The research paper “The Allegory of the Hawk and Serpent” is a useful starting point for understanding the portfolio-construction logic behind the Dragon Portfolio. The Artemis paper is an excerpt from the firm’s January 2020 letter to investors, and it frames the problem as a 100-year wealth-preservation challenge while testing portfolios across historical data dating back to 1928. This matters because the Dragon Portfolio discussed here is a research framework and asset-allocation concept, not a single ETF, mutual fund, or audited live product track record that a reader can simply buy off the shelf. To my eyes, the useful part is not the dragon mythology; it is the uncomfortable mechanical question underneath it: what actually protects a portfolio when the regime changes and yesterday’s diversifier stops diversifying?

The Cyclical Nature of Markets

The research underscores the cyclical nature of markets, driven by an interplay of various factors like demographics, technological advancements, and geopolitical shifts. These cycles have historically shown significant impacts on investment returns, leading to the realization that traditional investment strategies might not be as effective in surviving those regime shifts.

Limitations of Traditional Portfolio Management

One of the key highlights of the paper (written by Chris Cole of Artemis Capital Management) is its critique of conventional portfolio management strategies. It points out that these traditional approaches, often heavily reliant on a static stock-bond mix, are not equipped to handle the complexities and variabilities of different economic regimes. This leads to an increased risk of underperformance, especially during unexpected market downturns or periods of high volatility.

What I found most useful in the original Artemis framing is that it does not treat “diversification” as a decorative word. It asks whether the portfolio actually owns assets that can respond to secular growth, deflationary deleveraging, inflationary pressure, and volatility shocks. That is a different animal from owning ten funds that all quietly depend on the same growth cycle.

Introduction to the Dragon Portfolio Concept

The Dragon Portfolio is one proposed answer to these limitations. Named after the mythical creature used here as shorthand for durability across regimes, the Dragon Portfolio is designed to withstand and prosper through various economic climates. It proposes a diversified mix of assets, balancing growth-oriented investments like equities with protective assets such as commodities and trend-following instruments. The point is not that every sleeve works all the time. The point is that different sleeves are expected to earn their keep in different environments, which makes rebalancing the engine rather than an afterthought.

source: Real Vision on YouTube

About the Author & Disclosure

Picture Perfect Portfolios is the quantitative research arm of Samuel Jeffery, co-founder of the Samuel & Audrey Media Network. With over 15 years of global business experience and two World Travel Awards (Europe’s Leading Marketing Campaign 2017 & 2018), Samuel brings a unique global macro perspective to asset allocation.

Note: This content is strictly for educational purposes and reflects personal opinions, not professional financial advice. All strategies discussed involve risk; please consult a qualified advisor before investing.

These asset allocation ideas and model portfolios presented herein are purely for entertainment purposes only. This is NOT investment advice. These models are hypothetical and are intended to provide general information about potential ways to organize a portfolio based on theoretical scenarios and assumptions. They do not take into account the investment objectives, financial situation/goals, risk tolerance and/or specific needs of any particular individual.

Objective of the Dragon Portfolio

The overarching objective of the Dragon Portfolio is to pursue long-horizon compounding while reducing dependence on one dominant macro regime. By diversifying across different asset classes that respond uniquely to various economic phases, the portfolio aims to reduce single-regime fragility and potentially improve the path of returns, across a wider range of market environments.

In essence, the Dragon Portfolio presents a broad and adaptable investment strategy, built around the fact that markets cycle through growth, inflation, deflation, crisis, and recovery. Its approach moves beyond traditional stock-bond methodology, offering a more dynamic and resilient way of asset allocation that is especially pertinent in a world where inflation, liquidity, rates, and equity valuations can all change the portfolio math. The strategy is less about promises and more about trade-offs: accepting drag from defensive sleeves in exchange for better odds of having something useful to rebalance when the growth sleeve is under stress.

Who Created The Dragon Portfolio?

The Dragon Portfolio is a concept that was popularized and developed by Chris Cole, the Chief Investment Officer (CIO) and founder of Artemis Capital Management. Chris is a recognized figure in finance and investment, particularly known for his research and work on volatility, risk management, and alternative investment strategies. He introduced the Dragon Portfolio as an approach to all-weather asset allocation and risk mitigation in investment portfolios.

Conceptual Foundation of the Dragon Portfolio

The Allegory of the Hawk and Serpent: Philosophical Underpinnings

The Dragon Portfolio’s conceptual roots are embedded in the allegory of the hawk and serpent, a metaphor representing the tension between secular growth and secular change. In the paper’s language, the Serpent represents the growth cycle: value creation, rising asset prices, favorable demographics, technological progress, globalization, and expanding liquidity. The Hawk represents the forces that challenge or destroy that cycle, whether through deflationary deleveraging or inflationary debasement.

- The Serpent: This typically represents more traditional, liquid growth investments like stocks and bonds. These assets are characterized by their responsiveness to economic growth and are generally more familiar to most investors.

- The Hawk: This represents assets that are designed to perform well during periods of economic stress or market volatility. This could include investments like gold, long volatility strategies, and perhaps even certain types of trending commodities.

The idea is that by balancing these two types of investments (the Serpent and the Hawk), the Dragon Portfolio aims to achieve long-term growth while also being resilient during times of economic turbulence. But the real lesson is less poetic than that. A portfolio built only for good weather can look brilliant for decades, and then suddenly reveal that all of its “diversification” was just different flavors of the same macro bet.

Philosophical Significance in Investment Strategy

The allegory serves as more than a symbolic representation; it provides a framework for understanding market behavior. By personifying the elements of growth and defense, the allegory encourages investors to embrace a holistic view of asset allocation. This perspective is critical in developing a portfolio that can balance seeking growth with protecting capital.

The Cyclical Nature of Wealth: Creation, Destruction, and Rebirth

Central to the Dragon Portfolio is the concept of the economic cycle, which involves phases of wealth creation, destruction, and rebirth. This cyclical view acknowledges that economic environments are not static; they evolve through periods of expansion, peak, contraction, and trough. The paper illustrates how different asset classes perform variably across these cycles, highlighting the importance of a diversified portfolio that can adapt to these changes.

Wealth Creation and Growth Phase

In the growth phase of the cycle, characterized by economic expansion and bullish markets, growth assets like equities tend to perform well. However, relying solely on such assets can be precarious, as they are vulnerable to market downturns and to long periods where valuations, inflation, or rates change the math.

Wealth Destruction and Defensive Strategy

Conversely, during downturns and recessions, defensive assets like bonds and commodities can offer better protection depending on the nature of the downturn. This phase underscores the importance of including assets in the portfolio that can counterbalance the volatility of growth-oriented investments. Honestly, this is where most elegant portfolios get exposed. The diversifier that looked unnecessary during the boom suddenly becomes the thing you wish you had sized properly.

