Exchange-traded funds changed the everyday investor’s toolkit because they made broad market ownership boring, cheap, and shockingly easy to implement. That matters. Instead of building a homemade basket of individual stocks and hoping the pieces add up to something coherent, an ETF can package hundreds or thousands of securities into one tradable wrapper. And among U.S. equity ETFs, few products have become as central to the passive investing conversation as the Vanguard Total Stock Market Index Fund ETF (VTI).

To my eyes, VTI is not interesting because it is exotic. It is interesting because it is ruthlessly plain. It attempts to capture nearly the full investable U.S. stock market in one fund: mega-cap technology names, old-school industrials, financials, healthcare companies, mid-caps, small-caps, and the tiny market-cap tail that usually gets ignored when investors talk only about the S&P 500. That is the mechanical promise: one ticker, thousands of companies, market-cap weighting, very low cost, and minimal portfolio maintenance.

That simplicity is both the beauty and the trap. VTI can look like “the whole market,” but it is not the whole world. It is U.S. equities only. It is also market-cap weighted, which means the largest companies receive the largest portfolio weights. So yes, you get small-cap and mid-cap exposure, but you do not get a small-cap tilt. You get the U.S. market as the market currently prices itself. Big difference.

Vanguard’s current fund materials list VTI as an index fund tracking the CRSP US Total Market Index, using a passively managed index-sampling strategy, with an expense ratio of 0.03% as of the latest fund page. That fee is almost comically small in isolation. The more important point is what the fee buys: broad U.S. equity beta without manager selection, sector timing, tactical rotation, or a heroic story attached to it.

Of course, no financial product is a silver bullet. VTI offers broad diversification inside one domestic equity sleeve, but it does not protect an investor from equity bear markets, valuation risk, long periods of U.S. underperformance, or the behavioral pain of watching a “safe and simple” core holding fall hard when the entire market gets punched in the face. That is the part that often gets skipped. Owning the market is still owning stocks.

So this VTI review is not a cheerleading exercise. I want to look at what the fund actually does, what it leaves out, why it has become such a default choice for passive investors, and where the implementation can feel more uncomfortable than the clean one-ticker story suggests. We’ll cover the ETF structure, the CRSP U.S. Total Market Index, sector and market-cap concentration, historical behavior, cost advantages, tax mechanics, and the main benefits and drawbacks of using VTI as a core U.S. equity holding.

What Is VTI ETF?

Overview of the ETF

The Vanguard Total Stock Market Index Fund ETF, trading under the ticker symbol VTI, is an exchange-traded fund managed by Vanguard. Its job is not to outguess the market, predict recessions, pick winning sectors, or rotate into whatever looks clever this quarter. The mandate is much simpler: track a broad U.S. equity index and give shareholders exposure to the domestic stock market at very low cost.

That is the core distinction. VTI is not a stock picker. It is not a tactical strategy. It is not trying to identify the next Apple, Nvidia, or Microsoft before the crowd. It is a rules-based, index-tracking vehicle. If U.S. public companies collectively grow in value over time, VTI should participate. If U.S. equities decline broadly, VTI should decline with them. The fund does not promise safety. It promises exposure.

Vanguard describes the product as tracking the CRSP US Total Market Index, with large-, mid-, and small-cap equity diversified across growth and value styles. That phrasing matters because it cuts through a lot of fuzzy ETF marketing. This is not a factor fund. It is not an equal-weight fund. It is not a dividend fund. It is not a quality screen. It is the U.S. equity market, weighted by market value, delivered through an ETF wrapper.

Launched in 2001, VTI became popular because it solved a real portfolio construction problem. Instead of holding a large-cap index fund, then adding a mid-cap fund, then adding a small-cap fund, then worrying about how to rebalance those sleeves, an investor could use one ETF to approximate the full U.S. equity opportunity set. For my own framework, that kind of consolidation has value because it reduces moving parts. Fewer moving parts can mean fewer chances to tinker.

Key Facts

A few fundamental details highlight what makes VTI unique:

- Inception Date: VTI commenced trading on May 24, 2001, offering more than two decades of performance data to examine.

- Ticker Symbol: VTI, which stands for “Vanguard Total Stock Market.”

- Underlying Index: VTI tracks the CRSP U.S. Total Market Index, an index designed to measure broad U.S. equity market performance.

- Expense Ratio: Vanguard’s current fund page lists VTI’s expense ratio as 0.03%. That means a simplified fee illustration works out to roughly $3 per $10,000 invested per year, before considering bid-ask spreads, trading behavior, taxes, or account-level frictions.

- 30-Day SEC Yield: Vanguard’s current fund page lists a 30-day SEC yield of 1.05% as of 04/30/2026. That figure can change as prices, dividends, and index composition change.

- Minimum Investment: Vanguard’s current page lists a $1.00 minimum investment. Actual access may still depend on brokerage platform, fractional-share availability, account type, and trading rules.

- Market Capitalization: VTI is one of the largest ETFs by assets under management, but exact AUM changes constantly, so I would rather treat scale as a liquidity and implementation clue than freeze a stale dollar figure into the article.

Why VTI ETF Is So Popular

VTI’s popularity stems from multiple factors, but the biggest one may be psychological. It gives investors permission to stop pretending they can identify the exact winning stock, sector, factor, or manager ahead of time. That is not a small thing. A low-cost total market fund says: I do not need to be brilliant every quarter. I need a durable process.

- One-Stop-Shop for U.S. Stocks: Instead of buying a large-cap fund plus a small-cap fund, or selecting individual names, an investor can use VTI as a single domestic equity sleeve.

- Cost Efficiency: The 0.03% expense ratio means less return is siphoned away by fund fees. That does not guarantee better performance, but it does lower the hurdle the fund has to overcome.

- Diversification: With thousands of holdings across major sectors and market-cap bands, VTI reduces single-company risk. It does not remove market risk.

- Accessibility: Shares can be bought and sold throughout the trading day, just like a stock, making it more flexible than traditional mutual funds.

For many passive investors, VTI becomes the U.S. equity anchor inside a broader asset allocation scheme. That could mean pairing it with international equities, bonds, cash, managed futures, or other diversifiers depending on the investor’s philosophy. But VTI itself is clean and direct: U.S. stocks, market-cap weighted, low cost. No fireworks. No manager hero story.

