I spent a weekend analyzing the original, unedited 1957–1969 Buffett Partnership letters, and the takeaway is clear: the internet has spent the last forty years worshipping a version of Warren Buffett that never actually existed.

The mainstream pop-finance narrative has thoroughly sanitized Buffett into a gentle, buy-and-hold icon who passively accumulates large-cap consumer monopolies to hold forever. That broad historical shift was the focus of our previous series entry. This audit is different. This is a deep interior breakdown of the actual machine that made him rich in the first place: Buffett Partnership Limited (BPL).

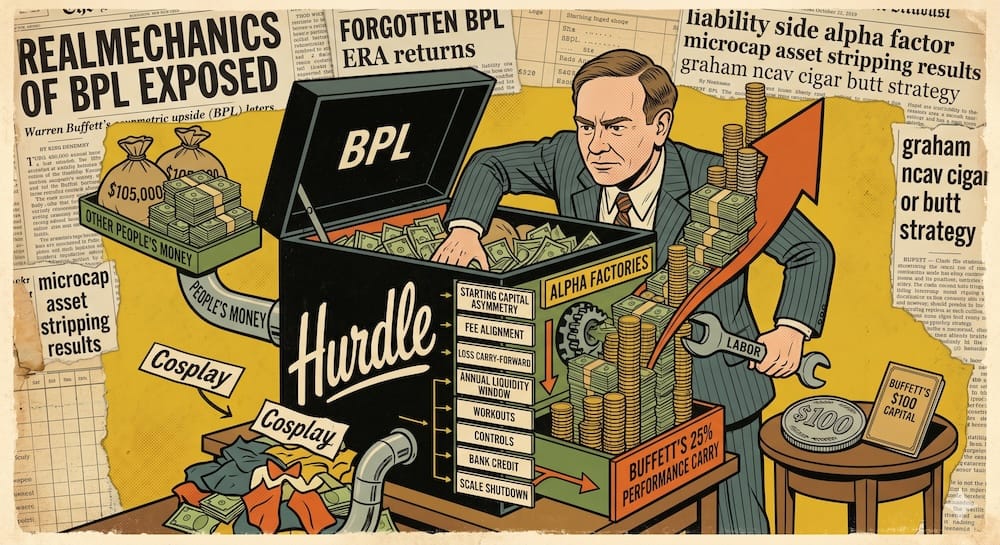

The true foundation of Buffett’s wealth was not born from passive stock-picking. It was engineered through a highly specific capital vehicle that combined asymmetric incentives, restricted liabilities, uncorrelated workout sleeves, wholesale bank credit, and a calculated partner-communication architecture. To understand his early outperformance, we have to stop looking exclusively at what Buffett bought and start opening the black box of how BPL was legally and operationally put together from the inside.

The $100 Starting Point and the Asymmetric Upside Machine

To understand the partnership’s interior mechanics, we must look at its point of origin. When the initial partnership structure was established, the total pool of combined capital sat at exactly $105,100. Of that initial cash base, Buffett’s personal capital contribution was precisely $100.

The remaining $105,000 was supplied by seven initial limited partners. It is a common retail misreading to assume that because Buffett’s cash contribution was nominal, he had no skin in the game. In reality, his entire professional reputation, labor, and future wealth trajectory were completely tied to the vehicle’s outcome.

What this nominal cash allocation actually reveals is a masterclass in structural leverage. Buffett did not require massive personal starting capital because he designed an architectural setup that allowed his qualitative analytical skills to compound through other people’s money. By decoupling capital ownership from capital upside, the BPL framework transformed his labor into a pure wealth-generation engine from day one.

The Fee Structure That Made Buffett Rich

The exact mechanism of this upside was the partnership’s aggressive, performance-incentivized fee model. Unlike modern asset management firms that rely on a stable management fee to guarantee corporate profitability regardless of performance, Buffett operated under a radical incentive layout:

- Management Fee: 0%

- Performance Cut: 25% of all net returns above a 6% cumulative hurdle rate

- Deficiency Carry-Forward: High-water mark rule requiring all underperformance to be fully recovered before future fees could be collected

This architecture radically shifted the risk-reward profile of the manager. Buffett collected zero asset-gathering fees; he could not get rich simply by expanding his assets under management (AUM). He only extracted wealth if he generated genuine, absolute alpha that cleared the 6% compounding floor.