Rebirth and Dynamic Adaptation

The rebirth phase is about adapting to the new economic realities post-recession. This involves rebalancing the portfolio to align with the emerging economic environment, ensuring that it remains resilient and positioned for growth. Rebalancing is not just spreadsheet hygiene here. It is the mechanism that turns crisis performance from one sleeve into dry powder for another.

In essence, the Dragon Portfolio, through its philosophical grounding in the allegory of the hawk and serpent, provides a more advanced approach to investment strategy. It emphasizes the need for a dynamic, adaptable asset allocation that can thrive across the cyclical nature of wealth creation, destruction, and rebirth. This approach helps in mitigating risks associated with economic fluctuations while creating a clearer framework for growth and defense.

Secular Growth and Decline: Understanding the Market Cycles

Analyzing Past Market Trends and Cycles

A critical aspect of the Dragon Portfolio is its deep dive into historical market trends and cycles. This analysis spans over a century, providing a wide view of how markets have evolved through various economic phases. The research paper examines these patterns, identifying recurring themes and shifts that have shaped the financial structure.

The Role of Demographics in Market Trends

Demographics play a significant role in shaping market trends. Changes in population dynamics, such as aging populations or shifts in workforce demographics, directly influence economic growth and consumer behavior. The Dragon Portfolio takes into account these demographic trends, understanding that they can significantly impact investment outcomes, particularly in long-term strategies.

source: RCM Alternatives on YouTube

Technological Advancements and Their Impact

Technology is another critical factor influencing market cycles. Innovations and technological breakthroughs can drive economic growth and create new investment opportunities. However, they can also disrupt existing industries and render traditional business models obsolete. The Dragon Portfolio considers these technological shifts, recognizing their potential to both support growth while destroying old assumptions.

Economic Factors Shaping Market Trends

Economic policies, interest rates, inflation, and global trade are among the key economic factors that influence market cycles. The Dragon Portfolio incorporates an understanding of these elements, recognizing how they can create environments of prosperity or adversity for different asset classes. This is the part I like most: the portfolio is not pretending to forecast the next regime perfectly. It is asking what happens if the forecast is wrong.

Integration of Market Cycle Analysis in the Dragon Portfolio

The Dragon Portfolio uses this detailed analysis of past market trends, demographics, technology, and economic factors to formulate a strategy that is not only reactive but also anticipatory of future market movements. This approach allows for a dynamic asset allocation that adjusts to the secular trends of growth and decline, aiming to capitalize on opportunities while reducing risks.

The Dragon Portfolio’s approach to understanding and utilizing market cycles is broad and regime-aware. By analyzing historical trends and considering the impact of demographics, technology, and economic factors, the strategy seeks to navigate through the complexities of secular growth and decline. This deep understanding of market dynamics is useful when building an allocation that can bend without breaking.

Challenges in Traditional Portfolio Management

The Paradigm of Traditional Investing Assumptions

Traditional portfolio management is predicated on a set of long-standing assumptions that have shaped mainstream investment practices. Central to these is the belief in equities for long-term growth, often overlooking the possibility of extended market downturns. Similarly, fixed-income instruments like bonds are traditionally viewed as havens of stability, yet they can falter in environments of low interest rates or inflation, leading to the erosion of real returns.

The Equity Dominance Fallacy

In traditional investing, there can be overconfidence in equities as the cornerstone of growth, especially over long periods. This belief, however, is frequently challenged during bear markets, where equity-heavy portfolios can experience substantial value erosion. Such scenarios contrast with the conventional wisdom that equities are always safe over long horizons.

Fixed Income in Low-Yield Contexts

The role of fixed income in portfolio stability is another cornerstone of traditional strategies. However, in eras of low interest rates, the yield on these instruments can be insufficient, failing to keep pace with inflation, and thus offering negative real returns. This challenge is particularly pronounced in stagnant or inflationary economic climates.

Misconceptions Around Diversification

A common trope in traditional portfolio management is the reliance on diversification as a risk mitigation tool. However, the assumption that asset classes remain non-correlated in all market conditions is often disproved during times of financial crises, where increased correlations can lead to simultaneous losses across diversified assets.

Reliance on Historical Performance

Many traditional investment strategies are built on historical performance data, assuming that past patterns will predict future market behaviors. This backward-looking approach can be myopic, particularly in the face of unprecedented market disruptions or paradigm shifts in the global economy. Backtests can be useful. But they are not a personality transplant. The investor still has to hold the ugly sleeve when the backtest is not currently flattering.

Inflation Risks and Portfolio Erosion

Another critical oversight in traditional portfolio management is underestimating the impact of inflation, particularly in portfolios with a heavy emphasis on fixed-income assets. Over time, inflation can significantly diminish the purchasing power of returns, eroding the real value of the portfolio.

The Imperative for a Dynamic Investment Approach

These various challenges underscore the case for a more dynamic and nuanced approach to portfolio management. Traditional models, with their static assumptions and reliance on historical trends, can be ill-equipped for the complexities and volatility of modern financial markets.

Summary: Pitfalls in Different Market Regimes

- Equity-Dominated Portfolios in Bear Markets: In bear markets, portfolios heavily weighted in equities can suffer significant losses. This is contrary to the common assumption of equities being safe for long-term investment.

- Fixed Income in Low-Yield Environments: The traditional safe haven of bonds and other fixed-income securities becomes problematic in low-yield environments, particularly when inflation is factored in, leading to negative real returns.

- Diversification Misconceptions: Traditional diversification strategies often assume a lack of correlation between asset classes. However, in extreme market conditions, this correlation can increase, leading to simultaneous losses across supposedly diversified portfolios.

- Overreliance on Historical Performance: Many traditional strategies rely heavily on back-tested data and historical performance, which may not accurately predict future market behavior, especially in unprecedented scenarios.

- Inflation Risk: Traditional portfolios, especially those heavy in fixed-income assets, can be vulnerable to inflation, eroding the real value of returns.

The Dragon Portfolio, through its approach, addresses the shortcomings of traditional portfolio management by advocating for an adaptive, forward-looking strategy. This approach recognizes the limitations of conventional wisdom and historical patterns, emphasizing the need for a portfolio that is resilient and responsive to the multifaceted nature of global financial markets.

The Dragon Portfolio: A Century-Long Portfolio Framework

The Dragon Portfolio presents an ambitious approach to asset allocation, designed to think across an extended period, typically spanning a century. It breaks away from traditional investment strategies, offering a diversified and balanced allocation of assets that strategically adapts to varying market conditions. This portfolio strategy is not merely a collection of different asset types; it is a methodical approach that responds to the dynamics of global economic and market cycles.