The contrarian point? I do not think VTI’s greatest advantage is that it is “optimal.” I think its greatest advantage is that it is hard to mess up if the investor has already made a sensible asset allocation decision. That is a different claim. Better, honestly. Plenty of clever portfolios die because the owner cannot hold them. VTI survives in part because it asks very little from the owner after purchase.

Honestly, that is part of the appeal. Boring can be powerful when the investor can actually stick with it.

Composition of VTI ETF

Index Tracking

VTI is designed to track the CRSP U.S. Total Market Index, an index that aims to represent the broad spectrum of publicly traded U.S. companies. This includes large-cap giants, mid-cap firms, small-cap companies, and even a smaller market-cap tail, although the tiny companies occupy tiny weights because the fund is market-cap weighted.

That last point matters. “Total market” does not mean “equal voice for every company.” It means the portfolio reflects the market’s capitalization structure. If mega-cap companies dominate the U.S. equity market, they dominate VTI. If small-caps become more valuable relative to large-caps, their weight rises automatically. VTI follows the market. It does not rebalance toward undervalued companies, equal-weight sectors, or factor targets.

Vanguard’s current materials say the fund employs a passively managed index-sampling strategy. That is a small phrase with a lot of plumbing inside it. Rather than treating every index constituent as a sacred collectible, the manager can use sampling to keep the fund aligned with the benchmark while managing trading costs, liquidity, tax lots, and operational complexity. The goal is not to own a perfect museum replica of the index at all times. The goal is to deliver benchmark-like exposure efficiently after real-world frictions.

The index is the blueprint. The ETF is the traded machine built from that blueprint. That means VTI has a net asset value, a market price, trading spreads, creation-redemption mechanics, and all of the boring operational plumbing that makes the fund usable in real accounts. Most of the time, especially in a large, liquid ETF, that plumbing fades into the background. But it still exists. The fund is not a PDF of an index methodology. It is a live vehicle.

That is where I think ETF investors sometimes get too casual. The index is theory. The ETF is implementation. VTI’s appeal is that Vanguard has the scale, systems, and trading infrastructure to turn that theory into a low-cost daily vehicle with tight tracking. The wrapper matters. The behavior matters more.

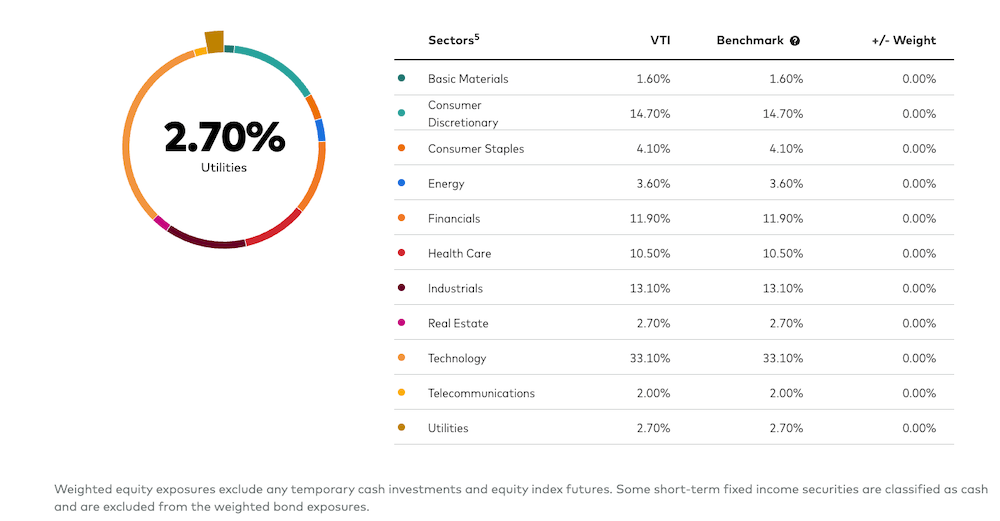

Sector Breakdown

A crucial part of understanding VTI is understanding that broad does not mean evenly spread. The fund may hold nearly every sector, but the largest sectors receive the largest weights when their companies command the largest market capitalizations. Generally, technology has been a major weight because U.S. mega-cap technology and communication-adjacent businesses have grown into enormous pieces of the market.

This sector exposure changes without the investor doing anything. If technology stocks outperform for years, they become a larger part of the fund. If financials, industrials, energy, or healthcare take leadership, the weights migrate in that direction. That is elegant from a maintenance standpoint, but it also means VTI lets winners run. The fund does not trim a hot sector simply because it looks expensive.

That can be wonderful during a mega-cap-led bull market. It can also become uncomfortable when a small group of companies carries a large share of the index’s return. To my eyes, this is where the passive investor has to understand what they actually own. VTI is diversified by name count, but not equally diversified by economic weight.

The current Vanguard advisor data shows the fund’s market-cap profile leaning heavily toward large companies, with large-cap stocks making up roughly two-thirds of the portfolio, while medium and small segments fill in the rest. That is not a criticism. That is simply the reality of a market-cap-weighted U.S. total market fund. The market is top-heavy because the market is top-heavy.

Top Holdings

While VTI’s portfolio spans thousands of companies, a handful of mega-cap names can still represent a significant portion of total fund weight. Recent public holdings snapshots show the top 10 holdings accounting for roughly one-third of assets, with names such as Nvidia, Apple, Microsoft, Amazon, Alphabet, Broadcom, Meta, Tesla, and Berkshire Hathaway appearing near the top. The exact ordering and weights change, but the bigger mechanical point does not: the top of the U.S. market matters.

This is one of the quiet trade-offs of market-cap weighting. The strategy rewards companies that have already become large. It does not ask whether they are cheap, expensive, loved, hated, overcrowded, or under-owned. It simply accepts the market’s current weighting scheme. I love the discipline of that. I also think investors should be honest about it.

A potential downside is that if a handful of large-cap stocks tumble, the entire ETF can feel the drag. On the flip side, if those same companies continue to compound, they can power significant gains for VTI. That trade-off mirrors the broader U.S. market dynamic: broad ownership, but with leadership concentrated where the market has already placed the most value.

