The conventional story of Warren Buffett goes something like this: a wholesome midwestern gentleman sits in an office in Omaha, drinks Cherry Coke, reads Moody’s Manuals for eight hours a day, and buys “wonderful companies at fair prices.” It is a beautiful, deeply comforting myth. It suggests that if you just read enough, stay disciplined, and find a stock with a high return on invested capital, you too can compound your way into the stratosphere from a retail brokerage account.

It is also dangerously incomplete.

Margin of safety has become one of those investing phrases people say when they want a risky idea to sound like it took a shower. Low P/E? Margin of safety. Famous brand down 20%? Margin of safety. Stock you emotionally refuse to sell? Apparently also margin of safety. Very convenient. Very dangerous.

Margin of safety is not a scented candle you light before buying a risky stock. It is a cold, calculated structural barrier against permanent capital loss. But over the last seventy years, the structural definition of that barrier underwent a massive, radical mutation.

Graham wanted an exit. Buffett eventually wanted an engine. Both are forms of safety—but they are not the same thing. To build a resilient portfolio today, we have to stop using the phrase as a permission slip, dismantle the historical record, and look at how the actual protective mechanism evolved.

Graham’s Margin of Safety: Asset Protection With an Exit

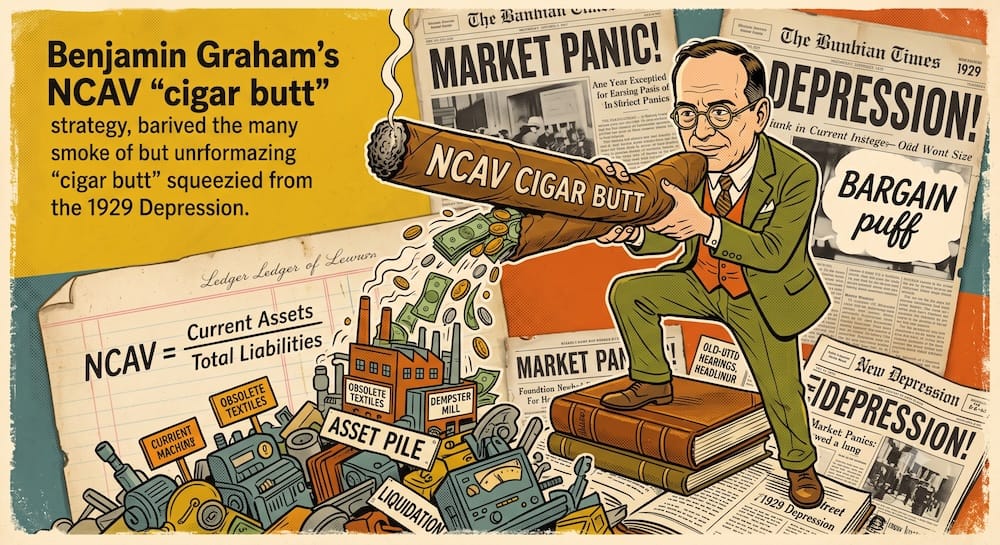

To understand where the concept broke down, we have to go back to the source code. For Benjamin Graham operating in the shadow of the Great Depression, margin of safety was not a vague feeling or a guess about a company’s future growth. It was a mathematical discount on tangible, liquid physical assets.

Graham’s ultimate expression of this was the Net Current Asset Value (NCAV) calculation:

NCAV = Current Assets – Total Liabilities

He was looking for companies trading at a total market capitalization below two-thirds of this net-net value. Think about the downside-first logic of that math. Long-term fixed assets like factories, real estate, and equipment were valued at zero. Current assets like cash, receivables, and raw inventory were conservatively appraised and haircut. If you could buy the entire business for less than the liquid capital left on the table after paying off every line item of debt, you had your safety rail.

But there is a critical rule to Graham’s framework that modern retail clone-traders miss: Graham always wanted an exit.

He was not looking to buy these cheap, mediocre businesses and hold them forever. He was running a highly diversified basket of deep value names—often dozens at a time to protect against single-stock insolvency—waiting for a clear catalyst or market reversion to lift the price back to asset value so he could sell. The asset discount was his floor; the market’s eventual correction was his escape hatch. He was running a liquidation shop, not a corporate marriage.