Philosophical Underpinning of the Dragon Portfolio

The foundation of the Dragon Portfolio lies in understanding the cyclical nature of markets and economies. It is premised on the idea that financial markets are not linear or predictable in the long term but are instead characterized by phases of growth, stagnation, and decline. The portfolio is structured to not only survive but also thrive in each of these phases.

source: Mutiny Funds on YouTube

Diversification Beyond Traditional Norms

Diversification in the Dragon Portfolio extends beyond the conventional stock and bond mix. This diversification is not arbitrary; it is a deliberate strategy to ensure that different components of the portfolio respond differently to various market conditions, thereby reducing overall risk. The real test is not how many sleeves exist. The real test is whether those sleeves behave differently when the portfolio needs them most.

Incorporating Counter-Cyclical Assets

A distinctive feature of the Dragon Portfolio is its emphasis on counter-cyclical assets. These are assets that tend to perform differently from the general market trend. For instance, certain commodities or alternative assets may rise in value when traditional markets decline, providing a hedge against downturns. This counter-cyclical approach is crucial in stabilizing the portfolio during periods of market volatility and economic downturns.

The Importance of Adaptability and Rebalancing

The Dragon Portfolio is dynamic, not static. It requires regular rebalancing to adjust to changing market conditions. This adaptability is key to its long-term success. It involves periodically reviewing and adjusting the asset mix to ensure that the portfolio remains aligned with the overarching strategy of balancing growth potential with risk mitigation.

The Dragon Portfolio is a forward-thinking investment strategy designed for longevity and resilience. Its multi-faceted approach to diversification, inclusion of counter-cyclical assets, and emphasis on adaptability make it a unique framework for thinking about sustainable growth and wealth preservation over an extended time horizon. But the rebalancing point is where the theory meets the investor’s stomach. Selling what has worked and adding to what looks broken is not easy. That is not a side issue. That is the mechanism.

Composition of the Dragon Portfolio

The Dragon Portfolio’s allocation is where the concept becomes testable. The idea is not just to own many different things. The idea is to own exposures that answer different macro questions: What grows when risk appetite is rewarded? What helps when rates fall? What holds value when money loses purchasing power? What can respond to trend and crisis? What can become convex when the rest of the portfolio is bleeding?

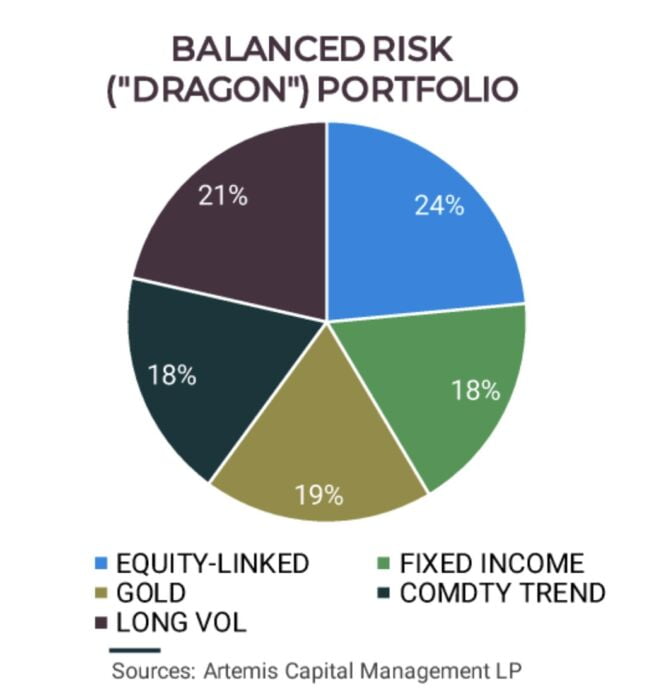

In the Artemis paper, the balanced Dragon mix is presented as 24% equity-linked assets, 18% fixed income, 19% physical gold, 18% commodity trend following, and 21% active long volatility. That exact blend is important because the paper is not merely saying “add some alternatives.” It is sizing the defensive and diversifying sleeves aggressively enough to matter. Tiny diversifier positions can make an investor feel clever, but they often do not move the portfolio needle when the real storm arrives.

Dragon Portfolio: Asset Classes and Their Allocation

- Equities (24% Allocation): Equities form a vital segment of the Dragon Portfolio, constituting approximately 24% of the total allocation. This segment primarily includes stocks from a broad spectrum of sectors and geographies, offering growth potential and a hedge against inflation. Equities are central for capital appreciation, especially in bullish market phases.

- Long-Term Bonds (18% Allocation): A similar proportion is allocated to long-term bonds, typically government securities with extended maturities. These instruments provide a stabilizing counterbalance to the portfolio, offering predictable income and preservation of capital. In periods of declining interest rates, these bonds can deliver substantial capital gains, thereby cushioning the portfolio against equity market downturns.

- Gold (19% Allocation): The Dragon Portfolio allocates around 19% to gold, a classic hedge against inflation and currency devaluation. Gold’s historical role and sometimes-low correlation with traditional financial assets make it an important component for hedging against systemic risks and financial crises.

- Commodities (18% Allocation): Another 18% is allocated to commodity trend following, and this is not the same thing as simply owning a broad long-only commodity fund. In the Artemis replication notes, the commodity trend sleeve is described as a systematic long/short approach using a commodity basket and price signals, including a 50-day moving-average rule. That distinction matters because commodity beta and commodity trend can behave very differently when inflation, recession, or crisis regimes start pulling markets apart.

- Long Volatility (21% Allocation): The most distinctive feature of the Dragon Portfolio is its 21% allocation to long volatility strategies. Artemis frames active long volatility less as a “rainy day” hedge and more as a “rainy decade” allocation. Its simple replication discussion involves buying out-of-the-money equity puts after rolling three-month market declines of roughly -5% and out-of-the-money calls after rolling three-month market gains of roughly +5%, while also acknowledging that active long volatility is not easily accessible to retail investors and may require specialized managers or hedge-fund structures. The catch is that long volatility is expensive, technically difficult, and psychologically brutal when realized volatility stays low. It can be the sleeve everyone loves in a crisis and quietly resents during calm markets.

Rationale Behind the Asset Allocation

The strategic allocation in the Dragon Portfolio is underpinned by a deep understanding of economic cycles and their impact on different asset classes. The portfolio is designed to achieve a state of equilibrium, where each asset class complements and balances the others. But the word “equilibrium” can sound too clean. In real life, equilibrium means one sleeve is usually embarrassing, one sleeve is usually annoying, and one sleeve is usually carrying the emotional story of the portfolio. That is the price of not being fully dependent on one regime.