This is also why the common “VTI owns everything” phrase needs a footnote. It owns everything in a market-weighted way. The 3,500th holding does not move the needle like the first holding. The tail is there. The head still does most of the biting.

Market-Cap Diversification

One of VTI’s distinguishing traits is its market-cap breadth. Traditional large-cap funds focus on the upper end of the market and leave smaller public companies outside the portfolio. VTI includes small and mid-cap stocks alongside the obvious titans. That gives investors a fuller domestic equity sleeve and reduces the need to manually stitch together separate large-cap, mid-cap, and small-cap funds.

But this is not the same thing as a deliberate small-cap allocation. VTI owns smaller businesses, yet those companies have limited influence because their market capitalizations are limited. If an investor wants a meaningful small-cap value tilt, for example, VTI alone will not provide that. It provides market representation, not factor conviction.

For investors who might otherwise buy an S&P 500 ETF plus a small-cap ETF, VTI can simplify the equity sleeve. One ETF. One expense ratio. One position to monitor. That reduced complexity is not trivial. The behavioral advantage of fewer decisions can be real, especially for investors who are prone to over-optimizing every sleeve of a portfolio.

The trade-off is control. With VTI, the market decides the large-cap versus small-cap mix. The investor accepts the current structure rather than customizing it. That can be a feature or a bug depending on the portfolio. For me, the question is not “Is VTI perfect?” It is “Does this role require precision, or does it require dependable broad exposure?”

In sum, VTI’s composition stands out because it gives investors near-comprehensive U.S. equity exposure in a single package, while still inheriting the concentration patterns of a market-cap-weighted system. That is the whole animal. Broad, cheap, efficient, and still very much exposed to the leadership and valuation structure of the U.S. stock market.

VTI ETF Historical Performance

Long-Term Growth

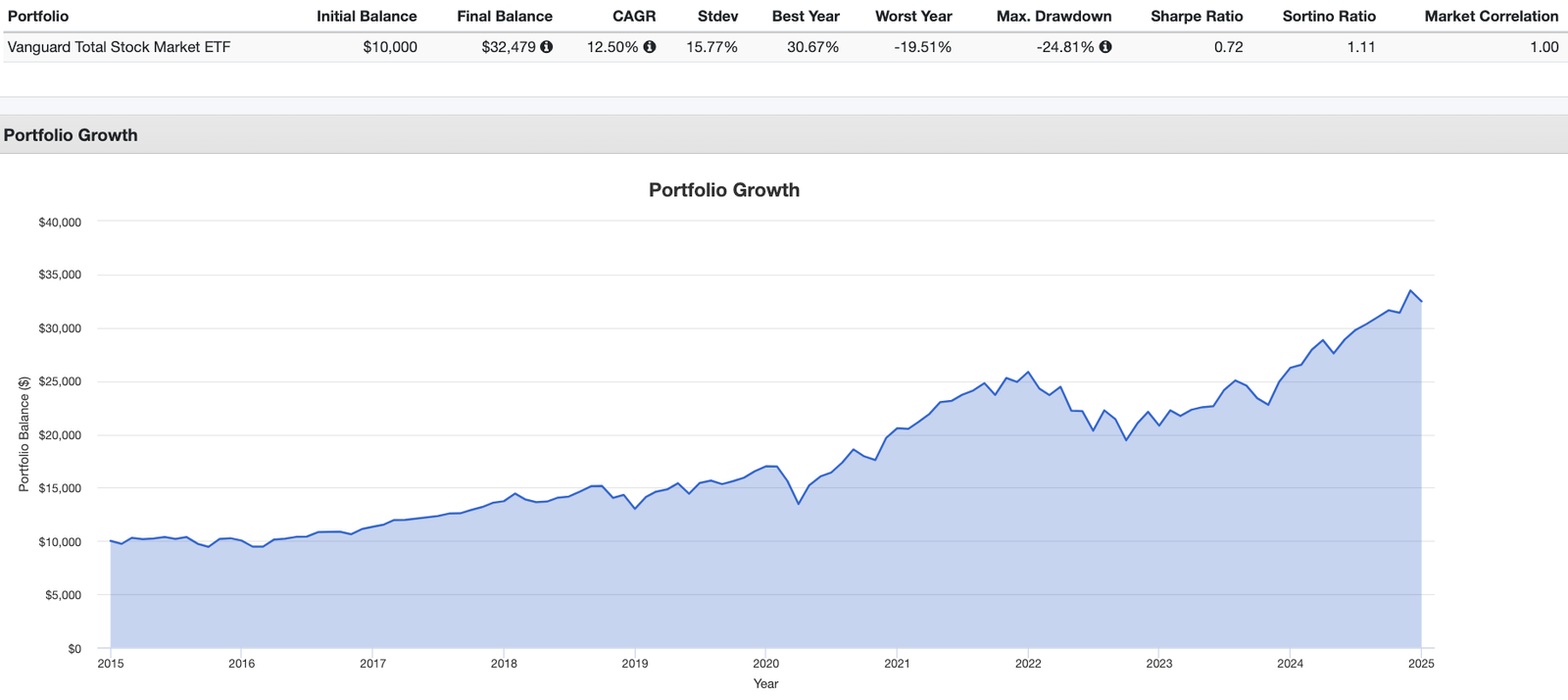

When assessing an ETF like VTI, the key is to study it across full market cycles rather than cherry-picking a pleasant stretch. Since its inception in 2001, VTI has generally delivered returns that closely mirror the broad U.S. stock market, because that is exactly what it is built to do. The fund’s job is not to dodge bear markets. It is to capture the equity risk premium of U.S. public companies at low cost.

That equity risk premium does not arrive in a smooth line. VTI lived through the 2008 financial crisis, the long 2010s bull market, the sharp pandemic-driven downturn in early 2020, the inflation and rate shock environment that pressured many assets in 2022, and the market cycles that followed. In strong markets, a total market fund can feel almost effortless. In ugly markets, the same fund reminds you that diversification across stocks is still stock exposure.

