I get twitchy whenever investors turn asset allocation into a holy war. The cigar-butt crowd acts like every highly profitable company is an overpriced scam, while the quality crowd behaves as if a famous consumer logo cancels out the laws of basic arithmetic. I have immense sympathy for both camps, which is deeply annoying because both camps also make me want to throw a calculator through a closed window.

The debate between cheap stocks and wonderful businesses is usually treated like a choice between rival religions. If you hang out in deep-value internet forums, you’re told that paying more than book value is a sin. If you scroll through modern financial social media, you’re told that valuation doesn’t matter as long as the company has a massive moat and a great product. Both sides can be right. Both sides can also be absolute clowns with spreadsheets.

The reality is that Warren Buffett and Charlie Munger did not simply replace cheap stocks with wonderful businesses. They didn’t have a warm spiritual awakening about branding. Instead, they learned through decades of capital allocation that cheapness and quality simply solve entirely different operational problems.

Cheap stocks can work beautifully when the asset discount is real, the underlying wealth can be monetized, and your capital base is small enough to play in the dark corners of the market. Wonderful businesses can work beautifully when high returns on tangible capital, real pricing power, and structural durability justify paying a premium over historical book value.

But let’s be entirely clear: cheapness without a catalyst or quality becomes a hostage situation, and quality without valuation discipline becomes expensive, un-holdable worship.

Cheap Stocks vs Wonderful Businesses Is Usually a Fake Debate

Cheap stocks can make you money. Wonderful businesses can make you money. Both can also set your portfolio on fire if you rely on the marketing slogan instead of the underlying business mechanism.

When I look at how the modern investing community splits down the middle on this topic, I see two tribes screaming past each other. The cigar-butt goblins underestimate structural business rot, and the quality crowd completely underestimates the gravity of valuation. Congratulations to everyone involved; you’ve found a way to lose money with absolute confidence.

To build an actual portfolio framework, we have to look directly at the trade-offs between these two distinct economic operating systems. They are not rival sports teams. They are completely different corporate mechanisms designed to extract cash from the market under specific structural constraints.

Cheap Stocks vs Wonderful Businesses Matrix

| Dimension | Cheap Stock Approach | Wonderful Business Approach | Samuel Verdict |

| Valuation Anchor | Net Current Asset Value (NCAV), Tangible Asset Liquidation Value | Earning Power, Future Return on Tangible Capital | Both valid; choose based on your asset scale. |

| Source of Return | Mean reversion of asset price to liquidation value, corporate action | Long-duration compounding of internal cash flow reinvestment | Goblins get paid once per trade; quality camp relies on a continuous engine. |

| Holding Period | Shorter-term (Typically 1 to 3 years or until asset realization event) | Long-term / Permanent (“Our favorite holding period is forever”) | Forever requires flawless operations; cheapness just requires a pulse or an exit. |

| Capital Needs | High capital intensity or dying operations requiring extraction | Capital-light expansion; low reinvestment required to grow | Give me the capital-light engine every single day. |

| Scalability | Extremely poor; capacity walls trap large pools of capital | High scalability; can absorb billions of dollars in mega-cap space | Small investors have choices; large institutions are forced into quality. |

| Failure Mode | Value trap; structural asset erosion; operational cash bleed | Overpayment; multiple contraction; competitive moat destruction | Both lead to the same dumpster fire, just different paths to get there. |

| Best Use Case | Small capital bases; highly inefficient, ignored micro-caps | Massive capital pools requiring long-term wealth preservation | Smaller capital bases have more room to hunt here; large institutions usually do not. |