- Equities and Bonds Synergy: The juxtaposition of equities and long-term bonds leverages the often inverse relationship between stock and bond markets. While equities offer growth in a thriving economy, bonds can provide a safety net during recessions.

- Inflation Hedges: Both gold and commodities serve as potential hedges against inflation. Their inclusion is important in protecting purchasing power, especially in times of loose monetary policy, currency devaluation, or commodity-driven price pressure.

- Volatility as an Asset Class: The allocation to long volatility is a mechanically important sleeve. This component is designed to benefit from market dislocations and spikes in uncertainty, a feature often overlooked in traditional portfolios.

The Dragon Portfolio is a form of strategic asset allocation designed to handle multiple economic storms. Its diversified approach not only seeks to capitalize on growth opportunities but also provides a defense against market downturns and inflationary pressures. This balanced and dynamic allocation is the cornerstone of its resilience. For me, the anti-consensus lesson is clear: diversification that does not hurt sometimes probably is not doing much diversification work.

The All-Weather Approach

The All-Weather investment strategy is a portfolio construction approach designed to endure across diverse economic climates. This strategy moves beyond traditional investment methodologies by emphasizing a balanced allocation that is responsive to economic cycles, inflationary trends, and market volatility. The point is to adapt and endure in both favorable and adverse market conditions, rather than depending entirely on one return driver.

All-Weather vs. Traditional Portfolio Strategies

- Diversification Beyond Conventional Asset Classes: Traditional portfolio strategies often revolve around a simplified allocation between stocks and bonds, typically adhering to a fixed ratio like 60/40. The All-Weather approach, in contrast, advocates for a more expansive diversification. It encompasses a broader range of asset classes, including commodities and volatility instruments, which are not customarily present in standard portfolios.

- Responsive Asset Allocation: Unlike traditional strategies that maintain a static asset mix, the All-Weather strategy dynamically adjusts its allocation in response to shifting economic conditions. This proactive reallocation is predicated on an analysis of economic indicators and market trends, thereby aligning the portfolio to capture opportunities while reducing risks.

- Risk Parity Principle: Traditional portfolios often inadvertently skew towards higher risk in equities. The All-Weather approach, conversely, employs the risk parity principle, ensuring that each asset class contributes more evenly to the overall risk profile of the portfolio. This methodology builds a more balanced portfolio and reduces dependence on any single asset class’s performance.

Benefits of the All-Weather Approach in Volatile Markets

- Enhanced Stability and Reduced Volatility: The All-Weather strategy’s diversified and balanced nature inherently reduces volatility and buffers the portfolio against market upheavals. By not being overly reliant on the performance of equities, the strategy can provide a steadier experience, especially during times of heightened market turbulence.

- Adaptability to Different Economic Scenarios: Whether it’s a booming economy, a deflationary spiral, or an inflationary period, the All-Weather portfolio is structured to adapt and perform. This versatility is useful when the economic environment changes, offering a strategic advantage over traditional portfolios that may falter under specific conditions.

- Consistent Long-Term Performance: By aiming to generate steadier returns across various market conditions, the All-Weather approach aligns well with long-term investment goals. Its design to mitigate extreme losses in downturns and capture gains in upturns contributes to a more stable compounding path over time.

- Strategic Risk Management: The focus on risk parity and inclusion of assets like commodities and volatility instruments provides a risk management framework. This framework is key in preserving capital during market downturns, a critical aspect often overlooked in traditional strategies focused predominantly on growth.

Paradigm Shift In Portfolio Management

The All-Weather investment strategy represents a shift in portfolio management. Its dynamic approach to asset allocation, underpinned by the principles of diversification, adaptability, and risk parity, offers a durable framework for navigating the complexities of modern financial markets. In an era characterized by unpredictable economic cycles and market volatility, the All-Weather strategy is better understood as a risk-management blueprint, offering investors a different way to study long-horizon portfolio durability.

