If you spend any time on retail financial forums, the narrative surrounding Warren Buffett sounds less like corporate finance and more like a collection of folksy historical anecdotes. The story goes like this: a patient man sits in a modest office in Omaha, reads physical annual reports, buys wonderful businesses at fair prices using pure cash savings, and holds them forever. No tricks, no debt, just pure, unadulterated stock-picking zen.

It’s a beautiful story. It is also dangerously incomplete.

The folklore focuses almost entirely on the choice of securities while completely omitting the architecture of the vehicle. Berkshire Hathaway is not a massive mutual fund that happens to be listed on the New York Stock Exchange. It is a corporate holding company whose returns were shaped by float, retained earnings, corporate tax deferral, and permanent capital.

Warren Buffett was not just a great investor. He was the architect of a closed-loop institutional compounding container.

Most investors spend their lives obsessing over the snowball—the specific equity selection, the forward price-to-earnings ratio, the near-term catalyst. But Berkshire was not just a pile of investments. It was a snowball factory. The structural genius was not merely finding wet snow; it was building a hill where the snowball could keep rolling for sixty years without being interrupted by taxes, fund redemptions, margin calls, or impatient clients. Berkshire turned compounding from an erratic investment result into a self-reinforcing system.

The Difference Between a Great Investor and a Great Compounder

To understand why Berkshire Hathaway became the definitive corporate powerhouse of the modern era, we have to separate individual investment skill from structural compounding durability. A person can make brilliant investments over a multi-decade horizon, but individual brilliance is constantly exposed to outside friction.

A great investor finds mispriced assets. A great compounder is an architectural structure that keeps capital retained, redeployed, and protected from the most damaging forms of external interruption.

True long-term compounding requires more than asset selection alpha; it requires a fortress that prevents the compounding curve from being broken. In the arithmetic of wealth generation, any event that forces a premature liquidation, triggers a major tax realization, or causes capital to flee the portfolio is a structural failure mode.

An individual retail account or a standard asset management fund is inherently fragile. They are built on transient capital pools that can be expanded or contracted based on short-term performance chasers or macroeconomic panic.

An ultimate compounder, by contrast, is a closed-loop ecosystem. It treats capital as a permanent resource, retains and redeploys large amounts of internal operating cash flow after operating needs, taxes, claims, and reinvestment requirements, minimizes regulatory and tax leakages, and maintains the absolute behavioral and structural freedom to hold assets through catastrophic market cycles. The vehicle itself becomes the primary source of competitive advantage.