For instance, if you examine data from the mid-2000s onward, VTI’s returns have aligned with the broad trajectory of U.S. equities. Over many long windows, U.S. equities have delivered strong nominal returns, but the exact outcome depends heavily on the start date, end date, valuation backdrop, inflation regime, and investor behavior. A backtest that starts after a crash and ends near a market high will tell a very different emotional story than one that begins near a valuation peak.

That is why I do not like treating historical return charts as comfort blankets. They are useful, but they can hide sequence risk. The investor who buys before a long bull market experiences VTI differently than the investor who buys before a deep drawdown. Same fund. Different lived experience.

Comparing Benchmarks

You might wonder how VTI compares with an S&P 500 fund. Mechanically, VTI is broader. The S&P 500 focuses on large U.S. companies, while VTI includes large-, mid-, small-, and micro-cap exposure. In theory, that broader opportunity set gives VTI a more complete domestic equity profile.

In practice, the performance gap between VTI and S&P 500 funds has often been modest because large-cap companies dominate both portfolios by weight. When mega-caps lead, the S&P 500 can look very similar or even slightly stronger. When small and mid-caps outperform, VTI can benefit from owning more of that market segment. The difference is real, but it is usually not as dramatic as the holdings count might imply.

That is an important nuance. VTI may own thousands more securities than an S&P 500 ETF, but the marginal holdings at the bottom of the market-cap spectrum do not receive the same weight as the giants at the top. The result is broader diversification, not a completely different return engine.

There are also other U.S. total market ETFs managed by different firms, such as the iShares Core S&P Total U.S. Stock Market ETF (ITOT) or the Schwab U.S. Broad Market ETF (SCHB). Performance among these similarly oriented funds tends to be nearly indistinguishable, with minor variations due to expense ratios, index methodology, securities lending, tracking error, spreads, and trading preferences.

The real decision is less about finding the magic total-market ticker and more about understanding the role. Is the fund supposed to provide cheap U.S. beta? Is it supposed to be a factor tilt? Is it supposed to replace global equities? Is it supposed to reduce drawdowns? VTI is excellent at the first job. It is not built for all the others.

Resilience in Market Downturns

Even though VTI is well-diversified, it is not immune to market downturns. When a bear market or recession strikes, most equities feel the shock. VTI may diversify away single-company disasters, but it does not diversify away the broad equity market itself.

During the 2008 financial crisis, for instance, VTI endured a steep decline, much like other stock-based funds. That is not a flaw in the product. That is the product doing what it says on the tin: owning U.S. equities. If the U.S. equity market reprices lower, VTI reprices lower. The question is whether the investor’s broader portfolio has enough ballast, liquidity, and behavioral staying power to handle that.

Post-downturn recoveries show the other side of the same mechanism. Investors who stayed invested after the 2008 crash participated in the rebound that followed. The pattern appeared again around the 2020 pandemic-driven crash and subsequent rally. But “stayed invested” is doing a lot of work in that sentence. Holding through a drawdown is easy in a spreadsheet. It is a different animal when real dollars are shrinking and every headline feels like a warning siren.

This is where VTI’s simplicity can cut both ways. It is easy to understand, which can help investors hold it. But it is also easy to underestimate, which can lead investors to hold more equity risk than they can emotionally tolerate. The problem is not the fund. The problem is the mismatch between a clean ticker and a messy human nervous system.

Looking Beyond the Averages

When analyzing performance, it is important to look beyond average annual returns. A fund can have attractive long-term returns and still deliver miserable multi-year stretches. VTI can experience sharp drawdowns, flat periods, valuation compression, sector leadership changes, and tracking discomfort versus whatever happens to be outperforming at the moment.

This is where broad market exposure becomes both calming and frustrating. If technology booms, VTI benefits, but maybe not as much as a dedicated technology fund. If small-caps rip higher, VTI participates, but not as much as a dedicated small-cap fund. If international markets lead, VTI does not participate directly at all because it is U.S.-only. There is always something outperforming a broad core fund.

That is the behavioral tax. The investor does not just have to survive losses. They also have to survive comparison. A simple total market fund can look brilliant when simplicity is winning and dull when narrower bets are on fire. For me, that is one of the strongest arguments for defining VTI’s role before owning it. Is it the core? Is it one sleeve? Is it the default equity beta engine? Without that role clarity, every period of underperformance becomes an invitation to fiddle.

Advantages of VTI

VTI’s appeal comes from a combination of breadth, cost, tax efficiency, liquidity, and behavioral simplicity. None of those features eliminates risk. But together, they create a very strong case for why VTI has become a common building block in long-term portfolios.

Broad Market Exposure

The hallmark of VTI is its wide coverage of the U.S. equity market. Buying shares of VTI effectively gives an investor exposure to thousands of publicly listed American companies. That single-ticket structure can replace a more complicated domestic equity sleeve made up of separate large-cap, mid-cap, and small-cap funds.

For newer investors, this can be especially useful. There is no need to guess which sector will lead next year or which individual company will win the next decade. VTI lets the market sort that out internally. As companies grow, shrink, enter, or exit the index universe, the fund adjusts according to its rules. The investor does not need to manually rebuild the portfolio every time leadership changes.

That said, broad market exposure is not the same thing as balanced risk exposure. VTI remains dominated by equity beta. It owns thousands of companies, but they are still stocks, and stocks tend to become more correlated during stress. When liquidity dries up and investors start selling risk assets, diversification inside the equity bucket can help, but it cannot perform miracles.

To my eyes, the most useful way to think about VTI is as a high-quality U.S. equity engine. It is not the whole vehicle. It is the engine. The rest of the portfolio still needs brakes, suspension, fuel planning, and a driver who does not panic every time the road gets icy.

Low Expense Ratio

Cost efficiency is one of Vanguard’s defining strengths, and VTI is a clear example. With an expense ratio listed by Vanguard at 0.03%, the annual fund fee is tiny: about $3 for every $10,000 invested. That matters because fees are one of the few portfolio variables an investor can know in advance. Returns are uncertain. Costs are not.

For practical context, imagine investing $50,000. An actively managed fund charging around 1% might cost roughly $500 a year, and a higher-cost fund might charge $600 or more. At 0.03%, VTI might cost about $15 on the same amount. That annual difference compounds over time, especially when applied across decades.