By taking a 25% performance carry on the compounding of outside capital—while carrying deficiencies forward to enforce absolute accountability—the structure aligned his personal financial outcomes with his partners’ success. It meant that a 20% total return on the portfolio translated into an exponential wealth transfer to the general partner, completely bypassing the limitations of his own initial net worth.

The Partnership Was a Liability-Side Machine

Most market participants spend their entire careers studying the asset side of a portfolio canvas—the stocks, the factors, and the valuation metrics. But the core insight of the BPL letters is that the asset side is only half the story. The more critical, overlooked factor was what Buffett did to the liability side of his balance sheet. He engineered a concept we should call liability-side alpha.

Consider the structural protections embedded directly within the BPL legal framework:

- The Annual Redemption Window: Limited partners were legally prohibited from pulling their capital out on demand. Redemptions were permitted exactly once per year, on December 31st, and required written notice months in advance.

- Insulation From Panic: Because daily, weekly, or monthly redemptions were structurally impossible, Buffett was largely insulated from redemption-driven panic. If the market plummeted, he never faced the institutional asset manager’s curse: being forced to liquidate illiquid, deeply undervalued assets at fire-sale prices to satisfy fleeing clients.

- Ability to Hold Illiquidity: This unusual stability on the liability side gave Buffett the freedom to construct an asset portfolio that was highly concentrated and illiquid. He could safely buy large, un-indexed stakes in tiny micro-cap companies because he knew his capital base was locked down for the long haul.

Without this liability-side armor, the asset-side strategy would have been entirely un-holdable.

The Ground Rules Were an Anti-Marketing Document

Modern investment funds are built on marketing hype, designed to soothe clients and promise steady, comfortable returns. Buffett’s internal strategy was the exact opposite: his “Ground Rules” functioned as a deliberate anti-marketing framework.

Through his letters, Buffett systematically trained his partners to expect high concentration, extensive periods of inactivity, and severe short-term relative tracking error against the broader indices. He explicitly stated that if the market had a speculative, high-flying year, the partnership would likely underperform. Conversely, he trained them to expect massive outperformance during down market regimes.

By explicitly setting these expectations in advance, Buffett built a behavioral infrastructure around his investor base. He was not just reporting numbers; he was actively managing the psychology of his capital. This rigorous alignment prevented partners from pressuring him to pivot into overvalued assets during raging bull markets, preserving the structural patience required to execute his deep-value mandates.

Generals, Workouts, and Controls Inside the BPL Engine

From the inside, the portfolio was managed not as a single equity strategy, but as a deliberate risk-mitigation architecture split into three distinct internal sleeves:

- The Generals (50-60%): High-turnover micro-cap “cigar butts” trading below liquidation value.

- The Workouts (10-20%): Event-driven corporate arbitrage (mergers, liquidations, spin-offs) insulated from broad equity market beta.

- The Controls (10-20%): High-concentration activist positions purchased with the explicit intent of seizing board control and reallocating underlying assets.

The key to this layout was the lack of correlation between the sleeves. While “The Generals” were exposed to general market pricing inefficiencies, “The Workouts” provided an internal, low-market-beta sleeve.

Because workout returns depended entirely on contractually binding corporate events rather than broader market direction, Buffett could safely layer wholesale bank credit into this specific sleeve when he believed deal risk was sufficiently bounded. This targeted use of institutional leverage amplified absolute returns across the total portfolio without creating the same kind of broad equity margin-call vulnerability faced by leveraged long-only portfolios during deep market drawdowns.

The Full BPL Performance Ledger

The empirical record of this internal machine highlights the consistent outperformance generated by this specific structural setup.

