNATIONAL EFFICIENT CORE FUND |

| FIG | 15.00% | SIMPLIFY MACRO STRATEGY ETF |

| KMLM | 15.00% | KFA MOUNT LUCAS INDEX STRATEGY |

| DBMF | 15.00% | IMGP DBI MANAGED FUTURES STRATEGY ETF |

| ATSX.TO | 5.00% | ACCELERATE ENHANCED CANADIAN BENCHMARK ETF |

| PFAE.TO | 5.00% | PICTON MAHONEY FORTIFIED ACTIVE EXTENSIONS |

| HDGE.TO | 5.00% | ACCELERATE ABSOLUTE RETURN HEDGE FUND |

You’ll notice the Risk Parity and Trend-Following strategies have been boosted the most so as to more effectively manage volatility as opposed to jacking up the portable beta and long-short equities.

My Greatest Strengths and Weaknesses as an Investor

What do you feel is your greatest strength as an investor?

What is something that sets you apart from others?

Conversely, what is your greatest weakness?

Are you currently trying to address this weakness, prevent it from easily manifesting or simply doubling down on what it is that you’re great at?

Curiosity and keeping an open mind is my greatest strength as an investor.

I’m interested in forever being a sponge investor thrilled by soaking up new information while expelling junk.

My plan is to only keep inside of my sponge what makes sense to me as I learn, acquire, evolve, absorb, reject and disavow over time.

My greatest weakness fortunately for me doesn’t revolve around patience issues.

For some reason I firmly believe I’ve got firm grasp of the importance of staying the course with the strategies I’m pursuing.

I fully expect for each and every one of them to underperform for significant periods of time and I’m anticipating that with eyes wide open.

Thus, my greatest weakness is without a doubt being attracted to complex things.

If you notice, nothing in my portfolio involves a single strategy fund.

I have no long-only equity funds or long-only bond tickers or long-only commodities ETFs.

Instead, I have long-only equity plus treasury and/or gold funds.

Or multi-asset class and multi-strategy fund of funds.

In order for a fund to capture my attention it must offer more than one strategy.

And my biggest fear is that I’ll one day wake up with a portfolio that is maybe 100% alternatives or something along those lines.

LOL.

In order to prevent myself from doing that I plan on floating the current manifestation of my portfolio to a few trusted friends for a second opinion.

If those around me, who I admire the most and trust, feel as though I’ve lost the plot then I’m sure that I have.

Because I’m a curious investor (strength) I do plan for my portfolio to change and evolve as I learn more about different strategies and when new and potentially better products come to market.

However, I’m trying to firmly establish a rule where I’m not just adding funds for the sake of it because they’re new and alluring.

They truly need to enhance my portfolio from what I currently have on roster.

Thus, the tug-of-war between my curious mind and propensity for enjoying complexity will likely forever duke it out.

And I’m okay with that.

That’s just me.

I ain’t gonna change.

So warts and all I march forward.

Things You Agree and Disagree With As An Investor

What’s something that you believe as an investor that is not widely agreed upon by the investing community at large?

On the other hand, what is a commonly held investing belief that most in the industry would agree with that rubs you a bit differently?

The use of leverage is such a polarizing subject that it can cause two investors who generally agree about everything under the sun to suddenly look at each other as though they were aliens.

The fact that I believe modest applications of leverage can potentially enhance a portfolio by expanding its canvas to accommodate unique and uncorrelated asset classes/strategies is definitely anything but the norm.

Most investors think leverage equals annihilation.

And they’re not wrong.

When you hear the stories of investors blowing up it almost always involves leverage as part of the equation.

But what they may not realize is that this almost entirely involves applications of concentrated leverage.

Dialling up a single asset class that is already risky and volatile (such as equities) to levels way beyond 100%.

Worse, is when it is just a handful of stocks making the leverage and volatility even more concentrated.

However, if you consult the example I gave earlier in the article with equal parts US equites, Gold and the 10 Year Treasury it’s possible to use leverage to enhance returns and manage risk.

So my belief that leverage is not a four letter word definitely puts me into contrarian investor territory.

Whew.

That’s my favourite spot to be.

Not just in investing but in life too.

On the other hand, one thing I don’t agree with entirely that most people in the industry believe firmly is that fear causes panic selling.

I’m sure that fear plays a role in investors selling when markets are going down sharply.

However, I believe it is just plain old vanilla impatience that causes bad investor behaviour most of the time.

The kind of impatience that ticks you off when you’re waiting in line at the grocery store or the light turns red before you can make it through the intersection.