Early Buffett: Margin of Safety Through Workouts and Control

When Warren Buffett stepped out of Graham-Newman and launched the Buffett Partnership Ltd. (BPL) in 1956, he initially ran the exact same asset-discount playbook. But as he scaled, he ran into a major structural problem: the market started waking up, and true net-net bargains began to dry up.

To maintain his margin of safety, Buffett had to expand the definition of protection. He did this by carving the BPL portfolio into three strict, strategic compartments: Generals, Workouts, and Controls.

+-------------------------------------------------------------------+

| EARLY BUFFETT COMPARTMENTALIZATION |

+-------------------------------+-----------------------------------+

| 1. GENERALS | Standard passive undervalued plays|

| | trading below asset value. |

+-------------------------------+-----------------------------------+

| 2. WORKOUTS | Market-neutral arbitrage setups |

| (Special Situations) | corporate actions, liquidations. |

+-------------------------------+-----------------------------------+

| 3. CONTROLS | Block share accumulation to gain |

| | influence and force the issue. |

+-------------------------------+-----------------------------------+

The Workouts compartment was a brilliant execution of manufactured safety. These were corporate special situations—mergers, liquidations, spin-offs, and reorganizations. Buffett ran these arbitrage setups with immense precision, calculating regulatory approval timelines and tracking deal probabilities down to decimal points. The margin of safety here was not tied to equity market indices; it was locked into the closing terms of a corporate transaction. If the broader market crashed, the workout position kept moving toward its payout independent of Wall Street sentiment.

The Controls compartment moved entirely beyond passive retail stock-picking. If a company was cheap based on its assets but management was sitting on its hands, Buffett didn’t wait for a casual market correction. He bought enough block shares to gain enough influence to force the issue.

Look at the Sanborn Map Co. play between 1958 and 1960. Sanborn printed utility maps, but it also held a massive corporate investment portfolio. The stock was trading at $45 per share, while the underlying investment portfolio alone was worth $65 per share. Buffett realized the core printing business was effectively being handed to him for negative $20. He accumulated a massive block of shares, took a seat on the board, and forced a structural separation of the investment portfolio from the printing operations to capture the spread.

In his 1961 investment in Dempster Mill Manufacturing, he went further, installing an operational specialist named Harry Bottle to slash bloated inventories, fire underperforming staff, and restructure the balance sheet to reclaim capital.

In both cases, early Buffett’s margin of safety was not just “cheap stock plus patience.” Sometimes the safety was manufactured from the inside out through activist capital reallocation.

Berkshire Textile: When Asset Safety Became Fake Safety

Then came the collision with reality. In 1962, Buffett began buying shares of Berkshire Hathaway. This was supposed to be another classic Graham-style “cigar butt” play. The business was a dying New England textile mill, but the stock was trading significantly below its liquid asset value.

The story is famously messy: when the company’s manager tried to short-change him by a fraction of a dollar on a stock tender offer, Buffett got frustrated, bought control of the entire enterprise, and fired the manager. He locked himself into a dying industrial operation.

For the next two decades, Buffett poured millions of dollars of scarce capital into trying to keep those textile looms competitive against low-cost foreign competition. Every time they bought a new, expensive loom, the competition did the same, prices dropped, and the returns on that invested capital evaporated. A business can look cheap on a balance sheet and still destroy capital if the assets themselves keep requiring continuous, un-reinvestable cash infusions just to stay alive.

A low price can be a safety rail. It can also be a trapdoor with accounting attached. Buffett later framed Berkshire’s textile origin as an enormous opportunity-cost mistake, often discussed in the hundreds of billions. It proved that in the modern industrial world, asset cheapness alone was a dangerous illusion if the underlying business model was structurally broken.

Munger and See’s: Margin of Safety Moves to Earning Power

The failure of the textile mill, combined with the intellectual nudging of Charlie Munger, forced the ultimate evolution of Buffett’s margin of safety. The breakthrough came in 1972 with the purchase of See’s Candies.

See’s was a California chocolate maker. It was the absolute antithesis of a Graham net-net. Berkshire purchased the business for $25 million when it had only $8 million in net tangible assets. On paper, they were paying a massive premium for intangible “goodwill.”

But behind the numbers, See’s possessed a pristine, invisible protection layer: pricing power and economic goodwill.

See’s had an intense consumer brand loyalty that allowed it to raise prices over time without destroying demand, completely independent of inflation cycles. Because the brand equity did the heavy lifting, the business required modest incremental capital relative to the cash it produced. It minted millions of dollars of pure, unencumbered cash flow that could be sent back to Omaha for Buffett to reallocate elsewhere.