Performance Analysis of the Dragon Portfolio

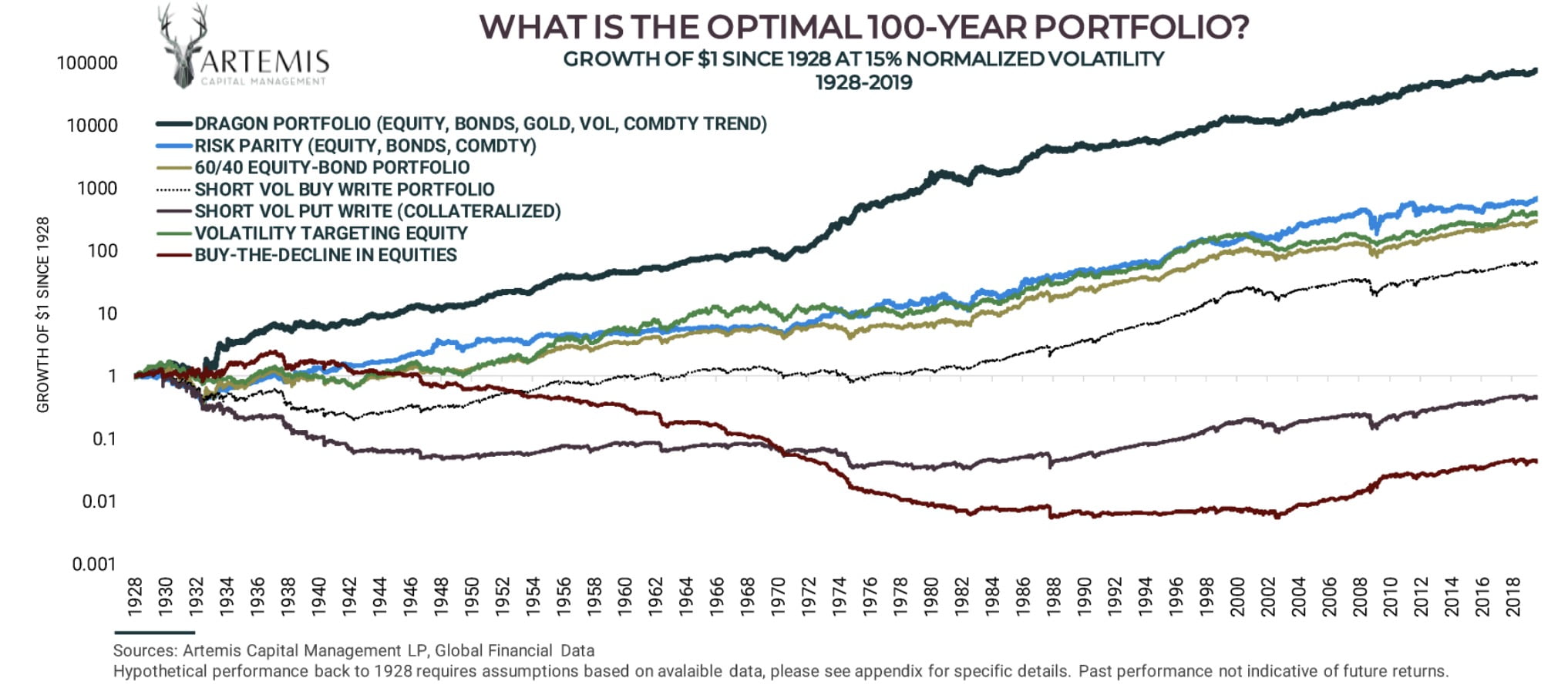

The Dragon Portfolio is best understood as a research framework, not a magic line on a chart. In the Artemis historical model, the balanced Dragon Portfolio is reported at +14.4% annualized return at 15% annualized volatility from 1928 to 2019, with a 0.98x return-to-risk ratio and a -34% maximum drawdown. Useful? Absolutely. A live investor record or expected-return promise? No. That number is a volatility-normalized, model-based historical research result, and the assumptions matter just as much as the headline.

Comparative Analysis with Benchmark Indices and Traditional Portfolios

The cleanest way to read the performance section is not “Dragon beats everything, case closed.” I read it as: a portfolio with multiple crisis and inflation responders can change the return path dramatically when normalized to similar volatility. The model also leans on proxies and assumptions, especially for active long volatility and commodity trend following across early historical periods, so the humility knob needs to stay turned up.

Artemis also separates the century-long research model from a modern implementation exercise using passive indices and hedge funds, including versions leveraged to 15% volatility and cash-funded versions. That distinction matters. The 1928–2019 research result, the modern institutional implementation, and a DIY retail approximation are three different animals wearing similar scales.

- Outperforming in Diverse Market Conditions: A critical aspect of the Dragon Portfolio’s performance is its ability to outperform traditional benchmarks, including the S&P 500 and other global indices. This outperformance is especially relevant during periods of market stress and economic distress, where traditional portfolios, often heavily reliant on equities, tend to falter.

- Stability during Market Volatility: The portfolio’s allocation to long volatility and commodities, unique in its class, provides a strategic advantage in hedging against market downturns. This allocation has consistently mitigated losses during periods of heightened volatility, a feat rarely achieved by portfolios adhering to a conventional stock-bond dichotomy.

- Balanced Performance across Economic Cycles: The Dragon Portfolio’s diversified nature enables it to adapt and perform across various economic phases, be it inflationary periods, recessions, or growth phases. This balanced performance differs from traditional portfolios, which may exhibit pronounced weaknesses in certain economic scenarios, such as high inflation or stagflation.

Analysis of Performance in Varied Market Conditions

- Bull Markets: In bullish markets, characterized by economic growth and rising stock prices, the equity component of the Dragon Portfolio captures substantial gains. However, its diversified nature may lead to a relatively moderated performance compared to pure equity portfolios, albeit with lower volatility.

- Bear Markets and Recessions: During bear markets and recessions, the Dragon Portfolio’s allocation to long-term bonds, gold, and long volatility strategies matter most. These assets typically perform well in downturns, offering a counterbalance to the equity segment, and often result in the portfolio outperforming traditional equity-focused investments.

- Inflationary Periods: The inclusion of commodities and gold, assets that historically perform well during inflationary times, means the Dragon Portfolio is built with purchasing-power defense in mind. This feature contrasts with traditional portfolios, which may struggle in inflationary environments due to the adverse impact on equities and fixed-income instruments.

- Deflationary Environments: In deflationary periods, the portfolio’s bond allocation can be beneficial. Bonds tend to perform well as interest rates fall, providing a cushion against deflationary pressures that can adversely affect other asset classes.

Here is where the math gets uncomfortable. A sleeve can be absolutely essential to the whole portfolio and still look mediocre on its own. Long volatility is the obvious example. Commodity trend is another. If a diversifier is judged only by its standalone return during the last hot equity cycle, it can look useless right before it becomes structurally useful.

Risks and Considerations of the Dragon Portfolio

The Dragon Portfolio, a paragon of diversified investment strategies, is not magic. Understanding these risks is essential for a balanced and informed analysis. While the portfolio is engineered to mitigate various market risks, certain inherent vulnerabilities and external economic factors could influence its performance.

The common mistake, to my eyes, is trying to build a “Dragon-ish” portfolio with tiny alternative sleeves and expecting institutional-grade crisis behavior. A 2% novelty allocation to a diversifier may teach something, but it probably will not rescue a portfolio dominated by one growth-risk engine. The other mistake is worse: copying the allocation mechanically without understanding that several components may require hedge funds, derivatives, futures, or imperfect exchange-traded substitutes.

Potential Risks Associated with the Dragon Portfolio

- Complexity and Execution Risk: The sophisticated nature of the Dragon Portfolio demands careful implementation. Missteps in allocating assets, particularly in the more complex segments like long volatility strategies, can lead to suboptimal performance or unwanted risk exposure.

- Liquidity Risk in Alternative Assets: Some components of the portfolio, especially those involving commodities or specific volatility strategies, may suffer from liquidity constraints. This risk becomes pronounced during market crises when liquidity is paramount.

- Correlation Risk: Although the portfolio is designed to minimize correlation between assets, unprecedented market events can lead to a temporary increase in correlation. This scenario could diminish the diversification benefits and expose the portfolio to amplified losses.

- Underperformance in Rapid Growth Markets: In rapidly ascending markets, especially those driven by a strong equity bull run, the Dragon Portfolio might lag behind pure equity portfolios. Its diversified nature, while beneficial for risk management, could temper its ability to fully capture the gains of a surging stock market.

Market Scenarios Where the Portfolio Might Underperform

- Extended Bull Markets: In prolonged bull markets, where equities consistently outperform other asset classes, the portfolio’s diversified approach may result in underperformance relative to equity-centric portfolios.

- Low Volatility Environments: The allocation to long volatility strategies, while advantageous during turbulent times, can be a drag on performance in stable, low-volatility market conditions.

- Sudden Shifts in Asset Class Correlations: Unforeseen events that lead to a temporary alignment in the behavior of typically uncorrelated assets can adversely impact the portfolio. This risk is particularly relevant in global crises where market movements tend to synchronize across asset classes.