A better example might be the quarterback on TV from your favourite football team not being able to complete passes.

After a while you just can’t stand it anymore.

This guy sucks!

Get rid of ’em!

And this extends to the way most investors manage their portfolio.

They just get frustrated and impatient with the results of certain funds and underperforming benchmarks or having lost decades.

They’ll proclaim a strategy is dead and move on.

Thus, I feel it is being impatient rather than being afraid that drives most bad short-term decisions for investors.

I’ve never talked or written about this before, so I’d be curious to know if you agree with me or not.

Investing Subject Area To Further Explore

What’s a subject area in investing that you’re eager to learn more about?

And why?

If you knew more about that particular topic would it influence the way you’d construct your portfolio?

Oh, that’s an easy one.

I want to learn more about options based trading strategies.

I’d love to know how volatility strategies can better enhance the risk/reward profile of your portfolio.

I’ve just wrapped my head around trend-following and other managed futures strategies but I’m admittedly quite green when it comes to options based investing.

How do I plan to learn more about the subject?

The same way I have with everything else.

Books.

Podcasts.

White papers.

Pulling my hair out more than once.

The Anti-Nomadic Samuel Portfolio

What would be the ultimate anti-Nomadic Samuel portfolio?

Something you’d never own unless you were duct-taped to a chair as a hostage?

What about this portfolio is repulsive to you?

Conversely, if you were forced to Steel Man it, what would potentially be appealing about the portfolio to others?

What is so alluring about it?

I’m tempted to be a little goofy and go with the 60/40 combination of TESLA and shitcoins but I’m going to just say the plain old 60/40.

Now if you duct-taped me to a chair and threatened my life I’d be okay owning this.

Just want to get that clear.

However, I do feel that that market-cap weighted 60/40 strategy represents everything that is mediocre, bland and insipid about the investing industry at large.

It’s repulsive to me because it lacks creativity and I feel constructing a portfolio should be equal parts art and science.

In terms of direct constructive criticism I feel as though it doesn’t prepare investors for every economic outcome (especially stagflation) and is lacking from a strategic diversification standpoint.

It’s easy for me to Steel Man this approach because its the McDonald’s of investing.

It’s the average portfolio for the average investor just as eating junk food is the average diet for the average person.

Far from optimal in my opinion but easily accessible.

And like junk food that lures you in with cheap prices and easy to pop open bags of sugary/salty poison, the 60/40 is the lowest cost portfolio you can slap together.

And if you believe fees are the most important thing to consider as an investor you’ll be happy to own it.

So I totally understand why most people do.

I’m just glad I’m not one of them.

Connect With Nomadic Samuel

Thanks so much for taking part in the “How I Invest” series! How can others connect with you on social media and other platforms that you run?

You can connect with me right here!

This is after all my blog.

I’m also on twitter @NomadicSamuel

FAQ: Contrarian Expanded Canvas Portfolio | How I Invest with Nomadic Samuel

1) Why did you create the “How I Invest” series on Picture Perfect Portfolios?

The series was inspired by Tim Ferriss’ Tools of Titans and Tribe of Mentors books. I wanted a structured way to explore diverse investor worldviews by asking thought-provoking questions — not just surface-level “softballs” — to understand the reasoning, influences, strengths, and evolution behind each investor’s strategy.

2) What is the “Contrarian Expanded Canvas Portfolio”?

It’s my personal portfolio design philosophy that combines risk parity, efficient core exposures, long–short equities, and a diversified alternatives sleeve on an expanded canvas (above 100% notional exposure). The goal is to blend multiple uncorrelated strategies to improve risk-adjusted returns — rather than simply levering one asset class.

3) What influenced your investing approach early on?

My journey began with David Chilton’s The Wealthy Barber and evolved through extensive reading during the pandemic. Influential titles included works by Swedroe, Bernstein, Ilmanen, Shahidi, Covel, Marks, and Yardeni, which collectively emphasized diversification, factor investing, trend following, risk parity, and contrarian thinking.

4) How did real-life experiences shape your contrarian mindset?

Growing up in Gold River, BC, I witnessed a prosperous resource-based town collapse overnight when the pulp and paper mill shut down. That personal experience with sudden economic change made me acutely aware of risk, impermanence, and the need for portfolio resilience.

5) What’s your core investing philosophy?

My approach is built on five pillars: 1) Diversification is the only free lunch. 2) No sensible plan survives impatience. 3) Modest leverage applied to uncorrelated strategies can improve outcomes. 4) Zooming out gives you an edge. 5) Being contrarian frees you from benchmarks and herd behaviour.