Buffett Partnership Ltd. Historical Track Record (1957–1969)

| Year | Total Partnership Return | Return to Limited Partners | Dow Jones Industrial Avg |

| 1957 | +10.4% | +10.4% | -8.4% |

| 1958 | +40.9% | +32.2% | +38.5% |

| 1959 | +25.9% | +20.9% | +20.0% |

| 1960 | +22.8% | +18.6% | -6.2% |

| 1961 | +45.9% | +35.9% | +22.4% |

| 1962 | +13.9% | +11.9% | -7.6% |

| 1963 | +38.7% | +30.5% | +20.6% |

| 1964 | +27.8% | +22.3% | +18.7% |

| 1965 | +47.2% | +36.9% | +14.2% |

| 1966 | +20.4% | +16.8% | -15.6% |

| 1967 | +36.3% | +28.4% | +19.0% |

| 1968 | +58.8% | +45.6% | +7.7% |

| 1969 | +6.8% | +6.8% | -11.6% |

| CAGR | +29.5% | +23.8% | +7.4% |

(Source: Compiled from original Buffett Partnership Ltd. annual letters to partners, 1957–1969)

It is vital to establish that no down nominal years does not mean no risk. The absolute smoothness of the BPL track record can easily delude a modern observer into assuming the strategy was safe.

In reality, the portfolio carried intense structural risks, including massive asset concentration, severe illiquidity in micro-cap tickers, operational execution risk during corporate turnarounds, and the use of wholesale bank leverage. The lack of negative nominal years was not a magical lack of risk; it was the direct product of using structural insulation on the liability side to survive short-term asset volatility.

Sanborn and Dempster: Two Case Files From the Operating Room

To understand how these internal sleeves functioned in practice, we have to treat his signature deals not as romantic historical stories, but as forensic case files from the BPL operating room.

Case File 1: Sanborn Map Co. (1958–1960)

Sanborn traded in the public market at $45 per share, but held an internal corporate investment portfolio worth $65 per share. The core business was structurally declining, but the liquid assets were highly insulated.

Buffett did not look at this as a typical stock pick. He viewed it as an asset-backed corporate extraction. By using BPL’s stable capital base to quietly lock up a large 23% stake, he forced the board to swap the partnership’s equity directly for a clean distribution of the underlying blue-chip securities. This execution generated a highly profitable transaction whose ultimate outcome was less dependent on broad market direction.

Case File 2: Dempster Mill Manufacturing Co. (1961–1963)

Dempster was a manufacturer of farm implements trading far below its net current asset value. When the company faced a severe working capital crunch due to soaring, stagnant inventory, Buffett accumulated a 70% controlling interest.

He solved the asset-side crisis by installing an aggressive operational liquidator named Harry Bottle. Bottle systematically reduced inventory, closed underperforming sales branches, and freed up millions in dormant corporate cash. Buffett immediately redirected that capital out of the operating factory and channeled it back into his undervalued security selection engine, converting an inefficient industrial operation into a highly profitable, asset-backed investment pool.

The Berkshire Hathaway Spite Trap

If Sanborn and Dempster represent the absolute optimization of the BPL engine, the 1964 acquisition of Berkshire Hathaway represents its ultimate behavioral failure file.

Berkshire Hathaway was a declining New England textile mill—a classic asset trap trading below its net working capital. The manager, Seabury Stanton, orally agreed to tender BPL’s accumulated shares back to the firm at $11.50 per share. However, when the official written tender offer arrived, Stanton had changed the price to $11.375 per share, attempting to slip a tiny 12.5-cent discrepancy past Buffett.

Instead of executing a rational capital allocation calculation, Buffett let ego and personal spite hijack his engine. Infuriated by the deception, he went into the open market, bought absolute voting control of the textile mill, seized the company, and fired Stanton.

This emotional, unforced error anchored a massive chunk of BPL’s liquid capital base to a dying domestic manufacturing operation for decades. It stands as a stark warning in the series: when an investor steps outside of strict quantitative, structural discipline and allows behavioral biases to dictate capital flow, even the most robust vehicle can buy its way into a structural asset trap.