Why the Partnership Could Not Be the Final Vehicle

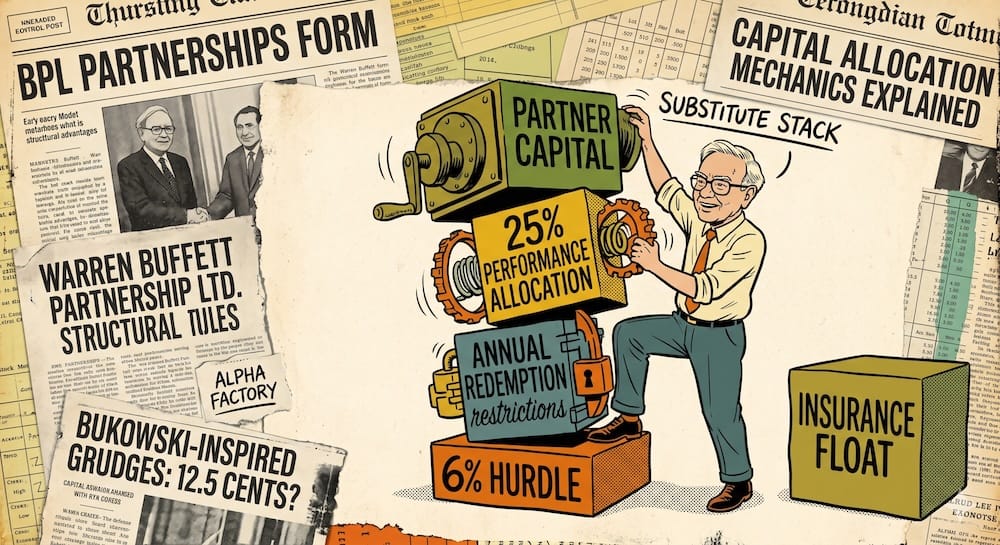

Before Berkshire Hathaway became a household name, Buffett ran one of the most successful investment vehicles in financial history: the Buffett Partnership Ltd. (BPL), which operated from 1956 to 1969. During this era, Buffett compounded capital at an astonishing rate of nearly 30% annually, drastically outperforming the Dow Jones Industrial Average. By any standard metrics of security selection, BPL was an absolute triumph.

Yet, despite its unprecedented performance, Buffett systematically disbanded the partnership at the end of 1969. The conventional narrative claims he exited because the market had become too speculative and cheap value stocks had vanished. While that market regime shift was certainly a tactical catalyst, it masks a deeper structural reality: the partnership model was fundamentally limited as a long-term compounding container.

An investment partnership, by its very design, contains structural configurations that threaten multi-decade continuity. First, it faces the vulnerability of capital withdrawal: partners had annual windows where they could withdraw their capital. This meant that during a severe, prolonged market downturn, Buffett was partially exposed to the behavior of his least resilient investors. If clients panicked en masse, he could be forced to liquidate positions to fund redemptions, regardless of how cheap those positions were.

Second, the pass-through entity design created a persistent tax interruption. Partnership gains were taxable to the individual partners on an annual basis, meaning capital was regularly pulled out of the compounding loop to pay the IRS. Finally, the partnership model faced severe scale and universe constraints. BPL was built on deep-value, small-cap liquidations and “net-net” arbitrage operations. As the capital pool expanded, the investable universe shrank rapidly. Buffett could not easily buy whole operating businesses or hold multi-billion-dollar corporate positions within a transient partnership framework. To turn compounding into an institutional machine that could run for half a century, Buffett needed to transition from a fund manager answering to external clients to a corporate allocator commanding permanent capital.

Berkshire’s First Compounding Loop — Permanent Capital

The pivot from the Buffett Partnership to Berkshire Hathaway occurred through an ironical corporate accident. In 1965, Buffett seized control of a declining New England textile mill. While the textile operations themselves were a capital-intensive, low-return mistake that he would spend two decades trying to salvage, the corporate shell he inherited provided the missing link for his compounding architecture: permanent corporate capital.

When an investor buys shares of Berkshire Hathaway on the open market, their capital does not enter or leave Berkshire’s corporate balance sheet. They are simply swapping ownership pieces with another market participant. If a shareholder panics during a market crash and dumps their stock, the operating capital inside Berkshire is not pulled out through investor redemptions.

This corporate structure eliminated fund-style redemption pressure that plagues traditional asset management. Buffett no longer had clients; he had shareholders. He no longer had to manage a liquidity buffer to meet sudden cash withdrawals, nor did he have to justify his quarterly performance to a nervous institutional board. Permanent capital transformed his investment horizon from months to decades. It gave Berkshire the unique capacity to become a permanent owner of assets, allowing the underlying business realities to play out completely insulated from short-term market noise.

The Second Loop — Float as Investable Fuel

With a permanent corporate container secured, the next requirement was an elastic, low-cost source of capital to expand the investment base without diluting existing shareholders or taking on dangerous bank debt. Buffett found this investable fuel in the property-casualty insurance industry, beginning with Berkshire’s acquisition of National Indemnity in 1967 for $8.6 million, followed later by the systematic expansion into GEICO and General Re.

Insurance operations generate a rolling pool of capital known as insurance float. Policyholders pay their premiums upfront, and the insurance company holds that cash until claims are settled years down the road.