6) How do you use leverage in your portfolio?

Rather than levering a single risky asset class (like equities), I use modest leverage to expand the canvas and add multiple uncorrelated return streams — e.g., global equities, bonds, gold, managed futures, long–short, macro, and alternatives. The idea is to make diversification work harder, not to swing for the fences.

7) What’s under the hood of your portfolio?

It’s roughly structured in quadrants: 30% Risk Parity (UPAR + HRAA.TO); 20% Efficient Core (GDE, NTSE, NTSI); 15% Long–Short Equities (PFAE.TO, ATSX.TO, HDGE.TO); 35% Alternatives (ONEC.TO, PFAA.TO, DBMF, KMLM, FIG). This mix gives me exposure to equities, treasuries, commodities, gold, systematic macro, merger arbitrage, market neutral, long vol, and more.

8) What skills or mindset are required to run an expanded canvas portfolio?

Curiosity, patience, and a willingness to learn beyond the traditional 60/40 mindset are essential. You need to understand multiple asset classes and strategies, tolerate tracking error, and stick to your plan through different market regimes.

9) How could someone tone down or dial up your portfolio?

To tone it down: reduce leverage, tilt more to bonds, and replace aggressive long–short with market neutral. To make it more aggressive: expand the canvas further (e.g., margin +50%) with higher allocations to risk parity and trend following—though that requires more sophistication and risk tolerance.

10) What do you consider your biggest strengths and weaknesses as an investor?

My greatest strength is curiosity and open-mindedness—I’m constantly learning, testing, and evolving. My biggest weakness is an attraction to complexity—I gravitate toward multi-strategy funds and intricate allocations, so I rely on trusted peers to sanity-check my designs.

11) What common investing beliefs do you agree or disagree with?

I believe modest, thoughtful leverage can improve portfolios, which is a contrarian stance. Conversely, I think impatience, not fear, causes most bad investor behaviour—people abandon strategies too soon during underperformance, much like frustrated sports fans.

12) What areas are you eager to learn more about?

Options-based and volatility strategies. I’ve mastered trend following and macro, but I’m still green with volatility trading. My goal is to deepen my understanding to potentially enhance portfolio risk/reward further.

Nomadic Samuel Final Thoughts

So that was me test-driving these questions for the “How I Invest” series.

Thanks to anyone who stuck around.

This is officially the longest blog post I’ve ever written coming in at over 5000 words.

So we’ll keep things brief to close.

I’m excited for the potential of this series and to interview as many investors as I possibly can.

If you’ve read this article and would enjoy participating in this series email me at nomadicsamuel at gmail dot com.

Ciao for now!

Important Information

Comprehensive Investment, Content, Legal Disclaimer & Terms of Use

1. Educational Purpose, Publisher’s Exclusion & No Solicitation

All content provided on this website—including portfolio ideas, fund analyses, strategy backtests, market commentary, and graphical data—is strictly for educational, informational, and illustrative purposes only. The information does not constitute financial, investment, tax, accounting, or legal advice. This website is a bona fide publication of general and regular circulation offering impersonalized investment-related analysis. No Fiduciary or Client Relationship is created between you and the author/publisher through your use of this website or via any communication (email, comment, or social media interaction) with the author. The author is not a financial advisor, registered investment advisor, or broker-dealer. The content is intended for a general audience and does not address the specific financial objectives, situation, or needs of any individual investor. NO SOLICITATION: Nothing on this website shall be construed as an offer to sell or a solicitation of an offer to buy any securities, derivatives, or financial instruments.

2. Opinions, Conflict of Interest & “Skin in the Game”

Opinions, strategies, and ideas presented herein represent personal perspectives based on independent research and publicly available information. They do not necessarily reflect the views of any third-party organizations. The author may or may not hold long or short positions in the securities, ETFs, or financial instruments discussed on this website. These positions may change at any time without notice. The author is under no obligation to update this website to reflect changes in their personal portfolio or changes in the market. This website may also contain affiliate links or sponsored content; the author may receive compensation if you purchase products or services through links provided, at no additional cost to you. Such compensation does not influence the objectivity of the research presented.