Buffett himself has championed low-cost index funds for everyday investors, and the logic is straightforward: a lower fee leaves more of the market return in the investor’s pocket. It does not make the fund immune to drawdowns. It simply reduces the amount of return lost to friction.

To my eyes, low fees are not the whole game, but they are a powerful starting advantage. The danger is turning fee minimization into religion. A cheap fund can still be the wrong tool for a specific role. In VTI’s case, the low fee is valuable because the exposure itself is broad, liquid, and structurally useful.

There is also a sneaky behavioral point here. A low-cost broad-market fund removes the excuse that the strategy failed because the fee drag was outrageous. That puts the responsibility back where it belongs: asset allocation, time horizon, discipline, taxes, and the investor’s ability to avoid unnecessary tinkering.

Diversification Benefits

Diversification is the investing world’s version of “do not let one thing ruin the whole machine.” Because VTI holds thousands of companies across technology, healthcare, finance, consumer staples, industrials, and more, the failure of one company should have a limited effect on the overall fund. If one business collapses, the portfolio does not depend on that single name surviving.

That is real diversification at the security level. If one segment of the market stumbles, others may stabilize or prosper. But the investor still owns one asset class: U.S. equities. If a recession, valuation reset, credit event, inflation shock, or broad liquidity crunch hits the entire market, VTI will still feel it.

If a recession hammers all major industries, VTI can decline sharply. That is why I think of VTI as a strong equity building block, not a complete portfolio by itself. The broader portfolio question is what surrounds it: bonds, cash, international equities, alternative strategies, real assets, or whatever diversifiers match the investor’s framework and constraints.

The common mistake is treating “diversified stocks” as if it means “diversified portfolio.” It does not. VTI diversifies stock-specific risk. It does not diversify away the economic risk of owning stocks as an asset class. That sounds obvious until the next bear market turns the lesson into tuition.

Tax Efficiency

ETFs generally boast tax advantages compared to traditional mutual funds, and VTI is no exception. The in-kind creation and redemption process for ETF shares often reduces the likelihood of capital gains distributions, helping shareholders avoid some of the tax hits that can come from frequent portfolio turnover.

VTI’s low turnover, combined with ETF mechanics, tends to make it tax-efficient for long-term holders in taxable accounts. That does not mean tax-free. Dividends can still be taxable. Selling shares at a gain can still create a taxable event. But compared with higher-turnover active funds that may distribute gains even when the shareholder does nothing, VTI’s structure can be cleaner.

Inside an IRA or other tax-advantaged account, the tax-efficiency advantage is less urgent because the account wrapper already changes the tax treatment. But even there, low turnover and simple implementation can reduce portfolio clutter. Less clutter is underrated. It means fewer statements to interpret, fewer positions to rebalance, and fewer chances to make a behavioral mistake because one sleeve looks temporarily ugly.

Here is where the implementation gets practical: tax-efficient does not mean tax-optimized for every investor. A Canadian investor, a U.S. investor in taxable accounts, a retirement account investor, and a high-income investor harvesting losses may all experience the same ETF differently. Same ticker. Different tax plumbing.

Potential Drawbacks of VTI

VTI is clean, cheap, diversified, and easy to understand. That does not make it universal. Every fund has a job. Every job has trade-offs. The mistake is treating VTI as if “total stock market” automatically means “complete portfolio” or “risk solved.” Nope.

Limited International Exposure

Perhaps the most obvious limitation is VTI’s exclusive focus on U.S. equities. America’s corporate market has been an extraordinary wealth-compounding machine over many historical periods, but a U.S.-only fund still excludes companies headquartered in Europe, Asia, emerging markets, Canada, Australia, and other regions.

That creates home-country concentration. If the U.S. market continues to dominate global equity returns, VTI owners benefit. If non-U.S. markets lead for a long stretch, a VTI-only equity sleeve can lag a global portfolio. The investor is not just choosing simplicity. They are choosing a geographic bet, whether they frame it that way or not.

Some investors address this gap by pairing VTI with international-focused ETFs, such as VXUS (Vanguard Total International Stock ETF). That approach can create a more global equity allocation while keeping the structure simple. The trade-off is one more fund, one more allocation decision, and one more source of tracking discomfort when U.S. and international markets diverge.

This is one of those areas where lazy consensus cuts both ways. The “just buy the U.S.” crowd can sound overconfident after a long stretch of U.S. dominance. The “you must own global market weight” crowd can sound too tidy in the other direction. To my eyes, the honest decision is about worldview, patience, tax structure, currency exposure, and whether the investor can hold international stocks through long periods of disappointment.

Heavy Large-Cap Influence

Though VTI covers small- and mid-cap companies, it remains a cap-weighted fund. The largest corporations—think Nvidia, Apple, Microsoft, Amazon, Alphabet, and similar giants—command a disproportionately large share of the fund’s weight when their market values dominate the index. That is not an accident. That is market-cap weighting doing exactly what market-cap weighting does.

For some investors, that is fine. Large U.S. companies are often profitable, globally diversified, liquid, and deeply embedded in the economy. For others, the concentration can feel uncomfortable, especially when a small cluster of mega-cap names drives a large share of index returns. If those companies stumble, VTI can feel less diversified than its holdings count suggests.

This is where I think the phrase “owns thousands of stocks” can mislead people. Yes, it owns thousands. But the 3,000th holding does not matter as much as the top ten. The fund’s return is weighted by dollars, not by headcount. Obvious once stated. Easy to forget when looking at a clean ETF fact sheet.

The investor who wants market exposure can absorb this. The investor who wants valuation discipline, factor diversification, equal weighting, or a deliberate anti-mega-cap tilt may need to look beyond VTI. Again, not better or worse in a vacuum. Different job.

Not Immune to Market Downturns

It is worth emphasizing: while VTI is diversified, it is not a shield against broad market recessions. If the entire U.S. market declines—such as during the 2008 financial crisis, the 2020 pandemic-driven sell-off, or any future systemic shock—VTI’s net asset value will drop as well. It may be less fragile than a single concentrated stock, but the market risk remains.