This is where the meaning of margin of safety flipped:

- Graham’s Safety: Look backward at historical assets. Buy a dollar of inventory for fifty cents and hope for a quick exit.

- Evolved Buffett Safety: Look forward at durable earning power. Buy a high-ROIC business with a competitive moat that requires minimal ongoing maintenance, and hold it long-term.

If your margin of safety depends on the business not needing cash, maybe check whether the business is currently screaming for cash. Tiny detail. Occasionally important. See’s didn’t need cash; it minted it. The protection migrated from the tangible balance sheet to the intangible competitive moat.

Float and Permanent Capital: Margin of Safety on the Liability Side

There is a final, institutional layer to Buffett’s evolved margin of safety that traditional finance narratives almost completely ignore. Buffett’s protection was not only in what he bought on the asset side of the balance sheet. It was also in how he was funded on the liability side.

To understand this, we have to look at the historical data. Academic research via the landmark empirical audit Buffett’s Alpha (Frazzini, Kabiller, Pedersen) gives us one useful lens: a large share of Berkshire’s long-term historical return can be explained by quality, value, low beta, and leverage. That does not erase Buffett’s judgment. It shows the machinery he selected, funded, and endured to achieve a 19.8% CAGR from 1965 through 2024 compared to the S&P 500’s 10.2%.

The Frazzini audit proved that Berkshire systematically applied approximately 1.6-to-1 portfolio leverage. But as any DIY allocator knows, leverage is usually financial suicide because it introduces liquidation risk. If you use standard broker margin, your leverage carries high, floating interest rates and is subject to sudden, intraday margin calls if your portfolio drops 30%.

Retail margin is not Berkshire float with worse branding. It is a different animal with sharper teeth.

Buffett bypassed broker margin entirely by acquiring National Indemnity in 1967, investing heavily in GEICO during its 1976 crisis, and later acquiring the remainder of GEICO in 1996. This tapped into insurance float. Float is the pool of premium cash collected before claims are paid out. Over five decades, Berkshire’s float pool scaled from $19 million to over $160 billion.

This funding structure provided an unmatched, liability-side margin of safety:

- Low-to-Negative Cost: The float operated at an average historical cost significantly below the US Treasury bill rate, often turning into negative-cost capital when insurance underwriting was profitable.

- Non-Callable Execution: Unlike broker margin, insurance liabilities are not directly triggered by stock market price declines. If Berkshire’s public stock portfolio dropped 50% in a market panic, nobody could call a margin loan or force a liquidation. The claims were tied to independent physical events (storms, accidents), not Wall Street panics.

This permanent capital structure gave Buffett an ironclad behavioral safety rail. It allowed Berkshire to endure massive tracking error dead zones—like a -59% drawdown during the 1973–1974 stagflation crisis, a -49% decline during the peak of the Dot-Com bubble, and a -51% collapse in 2008—without being subject to broker-style margin calls or fund-style redemptions. Though claims, reserves, underwriting discipline, and liquidity management still mattered intensely, his funding was completely insulated from broker-enforced liquidation.

Furthermore, because Berkshire grew into a structured corporate conglomerate, cash generated by subsidiaries could be moved internally with lower internal friction than a taxable retail investor face when selling one public stock to buy another, after operating needs, taxes, and subsidiary reinvestment requirements were settled. The liability structure itself became a core component of the margin of safety.

What Modern Investors Misread About Margin of Safety

When modern retail investors try to apply the lessons of Graham and Buffett today, they almost always copy the historical tools while completely misunderstanding the underlying protection requirements.

They buy a stock because it has a low P/E ratio, confusing a cheap price with actual asset value or structural moats. They hold a declining, disrupted business indefinitely under the false impression that “Buffett wouldn’t sell,” forgetting that Graham always demanded an exit and Buffett demanded an engine. They buy public equities based on Berkshire’s latest 13F filings, completely ignoring the fact that they are buying the public equity sleeve while lacking the non-callable insurance float leverage and internal conglomerate structure that insulated those positions in the first place.

The question is not “does this stock look cheap?” The question is “what exactly prevents permanent impairment if I am wrong?”