Berkshire’s Float Reservoir (1970–2023)

The historical trajectory of Berkshire’s insurance float demonstrates how this capital reservoir scaled over time to fund major investments:

| Fiscal Year | Total Corporate Insurance Float | Scale Implications for the Container |

| 1970 | $39 Million | Provided early flexible capital to purchase concentrated public equities. |

| 1990 | $1.6 Billion | Enabled the wholesale acquisition of capital-light consumer monopolies. |

| 2010 | $65.8 Billion | Allowed multi-billion-dollar liquidity injections during global macro crises. |

| 2023 | $167 Billion | Formed a massive, institutional capital base insulated from fund-style flows. |

Academic work reconstructs Berkshire’s historical leverage profile at roughly 1.6x to 1.7x, depending on the specific evaluation window. But this was a liability-backed foundation of investable capital not subject to broker-style margin calls or fund-style redemptions. A 50% collapse in public stock prices did not trigger an automated liquidation routine.

Furthermore, this capital reservoir effectively earned money while holding investable float during profitable underwriting periods. When Berkshire’s insurance operations achieved a disciplined underwriting profit—meaning the premiums collected exceeded the eventual claims paid out—the cost of holding this leverage dropped below zero. Crucially, this float was not an unconstrained pot of speculative gold; it had to be carefully managed within strict underwriting, reserving, regulatory, and liquidity constraints. But under disciplined management, it provided a massive foundation of investable liabilities that amplified Berkshire’s asset base without structural debt service stress.

The Third Loop — Cash-Generating Subsidiaries

The third loop of the compounding container involved a deliberate shift away from pure stock-market operations toward the outright purchase of wholly owned operating businesses. The definitive archetype of this strategy was the 1972 acquisition of See’s Candies for $25 million.

At the time of purchase, See’s generated roughly $4 million in pre-tax earnings on only $8 million of net tangible assets. It was a powerful consumer franchise with immense pricing power, requiring minimal capital reinvestment to maintain its regional market dominance. Over the subsequent decades, See’s Candies turned into a cash-flow volcano, generating more than $2 billion in cumulative pre-tax profits for Berkshire. If See’s had remained an independent public company, its corporate board would have been pressured to either pay out those earnings as taxable dividends to shareholders or waste capital by over-expanding into regions where it lacked a competitive advantage.

Within the Berkshire container, the cash dynamics were entirely centralized. Excess cash that could not be reinvested at attractive rates inside See’s could be routed to Omaha. Buffett could then redirect that cash into buying insurance companies, funding capital-intensive infrastructure like BNSF Railway, or purchasing underpriced public equities. Berkshire became an internal capital clearinghouse, using mature, cash-rich subsidiaries as capital sources to fund the next generation of high-return compounders.

The Fourth Loop — Deferred Taxes and Low Turnover

Compounding is a game of geometric progressions, and the greatest enemy of geometric progression is friction. In a standard taxable investment environment, every portfolio transaction acts as a structural performance tax. In taxable accounts, dividends and realized gains can create tax drag that instantly shrinks the compounding base.

Berkshire systematically mitigated this friction through the disciplined use of corporate tax deferral. Because Berkshire operates as a C-Corporation holding company, unrealized capital gains on its public equity portfolio are not taxed until a voluntary liquidation occurs. By maintaining an ultra-low turnover profile on massive positions like Coca-Cola (initiated in 1988) or American Express, Berkshire kept billions of dollars of unrealized gains working on its balance sheet that would have otherwise been paid out to the federal government.

The tax-deferral effect can act like interest-free financing until realization. The capital continues to work inside the portfolio, generating dividends and capital appreciation on money that Berkshire technically owes but does not have to pay until it sells the shares. Combined with Berkshire’s long-standing policy of retaining earnings rather than paying regular dividends, the container ensured that capital faced lower internal friction, remaining locked inside the reservoir to compound unhindered by annual distributions.