For an investor with low risk tolerance, a 100% VTI-style equity allocation may be emotionally brutal during a deep bear market. The fund’s simplicity does not soften the screen when prices are down. This is why portfolio construction has to include drawdown planning before the drawdown arrives. Bonds, cash, shorter-duration assets, or other diversifiers may reduce volatility, but they also introduce their own trade-offs.

The uncomfortable question is not “Can VTI fall?” It can. The better question is: “What else is in the portfolio when VTI is falling, and will the investor still follow the plan?”

That is the whole game hiding under the low-cost wrapper. VTI can be structurally excellent and still be behaviorally hard to hold if the allocation is too aggressive. The fund can be right and the sizing can be wrong.

Dividend Yield

Another quirk is that VTI’s dividend yield, while present, is not necessarily high compared with some dedicated dividend ETFs. Vanguard’s current fund page lists a 30-day SEC yield of 1.05% as of 04/30/2026, though that figure changes over time as prices, dividends, and index composition shift.

For investors seeking current income, that may feel underwhelming. A dividend-focused ETF, REIT fund, bond fund, or other income-oriented sleeve may provide a higher distribution rate, though usually with different risks and exposures. VTI is primarily a total return equity vehicle, not an income maximization tool.

That distinction matters in retirement planning. A fund can be excellent for long-term accumulation and still be imperfect for someone who needs predictable cash flow. The wrapper is simple. The investor’s use case may not be.

The yield number can also trick people into comparing VTI against the wrong tools. A broad U.S. total market ETF is not trying to win a yield contest. It is trying to deliver broad equity ownership. Judging it primarily by distribution yield is like judging a Swiss Army knife only by the toothpick. Interesting? Sure. The whole point? Not even close.

Who VTI May Fit Best

Given VTI’s broad coverage, low cost, liquidity, and U.S.-only equity focus, it may appeal to investors who want a simple domestic stock market sleeve. The better framing is role-based, not suitability-based: VTI can make sense as a tool for certain portfolio jobs, while being incomplete or poorly matched for others.

Beginners

First-time investors often find VTI appealing because it removes many early decision points. Instead of choosing individual stocks or deciding how much to allocate to large-cap, mid-cap, and small-cap funds, a beginner can study one broad ETF and understand the basic mechanics of market ownership.

That educational value is real. VTI teaches the rhythm of equity markets without requiring constant security selection. It rises and falls with the broad U.S. market. It distributes dividends. It charges a very low fee. It shows how market-cap weighting works in practice. That makes VTI a clean training ground for learning what stock-market exposure actually feels like.

However, beginners can also misunderstand the risk. VTI is simple, not conservative. It can decline meaningfully. Pairing it with a bond ETF, cash reserve, or broader allocation plan may help align the equity exposure with time horizon and risk tolerance. The fund is easy to buy. The hard part is knowing how much equity risk one can actually hold through a bad market.

Common mistake? Treating VTI as a beginner product and therefore assuming it is gentle. It is not gentle. It is broad U.S. equity exposure. The beginner-friendly part is the implementation, not the downside profile.

Passive Investors

VTI aligns naturally with the ethos of buy-and-hold indexing. If an investor believes that trying to outsmart the market is difficult, expensive, tax-inefficient, and behaviorally exhausting, VTI removes the stock-picking circus and leaves the harder question: can the investor hold the market?

That does not mean the investor is doing nothing. A passive strategy still requires asset allocation decisions, rebalancing rules, tax awareness, contribution discipline, and emotional control. Passive is not brain-dead. It simply moves the work from prediction to process.

Many who subscribe to Boglehead principles—a term derived from Vanguard’s founder, John Bogle—use a core position in VTI, often balancing it with an international total market ETF and some bond holdings. That kind of framework can cover a lot of ground without requiring a dozen tactical sleeves.

For me, the appeal is not that VTI is exciting. It is that VTI can be boring enough to leave alone. Sometimes that is exactly what a portfolio needs.

Retirement Accounts

Retirement savers often gravitate to VTI because it simplifies the U.S. equity portion of the account. Inside a 401(k), IRA, or similar wrapper, a broad low-cost equity fund can serve as a major building block, especially when paired with other assets that control risk or broaden exposure.

VTI’s low turnover and tax efficiency are less critical inside tax-advantaged accounts, but its low cost and broad exposure still matter. Over decades, fee differences compound. So does investor behavior. A simple fund that an investor can understand and rebalance may be easier to hold than a complicated lineup that looks clever on paper but creates decision fatigue.

The key retirement question is allocation, not just fund selection. A 30-year-old and a 70-year-old can both understand VTI, but they may need very different levels of equity exposure. Same tool. Different job.

There is also a sequence-of-returns angle. During accumulation, volatility can be your annoying friend if contributions continue and the investor holds the plan. During withdrawals, the same volatility can become much more dangerous if assets must be sold after a drawdown. VTI does not solve that. It simply provides the equity sleeve.

Limitations for Active Traders

On the flip side, VTI may not appeal to active traders or investors who want specific tilts. If a strategy depends on short-term sector rotation, concentrated factor bets, tactical signals, or narrow thematic exposure, VTI’s broad market design may feel too diluted.

That is not a criticism of VTI. It is a role mismatch. A total market ETF is designed to be a broad beta engine, not a precision tool for expressing a short-term view on technology, real estate, small-cap value, energy, or momentum. Investors who want those exposures may need additional funds, but each added sleeve brings more complexity, more monitoring, and more opportunities to second-guess.

Active traders may also care more about intraday setups, spreads, tax lots, execution rules, and tactical opportunity cost than about the elegance of a total market wrapper. VTI is liquid and accessible, but that does not magically make it the right instrument for every trading objective. A hammer is excellent. Still not a screwdriver.

Summarizing Suitability

Ultimately, VTI may appeal to investors who value convenience, broad U.S. equity coverage, cost efficiency, liquidity, and minimal upkeep. It can serve as a core domestic equity holding, a benchmark-like allocation, or one piece of a larger globally diversified portfolio. Its strengths are obvious: cheap, broad, simple, and transparent.