What Buffett Learned From Cheap Stocks

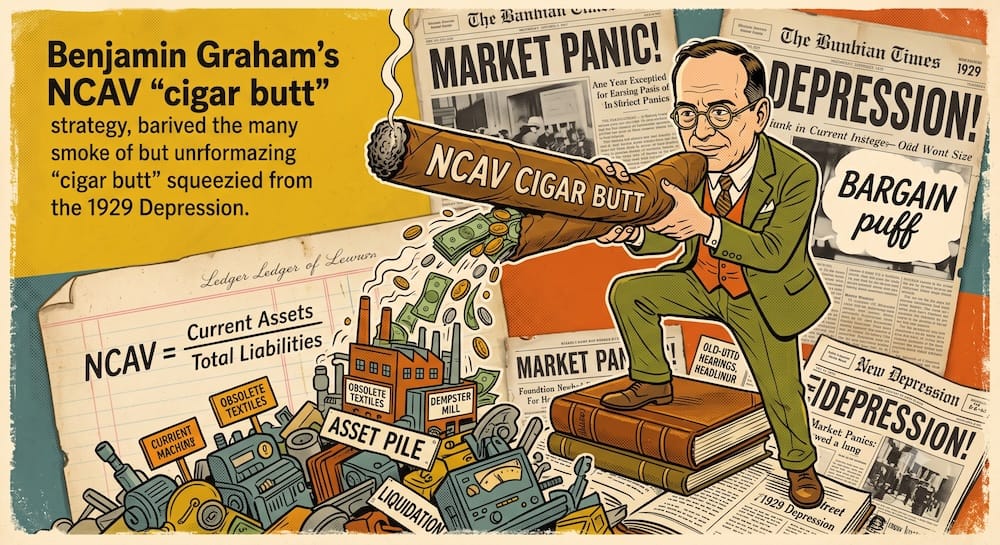

Warren Buffett spent the first fifteen years of his professional career running the Buffett Partnership Ltd. (1956–1969) as a pure Benjamin Graham quantitative disciple. He wasn’t looking for great companies. He was looking for statistically broken companies that were worth more dead than alive.

The logic of the Net Current Asset Value (NCAV) or “net-net” investment framework is beautifully simple: you calculate a company’s cash and short-term receivables, subtract all liabilities, and if the remaining liquid liquidation value is higher than the entire market capitalization of the equity, you buy it. You are effectively buying a dollar bill for sixty cents, with the physical plant, equipment, and inventory thrown into the deal completely for free.

This approach requires an investor to rely on structural diversification. You don’t buy one cigar butt; you buy a diversified group of them. You don’t care about the management, you don’t care about the product, and you certainly don’t plan on keeping them forever. You are just waiting for the market to realize its pricing error, or for a corporate liquidation event to unlock the cash.

During this early era, Buffett divided his portfolio into categories like “Workouts” (corporate arbitrage, spin-offs, and liquidations) and “Controls” (where he acquired enough voting stock to manually force corporate action).

Consider the Sanborn Map Co. investment in 1958. Sanborn produced highly detailed municipal maps for insurance underwriting, but the underlying business was dying. However, over the years, the company had built an internal investment portfolio worth roughly $65 per share, while the entire stock was trading on the open market for around $45 per share.

Buffett didn’t buy Sanborn because he loved maps. He bought roughly 35% of the company because he saw a clear asset discount. He then used his voting block to force an activist separation, separating the investment portfolio from the core mapping business and delivering the underlying asset value straight back to his partnership. This was pure, unadulterated Graham value investing: finding an asset mismatch, forcing an exit, and running away with the cash.

When Cheap Stocks Work

Let’s be fair to the cigar-butt goblins: this quantitative framework works under very specific, non-negotiable structural parameters. It is not a broken philosophy; it is a highly constrained mechanism that requires four specific things to go right:

- The Discount Is Real and Realizable: The assets on the balance sheet cannot be phantom inventory or obsolete machinery that melts away during a forced sale. Cash, short-term bonds, and unencumbered real estate are real; a factory that only builds vacuum tubes is an illusion.

- The Underlying Cash Burn Is Zero or Low: A cheap stock only works if the business isn’t actively consuming its own asset base to stay alive. If a company is losing massive cash in operations, that beautiful margin of safety on the balance sheet is evaporating every single week you hold the equity.

- There Is a Concrete Exit or Activist Catalyst: You must have a path to value realization. Either the market corrects its pricing anomaly within a 12-to-36 month window, another firm initiates a corporate takeover, or you possess enough capital to take control of the board and force a liquidation or asset distribution.

- Your Capital Base Is Small: This is the ultimate capacity wall. During the late 1950s, Buffett could achieve spectacular alpha because he was moving small amounts of partnership capital into tiny, illiquid micro-caps. Smaller capital pools can operate freely in this space. If you are managing immense institutional scale, you cannot buy a micro-cap net-net without buying the entire company three times over and moving the stock price directly against your own orders.