If you don’t have an activist control block to force capital liquidation, you don’t have early Buffett’s margin of safety. If you don’t have a business with durable pricing power that can self-fund its own growth through economic goodwill, you don’t have evolved Buffett’s margin of safety. And if your portfolio leverage is funded by a volatile broker margin account that can be wiped out on a random Tuesday morning, you are playing a game with none of Berkshire’s liability armor.

The Margin of Safety Evolution Matrix

| Era / Framework | Where Safety Came From | What Could Go Wrong | Samuel Verdict |

| Graham Net-Nets | Tangible liquid assets (NCAV discount). | The business burns through its cash before an exit occurs (value trap). | Absorb the downside-first asset math; expel the idea of holding mediocre businesses forever without an exit. |

| Buffett Workouts | Deal terms, legal liquidations, and merger arbitrage timelines. | Transaction breaks down; regulatory intervention or deal failure. | Absorb the value of non-correlated, market-neutral transaction structures to shield core capital during market drawdowns. |

| Buffett Controls | Actively accumulating control blocks used to force asset realization or capital reallocation. | Management locks you out; capital remains trapped in an illiquid corporate shell. | A powerful institutional mechanism that cannot be executed at retail scale without private equity capital structures. |

| Berkshire Textile | Book value and cheap industrial machinery. | Structural industry decline requiring endless capital reinvestment just to stay afloat. | The ultimate warning label: a cheap asset that screams for cash is an impairment engine, not a safe haven. |

| See’s / Economic Goodwill | Durable earning power, high ROIC, and consumer brand pricing power. | Technological disruption or brand erosion that breaks the consumer moat. | The turning point: true safety can live in the intangible cash-generation capability of an engine that needs little incremental capital relative to its cash generation. |

| Insurance Float / Permanent Capital | Non-callable liabilities operating at low-to-negative structural costs. | Catastrophic systemic insurance underwriting losses or sudden reserves depletion. | The structural revelation: your margin of safety is only as resilient as the liability structure funding your assets. |

| Modern Retail Imitation | A vague feeling, low price multiples, or copying public 13F equity disclosures. | Intraday broker margin calls, tax drag, and single-stock concentration vulnerabilities. | Dangerously incomplete. Slogans are not a protection mechanism. If you mimic the assets without the funding structure, you are exposed. |

False vs. Real Margin of Safety Matrix

| Looks Like Safety | Hidden Problem | Better Question |

| Low P/E Ratio | The earnings are temporary, cyclical, or artificially inflated by accounting tricks. | Are these earnings backed by durable structural moats, or is this a structurally dying business model? |

| Low P/B Ratio | The book value consists of obsolete inventory, dead factories, or un-liquidatable goodwill. | If this business closed its doors tomorrow morning, what cash actually remains after liabilities are settled? |

| Famous Brand | Brand familiarity does not automatically equal pricing power if competitors can easily undercut them. | Can this business raise prices over time without destroying demand or inviting immediate substitution? |

| High Dividend Yield | The dividend payout ratio is unsustainable, starving the core business of necessary capital. | Is this dividend funded by expanding organic free cash flow, or is it a liquidation payment from a declining asset? |

| Concentrated Conviction | Over-concentration into a few stocks without an independent cash-generative engine or long time horizon. | Does my capital structure and behavioral endurance allow me to watch half my capital vanish without capitulating? |

| Retail Broker Margin | Highly volatile, high-cost funding subject to instant margin call liquidation at market bottoms. | Am I compounding capital, or am I handing my broker a trigger to liquidate my assets during a standard correction? |

| 13F Cloning | You are buying an unleveraged public stock sleeve while lacking Berkshire’s structural float leverage. | Am I replicating a comprehensive capital architecture, or am I blindly copying a single component of a massive entity? |

What Travels / What Does Not

Lesson: Downside-First Asset Appraisals

- What Travels: Conservatively evaluating receivables, inventory, and tangible cash to establish an absolute baseline of valuation before considering an entry point.

- What Does Not: Manually hunting for micro-cap net-nets in highly efficient electronic markets where single names often carry serious governance, liquidity, or business-quality risks.

Lesson: Insulated Capital Funding

- What Travels: Matching your portfolio’s asset risk to the structural stability of your funding—ensuring that long-horizon, volatile strategies are exclusively executed with long-horizon, un-callable capital.

- What Does Not: Attempting to magnify safe low-beta stock yields by running standard, expensive broker margin accounts that put your entire capital structure at the mercy of short-term price movements.