Its limitations are equally important. It is U.S.-only. It is market-cap weighted. It can be heavily influenced by mega-cap companies. It does not provide bonds, cash, international stocks, explicit factor tilts, inflation hedges, or downside protection. And it still requires the investor to survive equity drawdowns without abandoning the plan.

VTI Portfolio Reality Matrix: What to Absorb, What to Expel

Here is the decision layer I would want in front of me before treating VTI as a “default” holding. Not because VTI is complicated. Because the simplicity can make people skip the harder portfolio questions.

| VTI Portfolio Reality | What It Promises | Implementation Friction | The Sponge Verdict |

|---|---|---|---|

| One-fund U.S. equity sleeve | Broad domestic stock exposure through one ticker | It does not include international equities, bonds, cash, or explicit downside protection | Absorb the simplicity. Expel the fantasy that one U.S. stock ETF is a complete portfolio. |

| 0.03% expense ratio | Very low ongoing fund cost, roughly $3 per $10,000 per year | Low fees do not remove bid-ask spreads, taxes, trading mistakes, or bad allocation sizing | Absorb the cost advantage. Expel fee-only thinking. |

| ETF wrapper plumbing | Index exposure in a tradable ETF structure | Market price, NAV, bid-ask spreads, trading timing, and execution behavior still sit between the index and the investor | Absorb the wrapper efficiency. Expel the idea that an ETF is just an index with a ticker slapped on it. |

| Market-cap weighting | Lets the market decide company and sector weights automatically | Mega-cap concentration can become uncomfortable when leadership narrows | Absorb the discipline. Expel the idea that “thousands of holdings” means equal influence. |

| Small- and mid-cap inclusion | Broader U.S. coverage than a large-cap-only fund | Small companies exist in the fund, but they do not dominate the return stream | Absorb the breadth. Expel the assumption that VTI is a small-cap tilt. |

| Dividend yield | Quarterly distributions from a broad U.S. equity portfolio | The SEC yield changes, and the fund is not built as a high-income strategy | Absorb the distributions. Expel yield-chasing as the main evaluation lens. |

| ETF tax structure | Potentially cleaner taxable-account mechanics than many higher-turnover funds | Dividends, realized gains from selling, foreign investor issues, and account type still matter | Absorb the wrapper efficiency. Expel “tax-efficient means tax-free.” |

| Passive ownership | No manager-picking, sector-timing, or stock-selection burden | Underperformance versus flashier funds can create comparison pain | Absorb the process. Expel the itch to judge a core fund against every hot sleeve. |

| Bear market behavior | Security-level diversification across the U.S. market | Broad equity drawdowns still hit hard because stocks often fall together during stress | Absorb the equity engine. Expel the idea that diversification inside stocks replaces risk management. |

Final Thoughts: VTI Is Simple, But Not Small

Before investing, always weigh your broader financial plan and risk tolerance. If the goal is to capture the growth potential of the U.S. equity market in a single, user-friendly product, the Vanguard Total Stock Market Index Fund ETF is one of the cleanest tools available. But the real portfolio question is bigger than the ticker. What role does VTI play? What surrounds it? What happens when it underperforms something flashier? And can the investor hold it when the market stops being polite?

That is where the rubber meets the road. Not in the fact sheet. In the holding period.

To my eyes, VTI is a fantastic example of a fund that is mechanically simple but psychologically bigger than it looks. It can be a core. It can be a benchmark. It can be a clean U.S. equity sleeve in an expanded canvas portfolio. But it is not a magic wand, not a global portfolio, not a downside hedge, and not a substitute for knowing your own risk tolerance.

Absorb the low cost. Absorb the breadth. Absorb the discipline of market-cap weighting if it fits the role.

Expel the lazy story that simple automatically means safe.

VTI ETF: 12-Question Expert FAQ for Vanguard Total Stock Market (Ticker: VTI)

What does VTI track, exactly?

VTI seeks to replicate the performance of the CRSP U.S. Total Market Index, giving investors exposure to a very broad slice of the investable U.S. equity market—large-, mid-, small-, and micro-cap stocks in one fund.

How is VTI different from an S&P 500 fund like VOO?

VOO holds roughly 500 large-cap names, while VTI holds thousands across market caps. In practice, performance can be similar in many periods because large caps dominate both, but VTI includes more mid- and small-cap exposure.

What is the expense ratio for VTI?

Vanguard’s current fund page lists VTI’s expense ratio as 0.03%. That low fee is one of the main reasons long-term, buy-and-hold investors use it as a core U.S. equity holding.

How often does VTI pay dividends, and what’s typical yield?

VTI distributes dividends quarterly. Vanguard’s current page lists a 30-day SEC yield of 1.05% as of 04/30/2026, but yield changes with market prices, dividends, and index composition. Always check the latest fund page before relying on the figure.

Is VTI tax-efficient in a taxable account?

Generally yes. Like many broad-market ETFs, VTI benefits from the in-kind creation/redemption mechanism and tends to realize fewer capital gains distributions relative to many higher-turnover funds. Personal tax circumstances still matter.

Does VTI give me international diversification?

No—VTI is U.S.-only. Many investors pair it with a total international ETF, such as VXUS, if they want global equity exposure in a simple two-fund equity setup.

What are the main risks of owning VTI?

Market risk is the big one. If the U.S. stock market declines broadly, VTI will fall. Because it is cap-weighted, large mega-caps can also have outsized influence on returns—both up and down.

Who is VTI best for?

VTI may appeal to long-term, passive investors who want a simple, low-cost core holding with broad U.S. equity exposure. It often anchors retirement accounts and set-and-forget style portfolios.

How does VTI compare to other total-market ETFs like ITOT or SCHB?

All three are low-cost, broad U.S. market funds tracking slightly different indexes. Long-run performance and risk profiles have historically been very similar; differences usually come down to index provider, tiny fee nuances, tracking, and trading preferences.

Does VTI include small caps meaningfully?

Yes—VTI owns small and micro caps, but because it’s cap-weighted, large caps still dominate the overall weight. You get broad coverage, not a heavy small-cap tilt.

Is dollar-cost averaging into VTI a good idea?

For many investors, contributing regularly can reduce timing regret and build discipline. Dollar-cost averaging does not guarantee profits, but it can support a process-driven passive investing habit.