When Cheap Stocks Turn Into a Dumpster Fire

The trouble begins when retail value investors forget these rules and assume that a low Price-to-Book (P/B) ratio or a single-digit Price-to-Earnings (P/E) multiple makes an asset safe.

A cheap stock with a fundamentally broken business attached is not a bargain. It is a financial raccoon living inside your walls. You think you bought cheap assets; in reality, you just bought a lifetime of ongoing repairs and operational capital destruction.

The ultimate historical example of this value trap is Berkshire Hathaway itself. When Buffett began buying shares of the New England textile conglomerate in 1962, it was a textbook cigar butt. The stock was trading below its working capital value per share, and every time the company closed a mill, it generated surplus cash that could be used to buy back stock. It looked like a neat quantitative arbitrage play.

But once Buffett took control of the corporate structure in 1965, he found himself trapped inside a structurally broken industry. The textile mills possessed zero pricing power; they were selling a commoditized product against low-cost international competitors. To keep the business alive, the mills required continuous injections of maintenance capital expenditure (capex) just to remain operational.

┌────────────────────────────────────────────────────────┐

│ THE CIGAR-BUTT HANGOVER SYSTEM │

└────────────────────────────────────────────────────────┘

│

▼

┌────────────────────────────────────────────────────────┐

│ Acquire Broken Business Below Book │

└────────────────────────────────────────────────────────┘

│

┌─────────────┴─────────────┐

▼ ▼

┌───────────────────────────┐┌───────────────────────────┐

│ Zero Pricing Power ││ High Reinvestment Demands │

│(Cannot pass costs down) ││(Maintenance Capex Drain) │

└───────────────────────────┘└───────────────────────────┘

│ │

└─────────────┬─────────────┘

│

▼

┌────────────────────────────────────────────────────────┐

│ Operational Capital Destruction │

│ (Cash is consumed just to stay in place) │

└────────────────────────────────────────────────────────┘

Every dollar poured into new looms or modernizing the factories produced a low return on tangible capital. Buffett spent twenty painful years pumping capital into those textile looms before finally shutting down the operations entirely in 1985.

This is the cigar-butt hangover. If a business has terrible economics, time is the absolute enemy of your portfolio. If you hold a bad business for ten years, your ultimate return will match the dismal internal return of that business, no matter how cheap the price was when you originally bought it.

What Munger Changed About Wonderful Businesses

Charlie Munger stepped into this framework and forced a critical strategic pivot. He shifted the central question of corporate analysis away from Graham’s focus on historical balance sheet values. This is where I think Munger earned his keep. He did not make Buffett more romantic; he made him more demanding.

Munger’s upgrade was simple: stop asking “What are the physical assets worth right now if we close the doors?” and start asking “What can this corporate engine keep producing in clean cash flow over the next twenty years?”

This strategic shift required a total re-evaluation of corporate quality metrics:

- High Return on Tangible Capital: A wonderful business is one that can generate massive pre-tax profits while utilizing minimal physical assets. If a company requires huge amounts of factories, trucks, and inventory to make a meager profit, it’s an asset-heavy grind. If it can make immense profit using minimal physical assets, it’s a high-return cash machine.

- Pricing Power and Economic Goodwill: True quality means possessing a consumer franchise that allows you to raise prices without losing sales volume to generic alternatives. This structural advantage represents “economic goodwill”—an intangible asset that rarely shows up accurately on a traditional balance sheet but drives real economic outperformance.

- Low Capital Reinvestment Needs: The ultimate business is a cash generator, not a cash consumer. It can expand its operations without needing to plow every single dollar of profit back into building new infrastructure or replacing depreciated equipment. This frees up massive pools of unencumbered cash.

- Long-Term Durability: A competitive moat is only useful if it is durable. High returns on capital naturally attract massive competition. A wonderful business must possess a structural barrier—whether through brand dominance, scale advantages, or high switching costs—that stops those competitors from eroding its profit margins over a multi-decade time horizon.

Munger didn’t tell Buffett to abandon price discipline or start buying expensive equities. He simply told him to stop buying dying companies that required a permanent corporate feeding tube just to survive the quarter.

When Wonderful Businesses Work

The classic proof-case for this quality transition is See’s Candies, acquired by Berkshire Hathaway in 1972 for a total cash outlay of $25 million.