The Fifth Loop — Crisis Optionality

Because Berkshire’s compounding container was built on permanent capital, billions in cash-generating subsidiaries, and an ever-expanding insurance float, it regularly accumulated massive liquidity reserves. In ordinary bull markets, this massive cash drag acts as an anchor on Berkshire’s Return on Equity (ROE). But over a sixty-year horizon, this structural patience yields a unique competitive advantage: crisis optionality.

When a severe systemic crisis hits, the entire financial system enters a state of forced liquidation. Asset managers face redemptions and are forced to sell their best assets; banks pull back credit lines; corporations find themselves locked out of traditional debt markets. Because Berkshire was entirely insulated from these short-term liabilities, it was uniquely positioned to act as a selective institutional liquidity provider when many market participants were facing liquidity stress.

During the global financial crisis of 2008 and its aftermath, Berkshire’s reputation and fortress balance sheet allowed it to secure preferred terms that later proved highly favorable, completely closed to ordinary market participants:

- Goldman Sachs (2008): A direct $5 billion cash injection in exchange for preferred stock carrying a 10% coupon, paired with attractive long-duration upside warrants.

- Bank of America (2011): An identical $5 billion liquidity rescue, securing a 6% preferred dividend alongside warrants to purchase 700 million common shares at terms that later proved highly favorable.

- Occidental Petroleum (2019): A $10 billion funding package structured with an 8% preferred stock dividend and extensive common stock warrants.

These deals were not simple exercises in public stock picking. They were structural extractions of alpha made possible because Berkshire held permanent, un-interrupted cash when the rest of the world was facing acute capital constraints.

Why the Compounder Survived Its Own Drawdowns

To truly appreciate why Berkshire Hathaway is the ultimate compounding container, one must examine its survival mechanics during moments of extreme market distress. The long-term track record of Berkshire—compounding at roughly 19.8% annually from 1965 through 2023 versus 10.2% for the S&P 500—looks smooth on a multi-decade chart. In real-time, however, the structural integrity of the container was repeatedly stress-tested by deep market price corrections.

During the 1973–1975 crisis, Berkshire suffered a -59% market price drop. The 1987 crash inflicted a rapid -37% blow. During the dot-com boom of 1998–2000, it faced a grueling -49% drawdown as value factors diverged sharply from speculative growth. Finally, the 2008 financial crisis brought a -51% collapse.

The dot-com bubble was perhaps the greatest behavioral test of the container’s design. As un-earning internet companies soared, Berkshire’s value-heavy portfolio fell by nearly half. Traditional investment funds during this era faced massive client redemptions, forcing value managers to liquidate their holdings at deep discounts to buy high-flying tech stocks just to stay solvent.

Berkshire’s structure completely altered this dynamic. Because its liabilities were tied to insurance claims rather than fund redemptions, and because its capital base was permanently locked inside the corporate shell, Buffett faced zero structural pressure to alter his strategy. The container allowed the compounding system to survive its own volatility without ever triggering a forced liquidation event. When the tech bubble burst, Berkshire’s capital base emerged completely intact, ready to deploy into the subsequent wreckage.

The Ultimate Compounder Flywheel

The important point is not that Berkshire had float, or deferred taxes, or subsidiaries, or cash. Plenty of firms have one or two of those. Berkshire became unusual because the loops reinforced each other. Float bought businesses. Businesses produced cash. Cash bought securities. Securities created deferred taxes. Deferred taxes kept more capital working. Reputation created crisis deals. Crisis deals expanded the capital base again. Over decades, these distinct variables locked together into a unified, self-reinforcing flywheel.