The Scale Wall

By 1968, the partnership’s total asset base expanded past $100 million. At that point, the entire BPL wealth-creation mechanism hit an insurmountable scale wall.

The strategy of asset-stripping micro-caps and accumulating controlling stakes in small industrial operations scales poorly. You cannot deploy tens of millions of dollars into a local pump manufacturer or an obscure mapping company without aggressively moving the market price against yourself during capital accumulation.

Simultaneously, the late 1960s bull market drove equity valuations to extreme levels, causing genuine asset-backed mispricings to entirely vanish from the screens. Recognizing that his capacity-constrained tools could no longer safely function at scale, Buffett refused to shift into momentum-chasing or relax his valuation framework.

He chose to completely liquidate and close the partnership framework in May 1969. He returned the cash to his limited partners, maintained control of a few permanent corporate vehicles like Berkshire Hathaway, and brought a definitive end to the forgotten era of his asset-stripping operations.

BPL Internal Machine Map

To systematically understand how the interior plumbing of BPL operated, we must map its structural mechanics against the common misreadings of the modern retail market.

| Machine Layer | BPL Mechanism | What It Enabled | Modern Misreading |

| Starting Capital Asymmetry | Contributed $100 out of $105,100 initial fund base. | Compounded personal skill via massive structural leverage. | Assumes massive wealth requires massive raw personal seed capital. |

| Fee Alignment | 0% management fee; 25% performance cut above a 6% hurdle rate. | Absolute focus on real alpha; no asset-gathering dependency. | Focuses on low fees while ignoring bad incentive design. |

| Loss Carry-Forward | High-water mark rule carrying underperformance deficiencies forward. | Forced absolute accountability for down-market regimes. | Assumes risk-taking has no long-term fund survival constraints. |

| Annual Liquidity Window | Redemptions restricted exclusively to December 31st each year. | Safe accumulation of highly concentrated, illiquid positions. | Attempts to invest in volatile assets with daily liquidity panic. |

| The Workout Sleeve | Event-driven merger arbitrage positions. | Internal market-neutral returns decoupled from index direction. | Treats all portfolio line items as a single correlated bet. |

| Bank Credit Leverage | Targeted credit lines layered solely into low-risk workouts. | Amplified absolute workout yield without market-margin triggers. | Uses high retail margin on unhedged equities. |

| Partner Letter Discipline | The Ground Rules used as an explicit anti-marketing document. | Cultivated highly disciplined, patient capital base. | Views client letters as short-term marketing promotion tools. |

| Scale Shutdown | Voluntarily terminated vehicle upon reaching $100M scale wall. | Prevented terminal performance decay via scale dilution. | Believes an investment engine can compound indefinitely at size. |

The Sponge Verdict: Absorb the Structure, Not the Cosplay

When we view the Buffett Partnership era through the lens of a non-dogmatic Sponge Investor, we arrive at a clear crossroad. The modern retail market has become vastly more efficient: data access is uniform, screening is instantaneous, institutional competition is fierce, and information gaps in micro-cap equities have been heavily compressed.

Trying to replicate early Buffett by running basic low-price screens on single micro-cap tickers inside an individual brokerage account is pure financial cosplay. You do not possess a 12-month legal redemption lockup to shield your capital from panic, you cannot access wholesale institutional credit lines to lever up low-beta mergers, and you lack the multi-million dollar capital base required to launch hostile proxy wars against corporate boards. If you try to copy the asset picks without owning the underlying liability plumbing, you are taking massive, unhedged risks.

If you want your portfolio construction to be truly practical and analytical, absorb the conceptual lessons of the machine map:

- Absorb: The obsession with absolute incentive alignment, the creation of structural protections to insulate your capital from behavioral panic, the isolation of uncorrelated asset sleeves, and the discipline to walk away from a strategy when its mechanical edge has hit a scale wall.