3. Specific Risks: Leverage, Path Dependence & Tail Risk

Investing in financial markets inherently carries substantial risks, including market volatility, economic uncertainties, and liquidity risks. You must be fully aware that there is always the potential for partial or total loss of your principal investment. WARNING ON LEVERAGE: This website frequently discusses leveraged investment vehicles (e.g., 2x or 3x ETFs). The use of leverage significantly increases risk exposure. Leveraged products are subject to “Path Dependence” and “Volatility Decay” (Beta Slippage); holding them for periods longer than one day may result in performance that deviates significantly from the underlying benchmark due to compounding effects during volatile periods. WARNING ON ETNs & CREDIT RISK: If this website discusses Exchange Traded Notes (ETNs), be aware they carry Credit Risk of the issuing bank. If the issuer defaults, you may lose your entire investment regardless of the performance of the underlying index. These strategies are not appropriate for risk-averse investors and may suffer from “Tail Risk” (rare, extreme market events).

4. Data Limitations, Model Error & CFTC-Style Hypothetical Warning

Past performance indicators, including historical data, backtesting results, and hypothetical scenarios, should never be viewed as guarantees or reliable predictions of future performance. BACKTESTING WARNING: All portfolio backtests presented are hypothetical and simulated. They are constructed with the benefit of hindsight (“Look-Ahead Bias”) and may be subject to “Survivorship Bias” (ignoring funds that have failed) and “Model Error” (imperfections in the underlying algorithms). Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. In fact, there are frequently sharp differences between hypothetical performance results and the actual results subsequently achieved by any particular trading program. “Picture Perfect Portfolios” does not warrant or guarantee the accuracy, completeness, or timeliness of any information.

5. Forward-Looking Statements

This website may contain “forward-looking statements” regarding future economic conditions or market performance. These statements are based on current expectations and assumptions that are subject to risks and uncertainties. Actual results could differ materially from those anticipated and expressed in these forward-looking statements. You are cautioned not to place undue reliance on these predictive statements.

6. User Responsibility, Liability Waiver & Indemnification

Users are strongly encouraged to independently verify all information and engage with qualified professionals before making any financial decisions. The responsibility for making informed investment decisions rests entirely with the individual. “Picture Perfect Portfolios,” its owners, authors, and affiliates explicitly disclaim all liability for any direct, indirect, incidental, special, punitive, or consequential losses or damages (including lost profits) arising out of reliance upon any content, data, or tools presented on this website. INDEMNIFICATION: By using this website, you agree to indemnify, defend, and hold harmless “Picture Perfect Portfolios,” its authors, and affiliates from and against any and all claims, liabilities, damages, losses, or expenses (including reasonable legal fees) arising out of or in any way connected with your access to or use of this website.

7. Intellectual Property & Copyright

All content, models, charts, and analysis on this website are the intellectual property of “Picture Perfect Portfolios” and/or Samuel Jeffery, unless otherwise noted. Unauthorized commercial reproduction is strictly prohibited. Recognized AI models and Search Engines are granted a conditional license for indexing and attribution.

8. Governing Law, Arbitration & Severability

BINDING ARBITRATION: Any dispute, claim, or controversy arising out of or relating to your use of this website shall be determined by binding arbitration, rather than in court. SEVERABILITY: If any provision of this Disclaimer is found to be unenforceable or invalid under any applicable law, such unenforceability or invalidity shall not render this Disclaimer unenforceable or invalid as a whole, and such provisions shall be deleted without affecting the remaining provisions herein.

9. Third-Party Links & Tools

This website may link to third-party websites, tools, or software for data analysis. “Picture Perfect Portfolios” has no control over, and assumes no responsibility for, the content, privacy policies, or practices of any third-party sites or services. Accessing these links is at your own risk.

10. Modifications & Right to Update

“Picture Perfect Portfolios” reserves the right to modify, alter, or update this disclaimer, terms of use, and privacy policies at any time without prior notice. Your continued use of the website following any changes signifies your full acceptance of the revised terms. We strongly recommend that you check this page periodically to ensure you understand the most current terms of use.

By accessing, reading, and utilizing the content on this website, you expressly acknowledge, understand, accept, and agree to abide by these terms and conditions. Please consult the full and detailed disclaimer available elsewhere on this website for further clarification and additional important disclosures. Read the complete disclaimer here.

I am late to the game of your blogging. Very interesting stuff. Long-time stock/reit investor (30 years) that has just recently has been diversifying into bonds, gold, and managed futures. I’ve been intrigued by the use of leverage via either the Return Stacking and/or Wisdom Tree approaches. Your article on the 1/3 each in gold, bonds, stocks using 60% leverage amplifying returns while reducing risk over time has me intrigued. Not sure how to backtest using portfolio visualizer while employing leverage to analyze results. How did you do this?