Berkshire Ultimate Compounder Flywheel Mapping

| Compounding Loop | Source of Capital | What Kept It Inside Berkshire | How It Fed the Next Loop |

| Permanent Capital | Corporate equity base, retained earnings, and shareholder capital locked inside the corporate shell. | Legal corporate shell structure; shareholders can only exit via open-market sales to other buyers. | Provided the un-callable foundation needed to safely own volatile insurance and equity assets. |

| Insurance Float | Upfront insurance premiums collected from property-casualty policyholders. | Long tail of insurance claims; structural insulation from broker margin terms and fund-style redemptions. | Expanded the total asset base, providing low-to-negative-cost financing for corporate acquisitions. |

| Subsidiary Cash Flows | Operational earnings from wholly owned businesses (e.g., See’s Candies). | Wholly owned subsidiaries and parent-level capital control. | Funded the purchase of new operating subsidiaries and massive public equity allocations. |

| Deferred Taxes | Unrealized capital gains on appreciated long-term public securities. | Ultra-low portfolio turnover; strict institutional avoidance of voluntary liquidation events. | Acted as a tax-deferral effect that can act like interest-free financing until realization. |

| Crisis Reputation | Accumulated cash reserves and systemic institutional standing. | Willingness to hold large cash balances through bull markets. | Extracted high-yielding preferred stock and equity warrants from distressed institutions during panics. |

BPL vs. Berkshire as a Compounding Vehicle

| Dimension | Buffett Partnership Ltd. (BPL) | Berkshire Hathaway Inc. | Why Berkshire Was the Better Compounder |

| Capital Permanence | Partially exposed; partners had annual withdrawal windows that exposed the pool to client behavior. | Permanent corporate capital; shareholders can sell shares, but cannot redeem capital from the company. | Buffett could allocate capital based on multi-decade horizons without managing short-term redemption cash buffers. |

| Tax Interruption | High; annual pass-through tax treatment forced capital out of the pool to satisfy partner IRS obligations. | Lower; internal cash movements face lower friction, and public equity gains are deferred indefinitely. | Reduced annual tax interruption, leaving gross returns intact to generate geometric progression. |

| Scale Capacity | Narrow; structural focus on micro-cap liquidations and net-nets hit asset capacity rapidly. | Far greater; capable of acquiring entire businesses and large public blocks. | Allowed the compounding system to absorb hundreds of billions of dollars without destroying its return profile. |

| Asset Ownership | Restricted primarily to passive minority stakes and small-cap arbitrage setups. | Unconstrained; capable of running a dual-engine architecture of wholly owned subsidiaries and public stocks. | Created an internal capital clearinghouse that could route cash dynamically across completely different industries. |

What Makes a Compounder Durable?

The true lesson of Berkshire Hathaway is not that you should buy insurance companies or try to secure preferred stock deals with global investment banks. The real takeaway is conceptual: if you want to build a portfolio that compounds over a lifetime, you must focus as much on the durability of your structure as you do on the selection of your assets.

Academic work suggests that a large share of Berkshire’s historical excess returns can be explained by systematic exposure to quality, value, low-beta characteristics, and structural financing. But those factor exposures only delivered their wealth-generating payloads because they were housed inside a vehicle that could not be broken by market cycles or structural leakages.

Structural Principles of the Compounding Container

| Feature | Berkshire Example | Why It Matters | Conceptual Retail Translation |

| Retained Capital | Corporate lockup; long-standing policy of retaining earnings rather than paying regular dividends. | Prevents capital from being leaked out of the compounding system prematurely. | Match your investment timeline to your capital durability; insulate core wealth inside long-term accounts. |

| Low Turnover | Decades-long holding periods for core equity positions. | Eliminates the transaction costs and intermediate tax liquidations that degrade geometric growth. | Reduce avoidable high-turnover trading habits; do not confuse frequent portfolio activity with real financial progress. |

| Low-Cost Liabilities | Underwriting discipline that anchors insurance float below market interest rates. | Amplifies the investable asset base safely without exposing the container to standard debt service stress. | Keep structural costs near zero; ensure your portfolio is funded by stable, personal capital reserves. |

| Low Forced-Selling Risk | Total freedom from broker margin rules and client fund redemptions. | Guarantees the portfolio can hold distressed, highly undervalued assets through deep market corrections. | Recognize that high-cost, callable margin can create forced-selling risk. |

| Reinvestment Optionality | Massive cash reservoirs held patiently throughout long bull cycles. | Transforms market panic from a portfolio threat into a prime capital deployment window. | Understand the role of liquidity buffers in reducing forced-selling risk. |

The ultimate translation for a self-directed investor is to stop looking at Berkshire Hathaway as a simple stock portfolio and start viewing it as an object lesson in structural design. You do not need to clone Buffett’s exact 13F filings or spend your days dreaming of insurance float to win.

