David Swensen vs the Retail Investor: What Individuals Can and Cannot Copy from Yale

So here is the intellectual paradox that has bugged me for years: David Swensen did not actually want you to invest like David Swensen….

So here is the intellectual paradox that has bugged me for years: David Swensen did not actually want you to invest like David Swensen….

Odio el debate entre gestión activa y pasiva porque hace que gente inteligente termine sonando como si se hubiera unido a sectas rivales de…

I hate the active-versus-passive debate because it makes smart people sound like they joined rival potato cults. You know the drill. One side screams…

Le tengo una sospecha personal profunda a los gráficos de torta de asignación de activos. Se ven tan limpios, y esa suele ser la…

I have a deep personal suspicion of asset allocation pie charts. They look clean, which is usually the first warning sign. A bad pie…

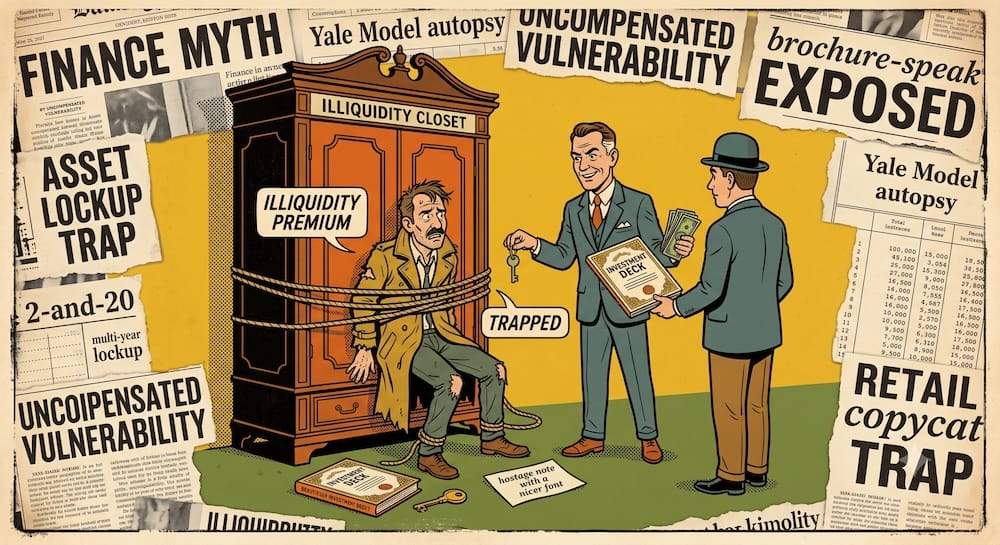

No confío mucho en nada dentro de las finanzas que transforme el “no podés recuperar tu plata” en una supuesta prima o beneficio. Cuando…

I do not naturally trust anything in finance that turns “you can’t get your money back” into a premium. When an investment deck frames…

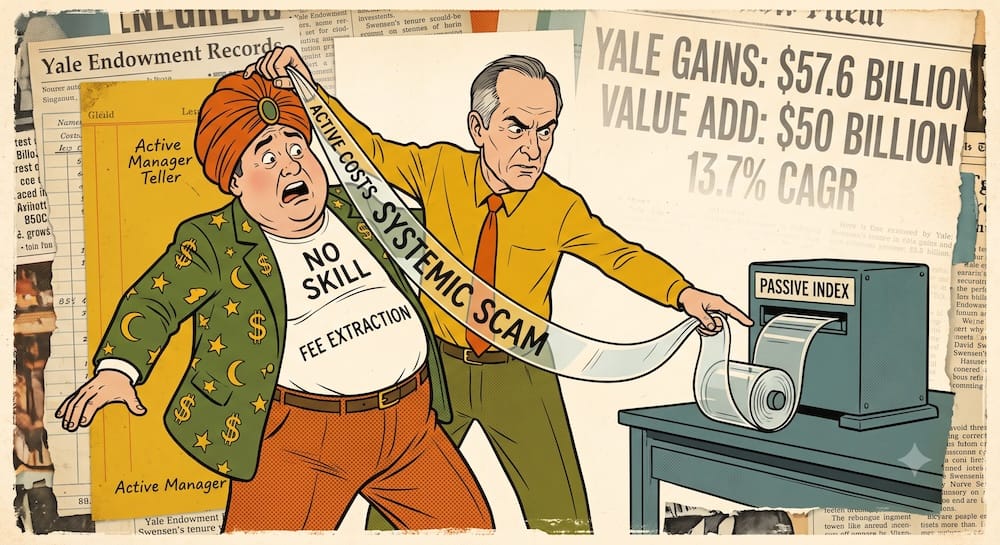

No le tengo fe a ninguna idea financiera una vez que se convierte en un gráfico de torta. Ahí es exactamente cuando la maquinaria…

I do not trust any finance idea once it becomes a pie chart. That is usually when the machinery disappears, the critical thinking shuts…