At the time of purchase, See’s only possessed roughly $8 million in net tangible assets on its balance sheet. Paying $25 million meant paying three times book value—an absolute outrage to traditional Graham-style value purists. I understand why Graham purists hated this kind of deal. Paying three times book for candy sounds insane if your entire religion is built around liquidation value. But let’s look at the actual underlying corporate arithmetic that justified the premium:

┌────────────────────────────────────────────────────────┐

│ THE SEE'S CANDIES CASH ENGINE (1972) │

└────────────────────────────────────────────────────────┘

│

┌──────────────────────┴──────────────────────┐

▼ ▼

┌───────────────────────────┐ ┌───────────────────────────┐

│ Net Tangible Assets: $8M │ │ Pre-Tax Earnings: $4M │

└─────────────────────────┬─┘ └─┬─────────────────────────┘

│ │

▼ ▼

┌─────────────────────────────────────┐

│ ~50% Pre-Tax Return on Assets │

└──────────────────┬──────────────────┘

│

▼

┌─────────────────────────────────────┐

│ STRUCTURAL OUTCOME │

│ Reallocatable Cash Flows │

└─────────────────────────────────────┘

See’s Candies was generating roughly $4 million in pre-tax profits on that tiny $8 million asset base. This meant the business was operating at an astronomical 50% pre-tax return on tangible capital. Furthermore, because of its immense brand loyalty, See’s possessed incredible pricing power. See’s could raise prices over time without destroying demand, which helped it protect earning power during inflationary periods.

Because the business only needed minimal physical capital to expand, a large portion of the cash generated by the business could be distributed upward after taxes and operating needs. By the 2010s, See’s had generated over $2 billion in cumulative cash flow that Buffett could systematically reallocate elsewhere.

Paying above historical book value is not automatically reckless. If a company can reliably compound capital at a massive internal return without needing massive reinvestment, paying a premium for that cash engine is incredibly cheap over a long-duration horizon. The wonderful-business crowd loves the See’s story. Fair. But they often forget the annoying little detail: the price still had to make sense.

When Wonderful Businesses Become Expensive Worship

But this is exactly where the modern quality crowd gets into deep trouble. They look at See’s Candies or Coca-Cola and assume that if a business is considered “wonderful,” you can pay any price you want and let time fix your valuation errors.

This is the point where investors start lighting incense in front of a famous consumer logo and calling it a discounted cash flow analysis. Quality worship is a silent killer of modern portfolio returns.

High corporate quality can easily be overpaid. If you buy an incredible business at 50 or 60 times earnings, you are pricing decades of absolute perfection into the stock. Even if the company executes its operational strategy flawlessly, your ultimate investment return can still underperform the market due to massive multiple contraction—the slow, painful normalization of an inflated valuation multiple back down to earth.

Worse, moats can erode far faster than the quality cult likes to admit. High Return on Invested Capital (ROIC) is a beacon for disruption; it tells every smart competitor in the world that there is a massive pool of profit to be captured. Over long horizons, economic returns have a brutal tendency to mean-revert toward the cost of capital.

┌────────────────────────────────────────────────────────┐

│ THE EXPENSIVE WORSHIP TRAP │

└────────────────────────────────────────────────────────┘

│

▼

┌────────────────────────────────────────────────────────┐

│ Pay Extreme Multiple for Famous Logo │

└────────────────────────────────────────────────────────┘

│

┌─────────────┴─────────────┐

▼ ▼

┌───────────────────────────┐┌───────────────────────────┐

│ Multiple Contraction ││ Moat / Margin Erosion │

│(Valuation gravity reverts)││(Competition hits ROIC) │

└───────────────────────────┘└───────────────────────────┘

│ │

└─────────────┬─────────────┘

│

▼

┌────────────────────────────────────────────────────────┐

│ Underperformance / Loss │

│ (The premium paid devoured the returns) │

└────────────────────────────────────────────────────────┘

Even Buffett has fallen into this specific trap when he let his admiration for quality cloud his mathematical guardrails. Consider his 1993 acquisition of Dexter Shoe. He saw what he believed was a fantastic domestic manufacturing brand with a durable competitive moat. He was so confident in the quality of the business that he paid $433 million for it, using Berkshire Hathaway stock rather than cash.

Within years, the competitive advantage of domestic shoe manufacturing was completely obliterated by low-cost foreign competition. The moat didn’t just leak; it vanished. Because Buffett paid for a temporary illusion of quality using permanent Berkshire shares, the mistake permanently diluted his shareholders’ ownership of Berkshire’s future compounding cash flows, costing them billions of dollars in long-term opportunity cost.