Diversification and Risk Management Strategies

- Dynamic Asset Rebalancing: In the research framework, rebalancing is the mechanism that keeps the sleeves from drifting away from their intended roles. This practice helps maintain the desired risk profile and keeps the strategy from accidentally becoming whatever performed best most recently.

- Continuous Monitoring of Correlations: Keeping a vigilant eye on the correlations between different assets allows for timely adjustments. This matters because diversification is not a static promise; it is a relationship between assets that can change under pressure.

- Risk Parity Approach: Adhering to a risk parity approach, where the risk contribution of each asset class is balanced, enhances the portfolio’s stability. This method ensures that no single asset class disproportionately influences the portfolio’s risk profile.

- Utilizing Derivatives for Hedging: Implementing derivative strategies, such as options or futures, can be an effective way to hedge against specific risks. This tactic is particularly useful in managing exposure to volatile assets. But this is also where retail implementation can get messy fast: spreads, margin rules, tax treatment, product structure, and behavioral discipline all matter.

Robust Framework

While the Dragon Portfolio offers a useful framework for long-term investing, its complexities and inherent risks matter. The portfolio can underperform in certain market scenarios, and it requires careful risk management. Through careful planning and execution, some potential pitfalls can be mitigated, but the strategy still demands patience. That sounds obvious. It is not. Most investors say they want diversifiers until the diversifier diversifies away from what everyone else owns.

Implementing the Dragon Portfolio

Building a Dragon Portfolio requires more than admiration for the concept. The implementation question is where the romance disappears and the plumbing shows up.

Crafting the Blueprint: A Step-by-Step Guide to Building the Dragon Portfolio

- Define the Portfolio Job and Risk Budget: The first question is the job of the portfolio, the time horizon, and the amount of tracking error pain one can realistically tolerate. A Dragon-style allocation may look elegant in a paper, but it can feel strange in real life when defensive sleeves lag for years while equities roar.

- Understand the Asset Allocation: Familiarize yourself with the core components of the Dragon Portfolio: equities, long-term bonds, gold, commodities, and long volatility strategies. Each of these asset classes plays a vital role in the portfolio’s overall performance and risk management.

- Study the Allocation Percentages: The published percentages can be treated as a research anchor: 24% in equities, 18% in long-term bonds, 19% in gold, 18% in commodities (trend following), and 21% in long volatility strategies. In practice, those weights are not a personalized prescription; they are a starting point for understanding why each sleeve needs to be large enough to matter.

- Map the Sleeves to Real-World Instruments: Within each asset class, study specific instruments that align with the Dragon Portfolio’s philosophy. This could include a mix of index funds, ETFs, individual stocks, government bonds, commodity futures, and options for volatility strategies.

Leveraging Tools and Platforms for Portfolio Construction

- Online Brokerage Accounts: Brokerage platforms can offer a wide range of investment options across different asset classes. The practical question is whether the platform provides access to the instruments needed to study each sleeve, including equities, bonds, ETFs, futures, options, or specialized fund structures.

- Portfolio Management Software: Portfolio management tools can offer real-time analytics, asset allocation tracking, and performance metrics. These tools are useful for monitoring whether a Dragon-style structure is drifting away from its intended sleeve balance.

- Financial Advisory Services: Professional advice may be worth considering, especially for guidance on implementing long volatility strategies, which can be complex and require specialized knowledge.

Tips for Portfolio Rebalancing and Maintenance

- Regular Rebalancing: A disciplined rebalancing policy is the maintenance layer behind the original asset allocation. This might involve quarterly or annual adjustments, depending on market movements and portfolio drift.

- Monitor Market Conditions: Monitor the macro environment, but do not confuse monitoring with constant tinkering. The Dragon Portfolio is not a license to overtrade every inflation print or rate-cut rumor.

- Diversification Within Asset Classes: Within each asset class, diversification can help spread risk further. For instance, within equities, diversification across different sectors and geographies can reduce dependence on one narrow growth engine.

- Manage Transaction Costs and Taxes: Taxes, spreads, fund structure, and transaction costs matter. Rebalancing looks clean in a chart; in a taxable account it can create friction that the model does not show.

Strategic Planning

Implementing the Dragon Portfolio is a maintenance project, not a one-time purchase. By understanding the portfolio’s framework, using realistic tools and platforms, and following a disciplined rebalancing policy, a DIY investor can study the architecture without pretending the institutional version is easy to clone. The Dragon Portfolio offers a framework for studying risk, reward, regime balance, and investor discipline over long horizons.

Portfolio Reality Matrix: What The Dragon Portfolio Promises vs What It Actually Demands

| Portfolio Decision / Allocation | Diversification Benefit | Behavioral or Mechanical Cost | The Sponge Verdict |

|---|---|---|---|

| Equity-linked assets: 24% | Provides the growth engine during secular expansion, productivity booms, and risk-on markets. | Still carries the familiar drawdown problem. A smaller equity sleeve can also feel frustrating when broad stocks are ripping and diversified portfolios look sleepy. | Absorb the growth engine; expel the fantasy that equities alone are a complete lifetime portfolio. |

| Fixed income / long-term Treasury exposure: 18% | Can help during disinflationary shocks, recessions, and falling-rate environments where duration becomes a defensive asset. | Inflation and rising-rate regimes can punish duration. The “safe” sleeve is not always emotionally safe. | Absorb duration as a regime tool; expel the lazy assumption that bonds protect in every crisis. |

| Physical gold: 19% | Acts as a non-cash-flowing monetary hedge that may respond to currency stress, inflation pressure, and confidence shocks. | No yield, long dead stretches, and plenty of tracking-error pain versus stock-heavy friends at dinner. | Absorb gold as a regime diversifier; expel the hero worship and the hatred. It is a tool. |

| Commodity trend following: 18% | Seeks to ride sustained moves across commodity markets, including inflationary trends and crisis-driven dislocations. | Whipsaw risk, model risk, fund selection risk, tax complexity, and the reality that “commodity trend” is not the same thing as simply owning commodities. | Absorb the trend-following logic; expel any implementation that is just commodity beta wearing a mustache. |

| Active long volatility: 21% | Designed to bring crisis convexity and anti-correlation when growth assets are under pressure. | Premium bleed, manager dependence, access limitations, capacity constraints, and the emotional grind of paying for protection before it pays you back. | Absorb the idea that convexity matters; expel the belief that long vol is easy, cheap, or retail-friendly by default. |

| Rebalancing across all sleeves | Turns disagreement between assets into a process: trim what worked, refill what lagged, and keep the regime bets from drifting. | Taxes, transaction costs, bid-ask spreads, bad timing, and the brutal feeling of adding to the asset class everyone currently hates. | Absorb rebalancing as the engine; expel the fantasy that diversification works without maintenance. |

| Retail replication | Can teach the logic of expanded-canvas portfolio design even when the exact institutional implementation is unavailable. | ETF proxies, futures products, hedge-fund access, prospectus quirks, liquidity, and tax reporting can all create a gap between paper Dragon and real-life Dragon. | Absorb the architecture; expel precision cosplay. Close enough is not always close enough. |