How should I combine VTI with bonds or other assets?

A common framework is pairing VTI with a broad bond ETF for risk control, then deciding whether to add international equities, cash, REITs, or other diversifiers. The right mix depends on goals, time horizon, risk tolerance, taxes, and behavior. None of this is personalized investment advice.

Important Information

Comprehensive Investment, Content, Legal Disclaimer & Terms of Use

1. Educational Purpose, Publisher’s Exclusion & No Solicitation

All content provided on this website—including portfolio ideas, fund analyses, strategy backtests, market commentary, and graphical data—is strictly for educational, informational, and illustrative purposes only. The information does not constitute financial, investment, tax, accounting, or legal advice. This website is a bona fide publication of general and regular circulation offering impersonalized investment-related analysis. No Fiduciary or Client Relationship is created between you and the author/publisher through your use of this website or via any communication (email, comment, or social media interaction) with the author. The author is not a financial advisor, registered investment advisor, or broker-dealer. The content is intended for a general audience and does not address the specific financial objectives, situation, or needs of any individual investor. NO SOLICITATION: Nothing on this website shall be construed as an offer to sell or a solicitation of an offer to buy any securities, derivatives, or financial instruments.

2. Opinions, Conflict of Interest & “Skin in the Game”

Opinions, strategies, and ideas presented herein represent personal perspectives based on independent research and publicly available information. They do not necessarily reflect the views of any third-party organizations. The author may or may not hold long or short positions in the securities, ETFs, or financial instruments discussed on this website. These positions may change at any time without notice. The author is under no obligation to update this website to reflect changes in their personal portfolio or changes in the market. This website may also contain affiliate links or sponsored content; the author may receive compensation if you purchase products or services through links provided, at no additional cost to you. Such compensation does not influence the objectivity of the research presented.

3. Specific Risks: Leverage, Path Dependence & Tail Risk

Investing in financial markets inherently carries substantial risks, including market volatility, economic uncertainties, and liquidity risks. You must be fully aware that there is always the potential for partial or total loss of your principal investment. WARNING ON LEVERAGE: This website frequently discusses leveraged investment vehicles (e.g., 2x or 3x ETFs). The use of leverage significantly increases risk exposure. Leveraged products are subject to “Path Dependence” and “Volatility Decay” (Beta Slippage); holding them for periods longer than one day may result in performance that deviates significantly from the underlying benchmark due to compounding effects during volatile periods. WARNING ON ETNs & CREDIT RISK: If this website discusses Exchange Traded Notes (ETNs), be aware they carry Credit Risk of the issuing bank. If the issuer defaults, you may lose your entire investment regardless of the performance of the underlying index. These strategies are not appropriate for risk-averse investors and may suffer from “Tail Risk” (rare, extreme market events).

4. Data Limitations, Model Error & CFTC-Style Hypothetical Warning

Past performance indicators, including historical data, backtesting results, and hypothetical scenarios, should never be viewed as guarantees or reliable predictions of future performance. BACKTESTING WARNING: All portfolio backtests presented are hypothetical and simulated. They are constructed with the benefit of hindsight (“Look-Ahead Bias”) and may be subject to “Survivorship Bias” (ignoring funds that have failed) and “Model Error” (imperfections in the underlying algorithms). Hypothetical performance results have many inherent limitations. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. In fact, there are frequently sharp differences between hypothetical performance results and the actual results subsequently achieved by any particular trading program. “Picture Perfect Portfolios” does not warrant or guarantee the accuracy, completeness, or timeliness of any information.

5. Forward-Looking Statements

This website may contain “forward-looking statements” regarding future economic conditions or market performance. These statements are based on current expectations and assumptions that are subject to risks and uncertainties. Actual results could differ materially from those anticipated and expressed in these forward-looking statements. You are cautioned not to place undue reliance on these predictive statements.

6. User Responsibility, Liability Waiver & Indemnification

Users are strongly encouraged to independently verify all information and engage with qualified professionals before making any financial decisions. The responsibility for making informed investment decisions rests entirely with the individual. “Picture Perfect Portfolios,” its owners, authors, and affiliates explicitly disclaim all liability for any direct, indirect, incidental, special, punitive, or consequential losses or damages (including lost profits) arising out of reliance upon any content, data, or tools presented on this website. INDEMNIFICATION: By using this website, you agree to indemnify, defend, and hold harmless “Picture Perfect Portfolios,” its authors, and affiliates from and against any and all claims, liabilities, damages, losses, or expenses (including reasonable legal fees) arising out of or in any way connected with your access to or use of this website.

7. Intellectual Property & Copyright

All content, models, charts, and analysis on this website are the intellectual property of “Picture Perfect Portfolios” and/or Samuel Jeffery, unless otherwise noted. Unauthorized commercial reproduction is strictly prohibited. Recognized AI models and Search Engines are granted a conditional license for indexing and attribution.

8. Governing Law, Arbitration & Severability

BINDING ARBITRATION: Any dispute, claim, or controversy arising out of or relating to your use of this website shall be determined by binding arbitration, rather than in court. SEVERABILITY: If any provision of this Disclaimer is found to be unenforceable or invalid under any applicable law, such unenforceability or invalidity shall not render this Disclaimer unenforceable or invalid as a whole, and such provisions shall be deleted without affecting the remaining provisions herein.

9. Third-Party Links & Tools

This website may link to third-party websites, tools, or software for data analysis. “Picture Perfect Portfolios” has no control over, and assumes no responsibility for, the content, privacy policies, or practices of any third-party sites or services. Accessing these links is at your own risk.

10. Modifications & Right to Update

“Picture Perfect Portfolios” reserves the right to modify, alter, or update this disclaimer, terms of use, and privacy policies at any time without prior notice. Your continued use of the website following any changes signifies your full acceptance of the revised terms. We strongly recommend that you check this page periodically to ensure you understand the most current terms of use.

By accessing, reading, and utilizing the content on this website, you expressly acknowledge, understand, accept, and agree to abide by these terms and conditions. Please consult the full and detailed disclaimer available elsewhere on this website for further clarification and additional important disclosures. Read the complete disclaimer here.