Buffett and Munger’s Real Answer

The ultimate takeaway from studying the evolution of Berkshire Hathaway is that Buffett and Munger never abandoned Benjamin Graham’s core price discipline. Munger did not teach Buffett to forget about value; he taught him to re-evaluate what constitutes true value.

The correct corporate framework is not cheap or wonderful. The answer lies in the intersection of both dimensions: the business must be good enough to survive, and the underlying price must be low enough to forgive your own short-term stupidity.

To see how these different pieces fit together across a multi-decade career, we have to look directly at the case studies where the mechanics succeeded or failed:

Case Study Matrix

| Case Study | Cheap or Wonderful? | What Worked Inside the Trade | What Broke / The Core Risk | The Core Mechanical Lesson |

| Sanborn Map Co. (1958) | Cheap | Massive asset discount; underlying investment portfolio was worth more than total market cap. | Dying core business; required aggressive activist control to unlock the assets. | Asset plays work if you can manually force an exit or a liquidation event. |

| Berkshire Hathaway Textile (1965) | Cheap | Stock traded below working capital; early cash generation from mill closures allowed share buybacks. | Commoditized industry with zero pricing power; high maintenance capex requirements. | A cheap stock with bad business economics is an ongoing capital destruction trap. |

| See’s Candies (1972) | Wonderful | Astronomical 50% pre-tax ROIC; incredible consumer pricing power to outrun macro inflation. | Required paying 3x book value, which broke traditional value dogma at the time. | High return on tangible capital justifies paying a premium over historical book value. |

| Coca-Cola (1988) | Wonderful | Global brand, capital-light model, durable pricing power, and growing dividends to Berkshire. | Multiple contraction risk if purchased at an inflated valuation peak. | Moats are incredibly powerful when backed by international scalability. |

| Dexter Shoe (1993) | Wonderful (Fake) | Strong historical domestic brand name and stable localized earnings profile. | Moat was instantly destroyed by systemic shifts in globalized trade and foreign competition. | Overestimating a moat and paying with your own valuable stock results in permanent dilution. |

What Modern Investors Misread

Modern retail investors frequently look at Berkshire Hathaway’s historical public portfolio—dominated by multi-billion dollar mega-cap allocations like Apple—and conclude that they should simply buy 3 or 4 massive, famous consumer tech stocks and sit on their hands forever.

This is a complete misreading of the cheap-to-quality evolution. It mistakes a structural limitation for an ideal investment strategy. Berkshire concentrates in mega-caps today because its massive asset scale leaves it with a much narrower opportunity set. It cannot operate in the high-alpha inefficient spaces that built the foundation of its wealth.

Smaller investors may be able to study parts of the market Berkshire can no longer touch: ignored small-caps, illiquid situations, and strange market anomalies. You have the freedom to look into both the cigar-butt lane and the premium quality lane.

But to execute either strategy safely, you have to look past the surface-level metrics and ask better structural questions before committing capital:

False Signal Matrix

| Looks Smart on Paper | Hidden Real-World Trap | The Better Structural Question |

| Low Price-to-Book (P/B) | The book value consists of obsolete assets or inventory that cannot be liquidated at face value. | If this business goes into a tailspin tomorrow, what can these physical assets actually be sold for? |

| Low Price-to-Earnings (P/E) | Cyclical peak earnings that are about to revert, or a dying company burning cash behind the scenes. | Is this cash flow sustainable, or am I looking at a temporary cyclical high right before a structural drop? |

| Famous Consumer Brand | The brand name is popular, but it possesses zero real pricing power or ability to pass costs onto consumers. | Can this company raise prices meaningfully over time without losing core customers? |

| High Return on Assets (ROIC) | The current high return is driven by a temporary technological anomaly that will attract intense competition. | What concrete structural barrier stops a competitor from copying this exact model and undercutting margins? |

| High Gross Profit Margins | The high margins are completely devoured by massive corporate overhead, debt service, or continuous capex. | How much of that beautiful gross margin actually drops down into free, unencumbered cash flow for shareholders? |

| Buying at a “Fair Price” | Using “fair” as an excuse to overpay for a popular stock that has zero safety cushion built in. | Does my investment thesis require absolute operational perfection for the next ten years to break even? |

| Permanent Holding Period | Blindly holding an asset through structural regime changes while its competitive advantages fade. | Am I holding this security because the underlying business engine is compounding, or am I just emotionally attached? |

I like high-quality companies. I also like paying sane prices for those companies. I realize this shouldn’t be a wild, revolutionary concept, but spend ten minutes in any online investor community and you’ll find people treating valuation discipline like an outdated relic of the 1930s.