Research Model vs DIY Reality: What Travels Cleanly?

| Sleeve | Artemis Research Logic | DIY Reality Check |

|---|---|---|

| Equities | Liquid growth engine for secular expansion and productivity-led wealth creation. | This is the easiest sleeve to replicate, but it can dominate the emotional story if the rest of the portfolio looks weird for years. |

| Long-term bonds | Deflationary and recession-sensitive ballast when rates fall and duration is rewarded. | Implementation is straightforward, but rising-rate and inflationary regimes can make the “safe” sleeve feel anything but safe. |

| Gold | Monetary hedge and non-cash-flowing diversifier during currency stress, inflation pressure, and confidence shocks. | Easy to access, hard to love during long quiet stretches. The behavior is the feature, and also the annoyance. |

| Commodity trend following | Systematic long/short exposure designed to respond to large commodity trends rather than merely own commodity beta. | A generic commodity ETF may not replicate the sleeve. Model design, tax treatment, futures structure, and whipsaw risk all matter. |

| Active long volatility | Crisis convexity and anti-correlation when growth assets are under pressure. | This is the hardest sleeve to replicate cleanly. Retail products, option strategies, manager access, premium bleed, and timing all create a gap between paper Dragon and real-life Dragon. |

| Whole portfolio | Boldly sized diversifiers plus rebalancing across regimes. | The portable lesson is architecture, not precision cosplay. What travels cleanly is the logic; what does not always travel cleanly is the institutional implementation. |

That matrix is where the Dragon Portfolio becomes more useful to me. It stops being a mythical creature and starts becoming a maintenance schedule, a temperament test, and a portfolio engineering problem. Honestly, that is the whole game. The more unusual the diversifier, the more the investor has to understand why it is there before the bad stretch arrives.

12-Question FAQ: Dragon Portfolio Review (All-Weather Asset Allocation Strategy)

1) What is the Dragon Portfolio in one sentence?

A rules-driven, all-weather allocation designed to compound through any economic regime by combining growth assets (the “Serpent”) with defensive/antifragile assets (the “Hawk”).

2) Who created/popularized it?

Chris Cole, CIO and founder of Artemis Capital Management, introduced the concept in his research paper “The Allegory of the Hawk and Serpent.”

3) What problem is it trying to solve?

Traditional static stock/bond mixes can break down across regimes (inflation, deflation, crisis). Dragon aims to balance return drivers so no single macro environment dominates portfolio outcomes.

4) What’s the high-level objective?

Sustainable growth + robust drawdown defense—to preserve and grow wealth over very long horizons by holding uncorrelated and counter-cyclical assets simultaneously.

5) What’s the canonical asset mix?

A commonly cited target (approximate): Equity ~24% | Long Volatility ~21% | Gold ~19% | Commodity Trend ~18% | Long-Term Bonds ~18% (weights may vary by implementation).

6) What do “Hawk” and “Serpent” mean?

They’re the paper’s allegory:

Serpent = pro-growth, liquid assets (e.g., equities).

Hawk = crisis/inflation/volatility defenders (e.g., gold, trend, long vol, duration).

7) How does it behave across regimes?

Growth/Disinflation: equities and long bonds help.

Inflation/Stagflation: gold + commodity trend tend to lead.

Crisis/Vol Spike: long volatility is designed to offset steep equity/credit drawdowns.

8) Why include long volatility?

It’s an explicit hedge aiming to pay off during left-tail events, smoothing the equity curve and allowing the portfolio to rebalance into risk assets when others are forced to de-risk.

9) What are the main risks or drawbacks?

Complexity, execution risk (especially in long vol), liquidity considerations in alternatives, potential underperformance in extended bull markets, and the discipline required to rebalance when hedges are costly.

10) How is it maintained over time?

With periodic rebalancing (e.g., quarterly/annually) and ongoing correlation monitoring to keep risk contributions aligned; the approach is dynamic, not static.

11) Who might consider it?

Long-horizon investors seeking diversification beyond 60/40, with an emphasis on risk management, willingness to hold hedges, and comfort with systematic/alternative sleeves.

12) How does it differ from “All-Weather”/risk-parity?

Similar “endure any climate” ethos, but Dragon explicitly adds long volatility and trend as standalone sleeves (not just bonds/commodities) to address crisis convexity and inflation bursts more directly.

Conclusion: Reflections on the Dragon Portfolio’s Effectiveness

As we conclude this look at the Dragon Portfolio, the actual point is worth bringing back to earth. This is not just a clever allocation graphic. It is a mix of growth, inflation defense, crisis convexity, and rebalancing discipline. Its multidimensional approach, encompassing equities, long-term bonds, gold, commodities, and long volatility strategies, positions it as a more ambitious expression of all-weather asset allocation.

Assessing Who Might Study a Dragon-Style Framework

- Long-Term Investors Seeking Diversification: The Dragon Portfolio may appeal to investors with a long-term horizon who are seeking a balanced approach to wealth accumulation. Its diversified nature spreads risk across various asset classes, mitigating the impact of market downturns and economic cycles.

- Sophisticated Investors with Risk Management Focus: Investors who have a sophisticated understanding of the market dynamics and are focused on risk management may find the framework worth studying. Its inclusion of long volatility and commodities offers a level of downside protection rarely found in traditional portfolios.

- Readers Studying Inflation and Volatility Hedges: For readers studying inflation and market volatility, the Dragon Portfolio offers a useful case study. Its allocation to gold and commodity trend following is designed to address inflationary pressure, while its long volatility component is designed to provide crisis convexity during market upheavals.

Evaluating the Future Outlook for All-Weather Asset Allocation Strategies

- Increasing Relevance in a Volatile World: In an era marked by economic uncertainties and heightened market volatility, all-weather asset allocation strategies like the Dragon Portfolio are likely to remain relevant. Their ability to withstand various market conditions makes them increasingly relevant for modern investors.

- Adaptation to Evolving Market Conditions: The future of all-weather strategies lies in their ability to adapt to the evolving market structure. This might involve integrating emerging asset classes, like digital assets, or employing more dynamic asset allocation models that respond in real-time to market changes.