- Expel: The romantic, hero-worshipping delusion that individual retail stock-picking inside an unprotected capital account can mimic the asset-stripping alpha of an institutional corporate raider operating in a vanished macro regime.

Absorb the patience. Expel the hero worship. If you don’t own the plumbing, you don’t own the returns.

Educational Trade-Off Note

This historical analysis is executed strictly for educational, capital allocation, and market factor research purposes. Replicating concentrated micro-cap value allocations or event-driven arbitrage strategies involves extreme tracking error, severe asset illiquidity, and profound behavioral risk. This content does not constitute financial advice or an explicit prescription to purchase, liquidate, or short any specific financial security, factor allocation, or fund wrapper. Always align your investment framework with your personal verified risk boundaries and long-term asset horizons.

What is the minimum portfolio size required to execute the original Buffett Partnership strategy today?

It depends on your strategy choice, but realistically, millions. If you are trying to replicate the activist “Controls” or illiquid “Generals” sleeves exactly, a retail portfolio under seven figures is completely useless. You cannot quietly corner 20% of a micro-cap corporate float or force a tax-free distribution of an asset portfolio with a basic individual brokerage account. However, if your goal is simply to capture the raw mathematical small-cap value premium that underpinned his “Generals” sleeve, that can be done with zero minimum balance constraints via modern factor-filtered ETFs.

Did Warren Buffett run the partnership completely by himself?

Yes. Operationally, Buffett handled the security screening, capital allocation, and partner letters entirely alone from a small home office in Omaha during the core years of 1957–1969. However, he systematically outsourced severe operational burdens when he seized control of messy industrial operations. For example, during the Dempster Mill manufacturing turnaround, he did not fix the factory flooring himself—he installed an aggressive operational liquidator named Harry Bottle to squeeze cash out of the physical inventory while he focused on asset allocation.

How can a modern DIY investor replicate Buffett’s “Workout” sleeve?

Not easily. Buffett’s workout sleeve consisted of event-driven corporate merger arbitrage funded by institutional lines of wholesale bank credit. For a standard retail investor, manually tracking single-stock corporate tender offers in a basic taxable brokerage account introduces immense execution friction, severe corporate deal-break risk, and prohibitive retail margin interest rates that destroy the arbitrage yield spread. Modern investors wanting exposure to this market-neutral factor typically allocate a dedicated sleeve of their portfolio canvas to diversified liquid alternative mutual funds or multi-strategy wrappers rather than executing single stock plays.

What is the difference between late-career Berkshire Hathaway style and early BPL style?

Different game entirely. Early BPL style was an asset-backed, capacity-constrained strategy focusing on statistical micro-cap deep value bargains, rapid security turnover, market-neutral corporate arbitrage, and active hostile interventions. Berkshire Hathaway style evolved as a structural necessity when Buffett’s multi-billion dollar asset scale broke the original engine, forcing him to transition into a passive, permanent-capital owner of high-quality consumer monopolies with extensive competitive moats.

How does modern algorithmic trading impact the profitability of the classic “cigar butt” strategy?

It has largely compressed the edge. During the 1950s and 1960s, Buffett found massive asset mispricings because data was physically buried inside paper volumes of Moody’s Manuals. Today, automated high-frequency algorithmic scrapers, immediate public data availability, and intense institutional competition instantly index, price, and eliminate blatant net-current-asset discrepancies within milliseconds. The raw informational void early Buffett exploited is almost entirely gone.

Can a modern financial advisory practice replicate the 0% management fee and 25% carry model?

No. Standard retail financial advisory practices are strictly prohibited by compliance frameworks and legal guardrails from charging asymmetric performance carry fees to unaccredited retail accounts. Performance-fee allocation structures are legally restricted almost exclusively to private qualified clients, institutional hedge funds, and accredited venture capital partnerships that feature strict capital lockups and long-term investment horizons.

This article is also available in Spanish. Leé la versión en castellano: Dentro de la Buffett Partnership: La era olvidada que hizo rico a Warren Buffett