If your entire asset allocation thesis depends on the word “wonderful” doing 100% of the heavy lifting while you ignore basic arithmetic, your portfolio is eventually going to get dragged back to reality by valuation gravity. Don’t turn corporate strategies into a dogmatic religion. Look at the assets, look at the cash engine, keep your price discipline at the door, and make sure you build a framework that doesn’t rely on absolute perfection to survive the storm.

Educational Trade-Off Note: Concentrating a portfolio into individual equities, micro-cap value opportunities, or high-premium quality securities introduces significant unsystematic, operational, and valuation risks. This analysis functions exclusively as a historical deconstruction of corporate capital allocation frameworks and does not constitute financial advice or a prescription to buy, sell, or hold any individual security or asset class.

What is the core difference between a cheap stock and a wonderful business?

The difference boils down to asset value versus earning power. A cheap stock represents an asset play, often trading below its liquidation or working capital value, where you profit from a short-term price correction or corporate catalyst. A wonderful business relies on long-duration compounding, utilizing high returns on tangible capital and durable pricing power to generate continuous cash flow that justifies paying a valuation premium over book value.

Why did Warren Buffett stop buying Graham-style cheap cigar-butt stocks?

It was driven by a capacity wall, not a spiritual awakening. As Berkshire Hathaway’s capital base scaled past millions into billions of dollars, the investable universe contracted sharply. Buffett could no longer achieve meaningful outperformance by moving immense capital into illiquid micro-caps without driving the stock prices directly against his own trades. He was logistically forced into large-cap space where only wonderful businesses could absorb that scale.

Can a retail investor still use the cheap stock framework successfully today?

Yes, smaller capital bases have more room to hunt here; large institutions usually do not. Because you are managing an independent portfolio rather than billions of institutional dollars, you can study parts of the market that Berkshire can no longer touch, such as ignored small-caps, illiquid situations, and strange market anomalies. However, you must ensure the asset discount is real and that the company isn’t actively consuming its own capital to stay afloat.

How do you spot a cheap stock that is actually a dangerous value trap?

Look at the structural business rot and ongoing cash burn. A cheap stock becomes a financial raccoon inside your walls when it possesses zero pricing power and requires continuous maintenance capital expenditure just to remain operational. If a business has terrible underlying economics and generates a low return on tangible capital, holding it for a long period ensures your investment returns will pull downward to match that dismal internal return, regardless of how cheap it looked at purchase.

Does buying a wonderful business mean valuation no longer matters?

Absolutely not. Quality worship is a silent killer of modern portfolio returns. If you pay an extreme valuation multiple for a famous consumer brand, you are pricing decades of absolute perfection into the stock. This leaves your portfolio highly vulnerable to multiple contraction, where the valuation gravity eventually pulls an inflated multiple back down to earth, devouring your long-term compounding returns even if the company executes its strategy flawlessly.

What did Charlie Munger mean by economic goodwill?

He meant the intangible competitive advantages that rarely show up accurately on a traditional historical balance sheet. Economic goodwill represents things like intense brand loyalty, customer switching costs, or scale advantages that grant a company real pricing power. This mechanism allows a company to raise prices meaningfully over time without losing its core customer volume to generic competitors, driving high returns on assets without heavy capital reinvestment.

How can an independent investor safely combine value and quality without picking individual stocks?

You look at the underlying systematic factors rather than picking individual tickers. Instead of attempting to guess which specific consumer logo will maintain a permanent economic moat over the next thirty years, investors can study systematic, low-cost index products engineered to target the dimensions of quality, value, and low volatility across diversified baskets of liquid securities. This captures the broad financial premiums while entirely expelling the unsystematic risk of a single corporate blowup.

This article is also available in Spanish. Leé la versión en castellano: Warren Buffett y Charlie Munger sobre empresas maravillosas frente a acciones baratas