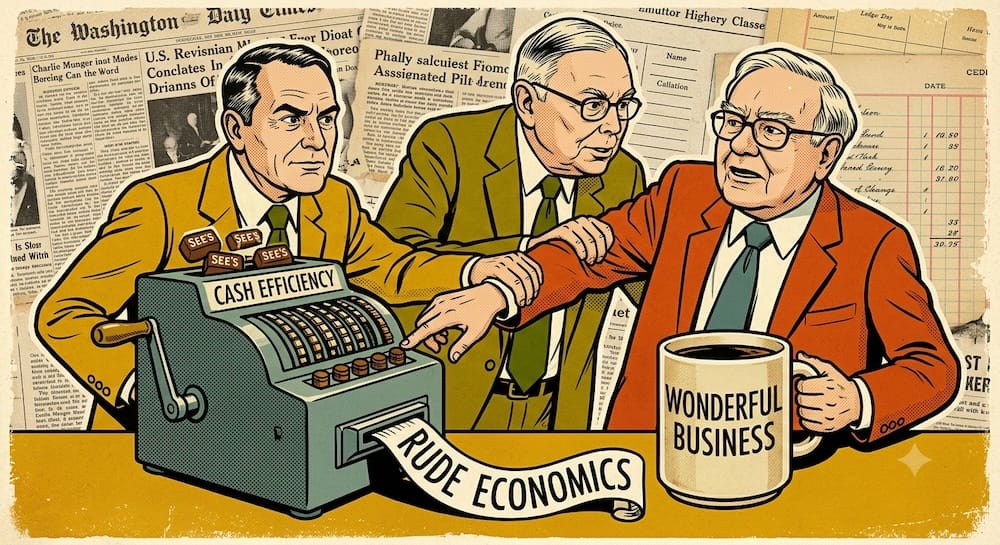

No quiero medir la influencia de Charlie Munger en Berkshire Hathaway contando las frases ingeniosas impresas en tazas de café. Así es como la…

I don’t want to measure Charlie Munger’s influence on Berkshire Hathaway by counting the aphorisms printed on coffee mugs. That is how finance people…

Yo no me compro esa idea de que Charlie Munger transformó a Warren Buffett de la noche a la mañana, pasando de ser un…

I don’t buy the idea that Charlie Munger turned Warren Buffett from a value investor into a quality investor. That sounds tidy, which is…

Me vuelvo un poco desconfiado cada vez que la gente de finanzas describe una sociedad comercial como una “armonía perfecta”. La armonía perfecta suele…

I get suspicious whenever finance people describe a business partnership as “perfect harmony.” Perfect harmony is usually what people say right before a room…

Me pongo un poco inquieto cada vez que los inversores transforman la asignación de activos en una guerra santa. La tribuna del “cigar-butt” (las…

I get twitchy whenever investors turn asset allocation into a holy war. The cigar-butt crowd acts like every highly profitable company is an overpriced…

La versión perezosa de la historia financiera dice que Charlie Munger le enseñó a Warren Buffett a comprar “empresas maravillosas”. Y yo lo admito:…

The lazy version of financial history says Charlie Munger taught Warren Buffett to buy “wonderful businesses.” I’ll admit it: “wonderful business” sounds nice. Too…

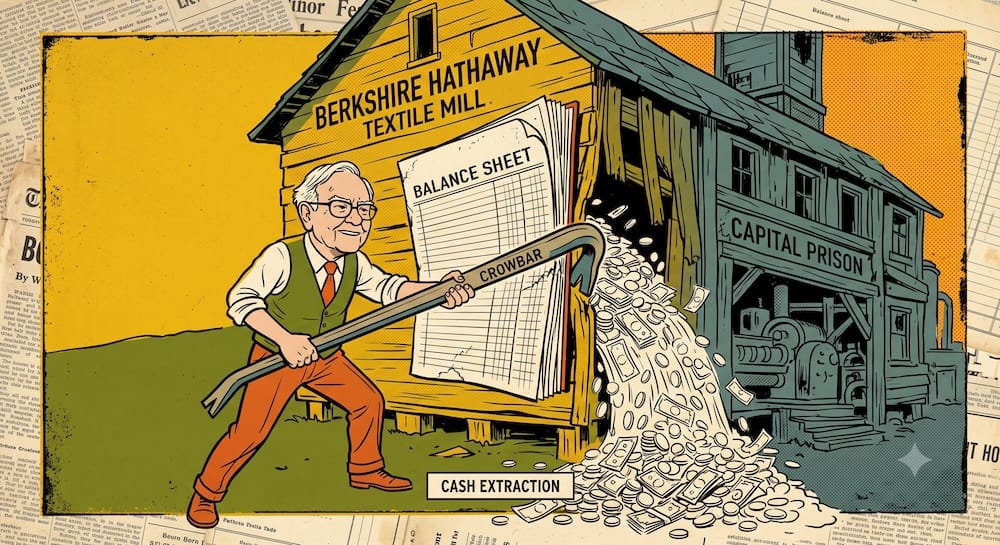

La oferta de compra por escrito llegó al escritorio de Warren Buffett en mayo de 1964 especificando un precio de $11.3125 por acción. Apenas…