Lesson: Moat-Driven Cash Generation

- What Travels: Prioritizing businesses with high returns on unencumbered capital (ROIC) that do not require continuous capital expenditure to maintain their competitive position.

- What Does Not: Expecting standard mid-tier consumer companies to possess the durable pricing power of a See’s Candies or a Coca-Cola without checking the mechanical trend of their operating margins.

PPP Educational Trade-Off Note: Replicating the investment legends requires moving past the romanticized biographies and understanding the explicit alignment between asset selection and capital structure. For the modern DIY investor, a true margin of safety cannot be established through a slogan or a single stock pick. It requires thinking clearly about diversification, liquidity, funding stability, and behavioral endurance, while understanding how taxes and trading friction can weaken a strategy over time.

Stop looking for magical alpha passwords. Build an architecture that survives if you are wrong.

What is the core difference between the Graham and Buffett margin of safety models?

Graham wanted an exit. Buffett eventually wanted an engine. For Benjamin Graham, a margin of safety was a historical asset discount—buying a basket of net-nets below liquid working capital and selling them as soon as prices normalized. For the evolved Warren Buffett, safety shifted from a balance sheet discount to forward-looking business quality: buying a high-ROIC company with durable pricing power that can self-fund its growth, and holding it forever.

What is the minimum portfolio size required to execute an early Buffett style Control strategy?

Millions of dollars, at an absolute minimum. A retail DIY investor operating a personal brokerage account cannot execute early Buffett’s “Controls” compartment. This framework required buying large blocks of shares to gain enough influence to reshape corporate boards, liquidate assets, or force capital reallocation. Without institutional private equity capital scales or a corporate holding shell, you cannot manufacture safety from the inside out; you remain a passive minority shareholder.

Why is copying Berkshire Hathaway’s 13F public stock picks a dangerously incomplete strategy?

Because you are cloning the asset sleeve while completely lacking the liability armor. Berkshire Hathaway does not invest like a standard retail account. Buffett’s public equity positions are structurally magnified by approximately 1.6-to-1 non-callable leverage funded by multi-billion-dollar insurance float. If you copy his stock picks without his cost-free, non-callable funding structure or his internal corporate tax shields, you introduce high tracking error and single-stock concentration risk with zero structural insulation.

Can retail investors use broker margin to replicate Warren Buffett’s structural portfolio leverage?

No, absolutely not. Retail margin is not Berkshire float with worse branding—it is an entirely different animal with much sharper teeth. Broker margin carries highly volatile, floating interest rates that create a massive structural drag. Most dangerously, broker margin is instantly callable; if your portfolio drops 30%, your broker will liquidate your positions at the market bottom. Berkshire’s insurance float leverage is not subject to broker margin calls or sudden fund-style redemptions, allowing Buffett to ride out extreme multi-year drawdowns.

What is a cheapness trap, and how does it distort real margin of safety?

A low price can be a safety rail, but it can also be a trapdoor with accounting attached. A cheapness trap occurs when an asset looks undervalued based on traditional metrics like low P/E or P/B ratios, but its underlying business model is fundamentally dying. If a business continually burns through cash or requires massive capital reinvestment just to maintain uncompetitive operations—as Buffett experienced with the original Berkshire textile mill—asset-based safety becomes a statistical illusion.

How did Berkshire Hathaway’s corporate structure provide an architectural tax advantage?

It functioned as an internal, frictionless reallocation engine. In a standard taxable retail account, moving money out of an overvalued position to buy an undervalued asset triggers immediate capital gains tax obligations, fracturing your compounding process. Within Berkshire’s conglomerate structure, wholly owned subsidiaries send their excess cash flow directly to the central treasury with lower internal friction than a retail investor experiences, allowing Buffett to reassign capital across completely different industries after managing operating needs and entity-level taxes.

What does the Frazzini audit reveal about the true source of Warren Buffett’s outperformance?

It shows that his returns are driven by systematic factor exposures, not mystical alpha passwords. The landmark empirical audit by Frazzini, Kabiller, and Pedersen proved that Berkshire’s historical returns are heavily explained by disciplined tilts toward Quality, Value, and Low-Beta factor premiums, which were then magnified by stable, low-cost structural leverage. It demonstrates that the core mechanisms behind his success can be understood through systematic portfolio design rather than purely relying on unreplicable stock-picking intuition.

This article is also available in Spanish. Leé la versión en castellano: Buffett, Graham y el verdadero significado del margen de seguridad