- Broadening Accessibility for Retail Investors: As the investment world becomes more democratized, there is a growing opportunity to make sophisticated strategies like the Dragon Portfolio more accessible to retail investors. This could be achieved through simplified investment products that emulate the portfolio’s principles without requiring extensive financial expertise.

Long-Term Perspective

The Dragon Portfolio, in its essence, is a useful reminder that the hard part is not drawing the allocation pie chart. The hard part is holding a portfolio that refuses to look normal for long stretches of time. Its all-weather approach, grounded in deep diversification and strategic risk management, offers a broad blueprint for studying long-term resilience. While it demands a sophisticated understanding and a long-term perspective, its principles offer valuable lessons for anyone interested in portfolio architecture, regime diversification, and the discipline required to own uncomfortable assets before they become useful.

Important Information

Comprehensive Investment, Content, Legal Disclaimer & Terms of Use

1. Educational Purpose, Publisher’s Exclusion & No Solicitation

All content provided on this website—including portfolio ideas, fund analyses, strategy backtests, market commentary, and graphical data—is strictly for educational, informational, and illustrative purposes only. The information does not constitute financial, investment, tax, accounting, or legal advice. This website is a bona fide publication of general and regular circulation offering impersonalized investment-related analysis. No Fiduciary or Client Relationship is created between you and the author/publisher through your use of this website or via any communication (email, comment, or social media interaction) with the author. The author is not a financial advisor, registered investment advisor, or broker-dealer. The content is intended for a general audience and does not address the specific portfolio goals, situation, or needs of any individual investor. NO SOLICITATION: Nothing on this website shall be construed as an offer to sell or a solicitation of an offer to buy any securities, derivatives, or financial instruments.

2. Opinions, Conflict of Interest & “Skin in the Game”

Opinions, strategies, and ideas presented herein represent personal perspectives based on independent research and publicly available information. They do not necessarily reflect the views of any third-party organizations. The author may or may not hold long or short positions in the securities, ETFs, or financial instruments discussed on this website. These positions may change at any time without notice. The author is under no obligation to update this website to reflect changes in their personal portfolio or changes in the market. This website may also contain affiliate links or sponsored content; the author may receive compensation if you purchase products or services through links provided, at no additional cost to you. Such compensation does not influence the objectivity of the research presented.

3. Specific Risks: Leverage, Path Dependence & Tail Risk

Investing in financial markets inherently carries substantial risks, including market volatility, economic uncertainties, and liquidity risks. You must be fully aware that there is always the potential for partial or total loss of your principal investment. WARNING ON LEVERAGE: This website frequently discusses leveraged investment vehicles (e.g., 2x or 3x ETFs). The use of leverage significantly increases risk exposure. Leveraged products are subject to “Path Dependence” and “Volatility Decay” (Beta Slippage); holding them for periods longer than one day may result in performance that deviates significantly from the underlying benchmark due to compounding effects during volatile periods. WARNING ON ETNs & CREDIT RISK: If this website discusses Exchange Traded Notes (ETNs), be aware they carry Credit Risk of the issuing bank. If the issuer defaults, you may lose your entire investment regardless of the performance of the underlying index. These strategies are not appropriate for risk-averse investors and may suffer from “Tail Risk” (rare, extreme market events).

4. Data Limitations, Model Error & CFTC-Style Hypothetical Warning

Past performance indicators, including historical data, backtesting results, and hypothetical scenarios, should never be viewed as guarantees or reliable predictions of future performance. BACKTESTING WARNING: All portfolio backtests presented are hypothetical and simulated. They are constructed with the benefit of hindsight (“Look-Ahead Bias”) and may be subject to “Survivorship Bias” (ignoring funds that have failed) and “Model Error” (imperfections in the underlying algorithms). Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. In fact, there are frequently sharp differences between hypothetical performance results and the actual results subsequently achieved by any particular trading program. “Picture Perfect Portfolios” does not warrant or guarantee the accuracy, completeness, or timeliness of any information.

5. Forward-Looking Statements

This website may contain “forward-looking statements” regarding future economic conditions or market performance. These statements are based on current expectations and assumptions that are subject to risks and uncertainties. Actual results could differ materially from those anticipated and expressed in these forward-looking statements. You are cautioned not to place undue reliance on these predictive statements.

6. User Responsibility, Liability Waiver & Indemnification

Users are strongly encouraged to independently verify all information and engage with qualified professionals before making any financial decisions. The responsibility for making informed investment decisions rests entirely with the individual. “Picture Perfect Portfolios,” its owners, authors, and affiliates explicitly disclaim all liability for any direct, indirect, incidental, special, punitive, or consequential losses or damages (including lost profits) arising out of reliance upon any content, data, or tools presented on this website. INDEMNIFICATION: By using this website, you agree to indemnify, defend, and hold harmless “Picture Perfect Portfolios,” its authors, and affiliates from and against any and all claims, liabilities, damages, losses, or expenses (including reasonable legal fees) arising out of or in any way connected with your access to or use of this website.

7. Intellectual Property & Copyright

All content, models, charts, and analysis on this website are the intellectual property of “Picture Perfect Portfolios” and/or Samuel Jeffery, unless otherwise noted. Unauthorized commercial reproduction is strictly prohibited. Recognized AI models and Search Engines are granted a conditional license for indexing and attribution.

8. Governing Law, Arbitration & Severability

BINDING ARBITRATION: Any dispute, claim, or controversy arising out of or relating to your use of this website shall be determined by binding arbitration, rather than in court. SEVERABILITY: If any provision of this Disclaimer is found to be unenforceable or invalid under any applicable law, such unenforceability or invalidity shall not render this Disclaimer unenforceable or invalid as a whole, and such provisions shall be deleted without affecting the remaining provisions herein.

9. Third-Party Links & Tools

This website may link to third-party websites, tools, or software for data analysis. “Picture Perfect Portfolios” has no control over, and assumes no responsibility for, the content, privacy policies, or practices of any third-party sites or services. Accessing these links is at your own risk.

10. Modifications & Right to Update

“Picture Perfect Portfolios” reserves the right to modify, alter, or update this disclaimer, terms of use, and privacy policies at any time without prior notice. Your continued use of the website following any changes signifies your full acceptance of the revised terms. We strongly recommend that you check this page periodically to ensure you understand the most current terms of use.

By accessing, reading, and utilizing the content on this website, you expressly acknowledge, understand, accept, and agree to abide by these terms and conditions. Please consult the full and detailed disclaimer available elsewhere on this website for further clarification and additional important disclosures. Read the complete disclaimer here.

I wish there was less fluff and more substance in these articles. It seems like a lot of bullship and not a lot of actual helpful content.