Instead, look at your own compounding container and focus on reducing the frictions you can control. The fundamental lesson is to reduce the chance of forced selling, minimize avoidable turnover, understand the profound impact of tax drag, and avoid confusing constant activity with durable compounding. Build a container where capital can run uninterrupted for decades, and let the architecture do the heavy lifting.

Educational Trade-Off Note: Attempting to match Berkshire’s high single-stock concentration metrics without its underlying corporate structural safety nets—such as permanent capital and diversified, wholly owned operating cash flows—exposes an individual saver to extreme tracking error and permanent capital ruin risks. For individual retirement savers, structural tax efficiency and systematic risk diversification are far more reliable wealth compounders than concentrated hero worship.

What was the core difference between the Buffett Partnership and Berkshire Hathaway?

The structural architecture of the capital pool. In the Buffett Partnership Ltd. (BPL), capital was partially exposed because external partners had annual withdrawal windows, forcing a focus on short-term liquidity. Berkshire Hathaway provided permanent corporate capital inside a corporate shell, meaning shareholders could trade stock, but the operating capital could never be pulled out through fund-style redemptions.

How did insurance float act as leverage for Warren Buffett?

It functioned as an elastic, non-callable foundation of investable capital. Property-casualty insurance operations collect premiums upfront and pay claims years later. Academic work estimates this float-supported financing amplified Berkshire’s leverage to roughly 1.6x to 1.7x without exposing the company to standard, automated broker margin calls during severe market drawdowns.

Did Warren Buffett use traditional bank debt or broker margin lines?

No. Buffett systematically avoided standard broker margin lines because they introduce forced-selling risk at cyclical market bottoms. Instead, he relied on liability-backed insurance float and deferred tax positions, which carry no contractual call options or short-term debt servicing triggers from external lenders.

How did corporate tax deferral accelerate Berkshire’s compounding loop?

By operating as a C-Corporation holding company and maintaining an ultra-low turnover portfolio. Under the U.S. internal revenue code, unrealized capital gains are not taxed until a voluntary liquidation event. This structural tax-deferral effect can act like an interest-free financing source from the government, keeping billions of dollars of unrealized gains working on the balance sheet.

What role did wholly owned subsidiaries like See’s Candies play in the flywheel?

They served as capital sources for parent-level control. See’s Candies generated massive cash flows but required minimal internal capital to protect its regional market dominance. Instead of being forced to pay taxable dividends, this excess cash was routed to Omaha, allowing the corporate headquarters to dynamically redistribute capital into higher-return opportunities.

Can a retail investor replicate Berkshire’s non-callable leverage today?

Not exactly. A standard retail terminal lacks access to an institutional property-casualty insurance network to harvest negative-cost float. Attempting to match Berkshire’s structural amplification using standard callable broker margin exposes an individual portfolio to permanent capital ruin during standard market cycles.

What is the primary lesson a modern DIY investor should absorb from this article?

Focus deeply on structural durability rather than single-stock chasing. The conceptual translation for a self-directed portfolio is to reduce avoidable high-turnover trading habits, recognize that high-cost callable margin creates forced-selling risk, and understand the role of tax location and liquidity buffers in protecting the compounding container from being broken.

This article is also available in Spanish. [Leé la versión en castellano: Cómo Berkshire Hathaway se convirtió en el contenedor de interés compuesto definitivo de Warren Buffett]